The Navigator provides insight into stock market events with an outlook.

July 8, 2022

“Summer High”. Inflation reaches new highs, the stock market discounts the rise in interest rates, but ignores any declines in profits. If emotions give way to facts in this tense situation, a bear market rally could set in. However, a summer high could also be reflected in inflation, namely if capacity bottlenecks can be overcome. With the wage increases already implemented in part by trade unions, inflation is likely to remain an issue for the foreseeable future, albeit less pronounced. At the same time, a cooling of the economy is to be expected, which harbors further correction potential in the markets. What was less in demand in the bull market can make the difference in such an environment: Active stock selection.

Market review

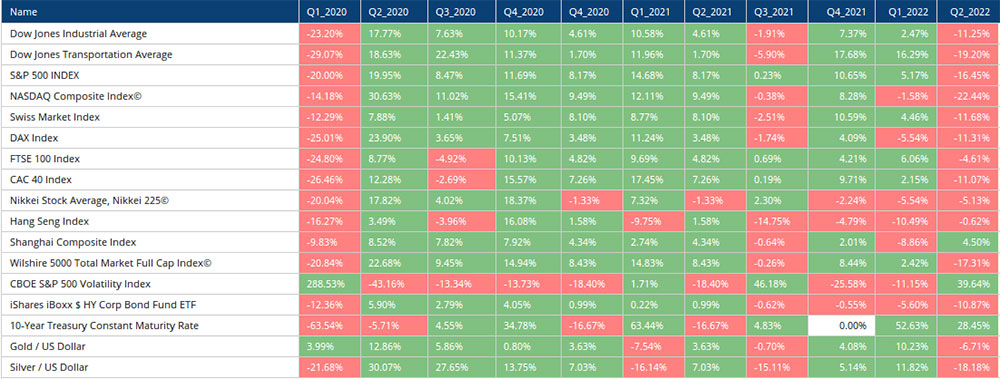

The second quarter was marked by an acute phase of market weakness. While the American indices continued the correction from the previous quarter without delay, European indices temporarily showed a certain strength, which was then ended towards the end of the quarter with abrupt slumps back to previous lows from the 1st quarter. The DAX, for example, lost over 10% in the last month alone.

After gold was still able to record new highs in the first quarter, the precious metal, together with silver, also continued its correction and was just able to hold slightly above the last lows.

The yields on government bonds, measured against the benchmark with a 10-year term, reached new highs in the course of the quarter and eased slightly towards the end.

With a view to the yield curve, the markets’ assessment is that the recent interest rate hikes, alone 0.75% by the US central bank in June – which is virtually a doubling of the interest rate level, will weaken the economy, so that the central bank will soon have to moderate again. In other words, the capital market expects a weakening of the economy and an inflation that is tamer than what can be gleaned from the media noise.

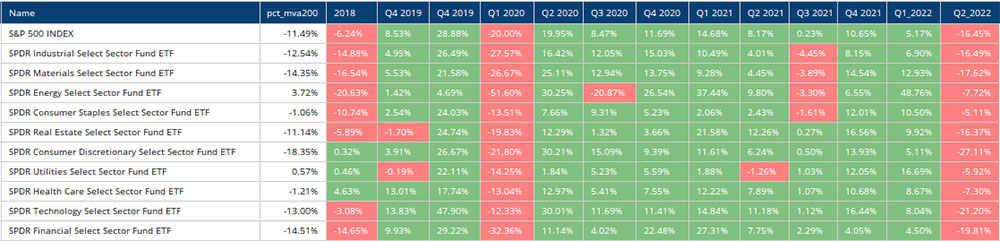

In terms of sectors, everything suffered primarily that had to adjust forecasts downwards in an environment of tightening liquidity or due to the rising costs of tightening energy. The relative winners were therefore the defensive consumer stocks or the energy stocks themselves.

In focus

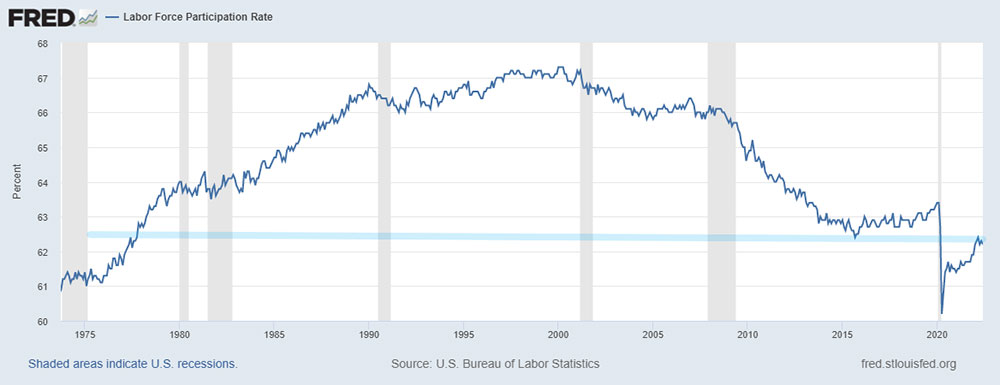

If one believes the statements of government agencies, the economy is in good, if not very good condition. The growth rate globally is around 4.5% – higher than average. In the still largest economy in the world, the USA, the economy shrank according to the latest measurement as of the 1st quarter of 2022 already by 1.6%. The strong labor market with record lows in unemployment figures is also often mentioned – in the USA as low as last before the pandemic and before that only in 1969/70. However, participation in this labor market, and this is hardly reported, is still around one point below the level before the start of the pandemic at 62.5% and as low as last only in 2015 and at the end of the seventies.

Even if the income situation of households still proves to be robust and a still solid demand for goods and services persists, consumer confidence has deteriorated significantly in the 2nd quarter according to surveys. In addition, the output of the economy, using the example of the world’s largest economy, the USA, pressed in units, shows a decline. In short: The economy is showing weakness, or is at least not as strong as officially announced.

Inflation has become the focus of politics, no wonder, it affects many households and thus potential voters sensitively. There is talk of price caps, reserves are tapped into in the energy supply (Biden in the USA) and the central banks – whether independent or not – have woken up from their slumber and are trying to break the price dynamics through measures and speeches. Whether interest rate hikes really break inflation in such an environment is questionable. Unlike in the seventies, we are not in a booming economy. Capacity bottlenecks will keep us busy for a while. First through the pandemic, where businesses were closed or then ports, which in turn laid off employees. The governments have absorbed the wage losses and the money has been happily spent in online shopping while restaurants and cinemas as well as casinos and amusement parks were closed. When the lockdowns were lifted again, the ports were literally flooded with ordered loads from the Far East, so that the ships often had to return without the emptied containers because there was no time to reload them. The prices for containers have accordingly risen from originally USD 1,000 to over 10,000. This also affects the prices of goods, apart from the increased demand. It is to be expected, and partly already noticeable, that the situation will normalize again. Logistics is slowly returning to the old routine, freight costs are falling, even if an aftertaste remains and the supply chains are partly being re-planned.

With the interest rate hikes, the companies are now again being put in a difficult position and production is being slowed down rather than promoted.

In addition, the post-war generation is entering retirement age these years: shortage of skilled workers everywhere. All in all, this is likely to lead to a higher price level, but driven more by structural nature than primarily by an excessive amount of money alone.

Outlook

The coming months will show whether we are sliding into a recession, even a sharp one, or whether everything will be less bad. A relaxation regarding the conflict with Russia would help Europe, and a flattening of inflation could mean a global avoidance of a recession.

Where liquidity is available, relatively attractive entry opportunities, to be approached with caution, also arise in this environment – relatively, because as a consequence of the previously described quantity situation, prices could continue to tumble. However, many values have already corrected sharply and, from a historical point of view, one no longer pays excessively expensive prices – precisely if the future earnings do not collapse too much. Have courage to face the gap: A first tranche for purchase is a good idea, especially where one has held back with additional purchases in recent years and has set aside liquidity. The markets are likely to have priced in the upcoming interest rate hikes and when the economy cools down, it will become clear whether the central banks will stick to their course with rising unemployment figures or fall back into the old ways of cheap money.

Nobody wants a sharp recession with unemployed people and in combination with already record high debts at the state level and especially we as a society in the West would face serious challenges. The pressure on politics and governments will thus increase not only on inflation but also on other levels. A defensive interpretation of the portfolios with a focus on investments with a steady flow of money pays off again.

“Stock prices fluctuate more than stock values.” Franklin Templeton

EDURAN AG

Thomas Dubach