Spotlight sheds light on a topic of interest or current relevance.

September 18, 2018

“There is no free lunch” – this also applies to the passive versus active investing debate. Passive investing comes with a favorable price tag, but also entails certain trade-offs.

Passive investing and ETFs

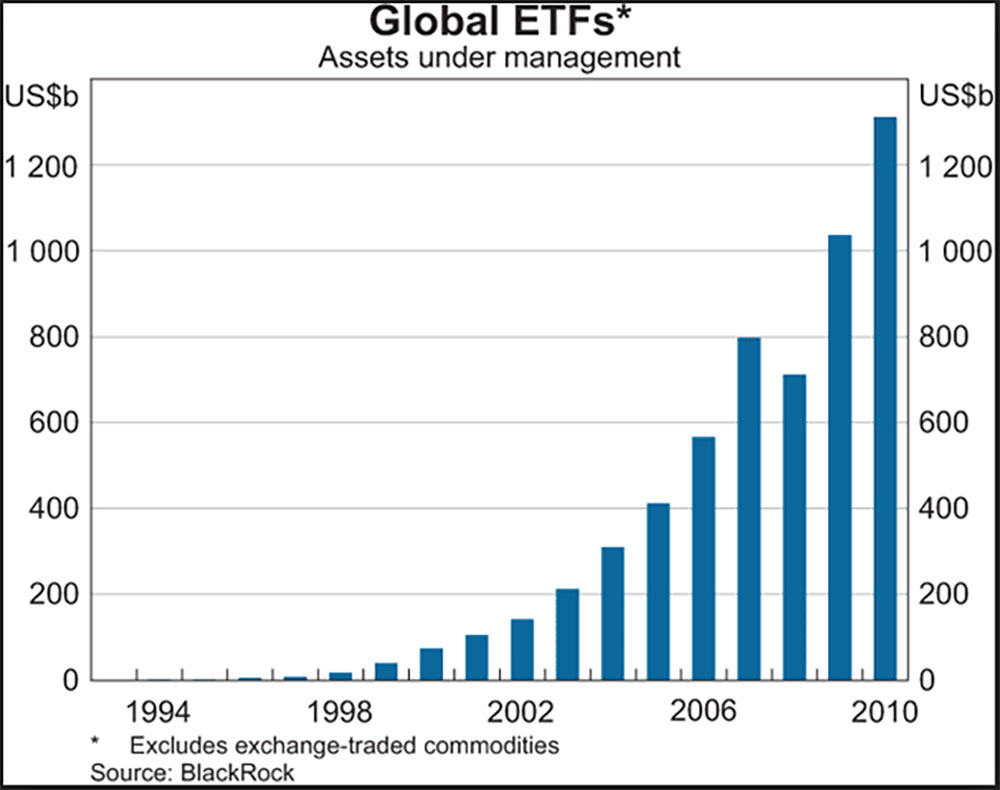

With the advent of exchange-traded funds (ETFs), the market share of passive investing has steadily increased. Passive forms of investment now account for almost half of the market volume.

There are a number of vehicles that do not actively select shares or bonds, for example, but instead aim to provide access to the “market” as holistically and unfiltered as possible. What slowly began to make the rounds around the turn of the millennium has been on everyone’s lips for the last few years. One important form of this is the ETF. No wonder, because ETFs provide uncomplicated access to diversified investments at rock-bottom costs. ETFs also offer access to various investment themes or investment strategies. In this issue of “spotlight”, we would like to take a closer look at how this works in practice and what investors may ultimately hold in their portfolios.

It was invented by John Bogle. On August 31, 1976 – 16 months after Vanguard was founded – the current Chairman of the Board of Directors of Vanguard Group launched an index vehicle on the stock exchange. The four most powerful brokerage houses in the USA were on board and had expected around USD 150 million in value or capitalization. At the close of the book, only around USD 11.3 million had been raised and the brokers wanted to cancel the IPO. Jack Bogle stuck to his guns, as this was the first traded index fund to be launched. In addition to Mr. Bogle, Nobel Prize winner Samuelson was also of great importance, as he had already written a paper on passive indexing in 1951 and is therefore the spiritual father. The original USD 11 million was then worth around USD 100 million in 1999. ETFs have definitely arrived in the investment world. Even the Great Financial Crisis (GFC) in 2008/09 did little to dampen growth – after many investors got a bloody nose, growth in passive investments actually increased as the belief in equity selection suffered. The broad market is a safer place to ride.

As is so often the case in life, good intentions can lead to a result that brings new problems, or else: what’s written on the tin is not always what’s in it.

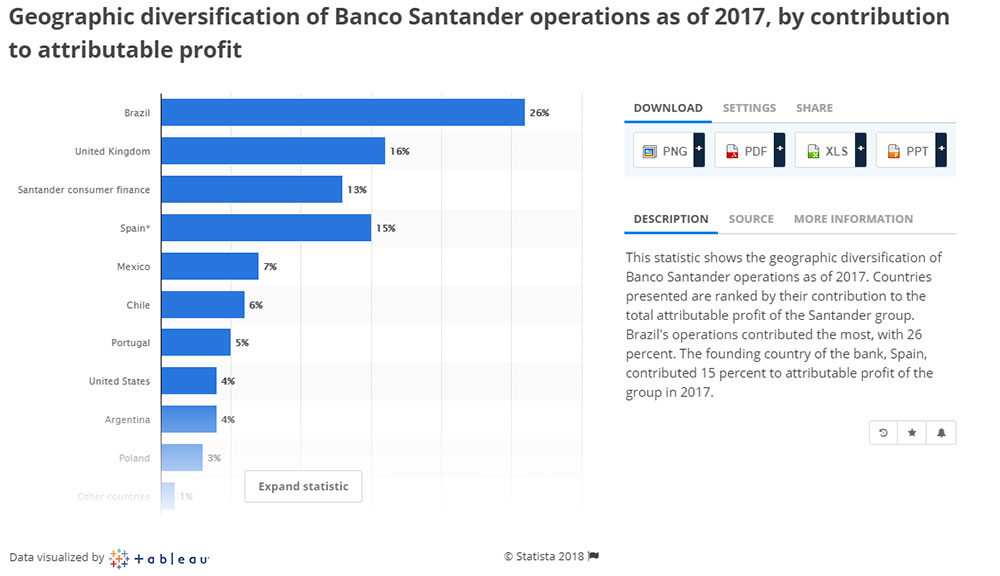

Passive investment is rule-based or simply attempts to replicate an index. In the latter and most widespread case of reproducing the index, the client should have access to the broad market. This increases security through diversification, according to the generally accepted opinion. There is no speculation through the selection of rivets. It should be mentioned in passing that the index itself also represents a selection. This may be determined by a committee, as with the American S&P Index, or by capitalization (the largest companies) or price (Dow Jones Index), as with other indices. For example, with the QQQ, which represents the Nasdaq, the client has a relatively large share of the investment in just 5 stocks: Facebook, Microsoft, Apple, Amazon and Google. If it were an actively managed investment fund, in some jurisdictions the regulator would intervene as such a concentration in individual stocks is not allowed (if the vehicle replicates an index, then it is allowed). If clients want easy access to a specific region or country, ETFs or other passive investment options are also available. In the ishares MSCI Spain ETF, for example, most of the invested capital is in companies that do not necessarily do business in Spain. The largest position, Banco Santander, for example, earns more money in Brazil than 1/6 in Spain.

In the valuation of the ETF, e.g. the price/earnings ratio, it can also happen that companies with a loss and therefore a negative price/earnings ratio or growth stocks with an absurdly high price/earnings ratio are excluded from the calculation.

As passive investing does not involve any major entry barriers, the business is characterized by thin margins. High volumes are required in order to make a profit. As a consequence, you need high turnover in shares, for example, which are part of the product. For example, shares from an index may not be included in the ETF because the turnover per tick movement is too low.

With the now significant proportion of passive investments in the market, liquidity is becoming more and more of an issue. The actual task of the market would be to determine the price. Passive investing means that this price mechanism no longer works properly. This is because, as described above, capital flows into either large-capitalized stocks or others that can demonstrate a certain trading volume without any valuation of the transaction, the balance sheet, being carried out. Certain strategies, such as momentum strategies, work well because the money that is reinvested always goes back into the same selected stocks. Value ETFs, for example, also benefit because the ETFs are dependent on large stocks and therefore the same stocks can be found in many large ETFs. If one day money is withdrawn from the market and profits are realized, liquidity is likely to become a problem.

In contrast to passive investing, active stock selection means that money is not invested almost blindly according to market capitalization or stock price. Instead, transactions are analyzed and evaluated. This pricing process has been partially prevented or disrupted by the increased emergence of passive forms of investment. Securities that are strongly represented in ETFs are becoming more expensive and those that are not (or no longer) part of them (because the ETF has become too large) are lagging behind the market and have had to underperform somewhat.

The seemingly favorable investment opportunity of passive investing therefore also comes with a price – because nothing is free.

Your EDURAN AG