The Navigator provides insight into stock market events with an outlook.

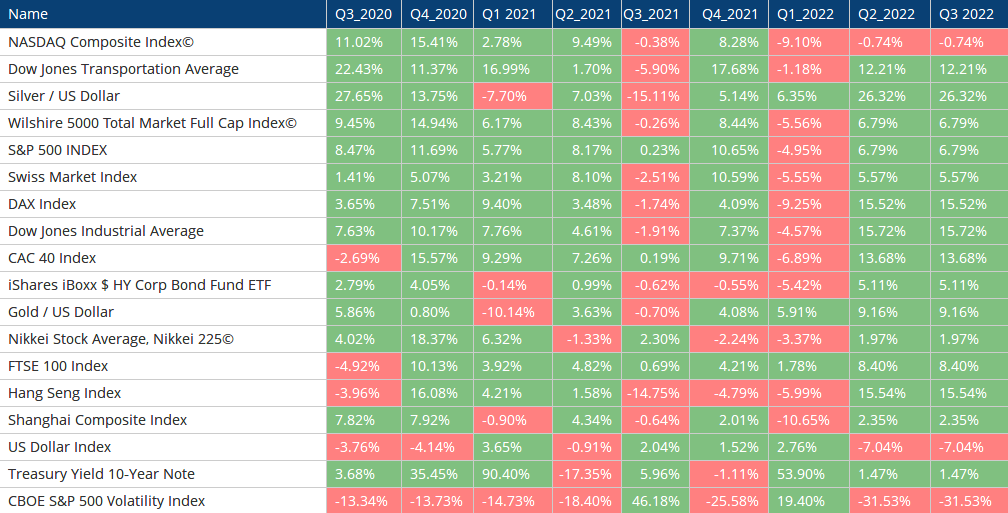

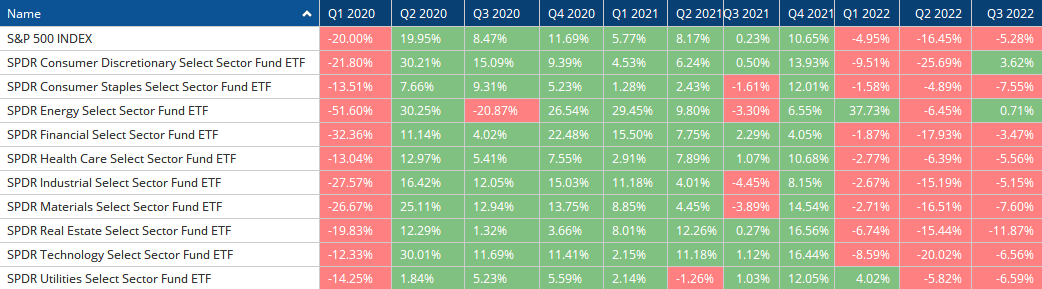

Market review

Among sectors, the real estate sector, in particular, felt the pressure of interest rates, while the energy and consumer goods sectors saw slight gains, after the latter had suffered massive losses in the previous quarter.

Gold also continued to lose ground, breaking the crucial support level of USD 1680 per ounce in mid-September. Bitcoin & co. also suffered from the liquidity crunch and were well represented on the supply side.

In focus

The dollar continued its spectacular upward trend. This is causing increasing stress in the global financial system, leading to the need to sell reserves to provide the economy with the required liquidity; US Treasury bonds and gold have come under pressure. So much for the monetary aspect, where the paradigm shift by central banks, late in the cycle and forced by headline-grabbing inflation reports, is draining the usual liquidity from the economy.

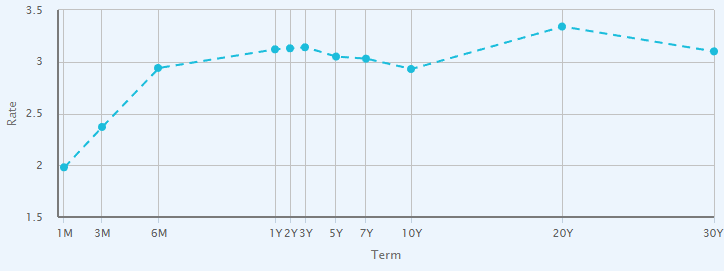

Commodities have also weakened, which in turn reflects the ailing economy. This is also true for the situation in China, where the economy is suffering due to lockdowns. Furthermore, the government has decided to curb the real estate boom: ‘Houses are for living,’ is the new motto. Generally, it can be said that leading indicators, in contrast to lagging ones, already point to an economic slowdown – with varying degrees depending on the region. However, the head of the US central bank made it clear in recent statements that the chosen course should be maintained and thus interest rates will continue to be raised. The yield curve is already in a structure, an inverted curve, which is typically followed by a recession.

Thus, again with regard to the USD, a record-high US trade deficit is observed, a large part of which goes to China. Normally, these dollars flow back to the USA (are ‘recycled’), be it through investments in companies, infrastructure, real estate, or simply via the purchase of US Treasury bonds. Due to the lockdowns, the situation is now different – almost none of this is happening, and most of the money remains in China. If the zero-Covid strategy is lifted, this could trigger a new surge in inflation, as a lot of capital flows again or simply Chinese tourists book hotel rooms again, where, incidentally, there is a shortage of skilled workers, especially in the tourism industry. In addition, the energy sector, which already represents a scarce supply due to a combination of climate protection (new investments in fossil fuels are difficult) and sanctions against Russia, would further stimulate prices through a possible revival of production in China.

Outlook

Barring any unforeseen events, central banks are likely to stick to their announced course and – as we believe – continue to raise interest rates ‘preemptively’. This is because they can, as labor market statistics still permit it. Soon, signs of a recession are likely to appear in lagging indicators, such as unemployment statistics, prompting central banks to apply the brakes on interest rates or deviate from the current course. Unless China reverses its Covid policy, lifts lockdowns, and inflation temporarily receives new impetus. It can be stated that uncertainties persist, and regardless of the outcome: central banks primarily react and lag behind developments. Within the US central bank, opinions appear to be widely divergent; for some, the time would be near or already here to stop or even reverse interest rate hikes, while for others, including Chairman Powell, it is still too early, and they intend to continue tightening monetary policy. For portfolios, this means continuing to focus on quality with an emphasis on capital preservation rather than profit maximization. In the current environment, interest rates offer initial opportunities for new investments, albeit with inherent uncertainties and thus only cautiously. Because the possibility of lower interest rates, even if only in the medium term, remains. In such an environment, it is advisable not to be swayed by immediate impulses, but to remain calm, consider the bigger picture, and indeed, stick to quality.

“In the dark, the blind find their way better than we do.” Otto Ernst

EDURAN AG

Thomas Dubach