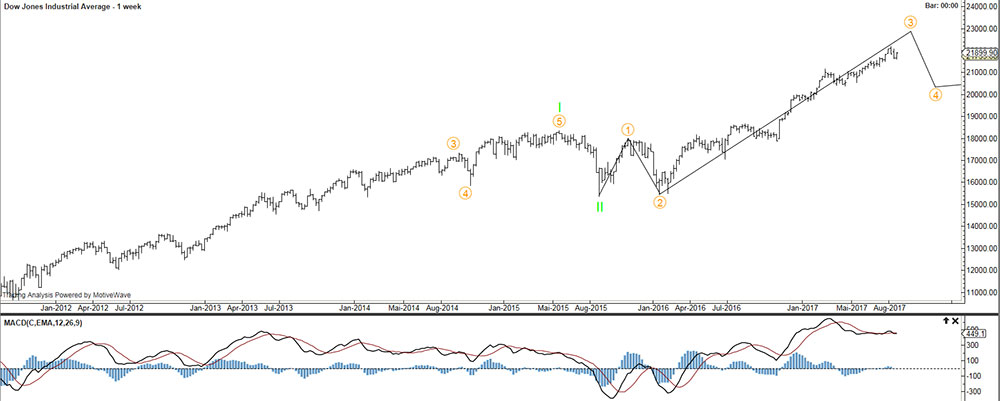

The markets have remained calm and consolidated for the most part over the summer. The correction that some market players had been expecting for some time has so far failed to materialize.

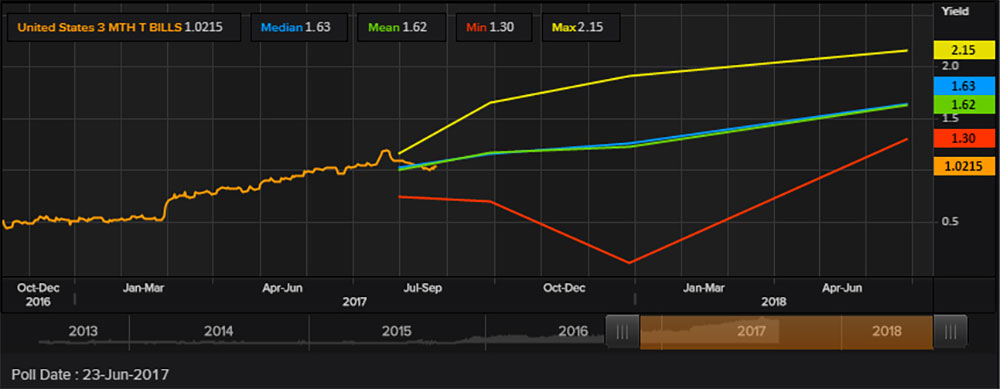

For some months now, market technology has also been increasingly pointing to potential, at least temporary, market weakness. The bottom line is that we are probably at – or close to – an important point in terms of further market development. In recent years, stock markets have been driven primarily by central bank activities. With the US Fed’s turnaround in interest rate policy, which has already been publicly discussed and is in the process of being implemented, the current structure is coming under pressure, ceteris paribus. The increasingly robust economy should have a positive effect on share prices – in contrast to recent attempts, this time also in Europe and emerging markets. It will probably be a balancing act between normalizing, rising interest rates and a strengthening economy, with slight advantages in favour of growth. The central bankers will be wary of tightening the screw too sharply.

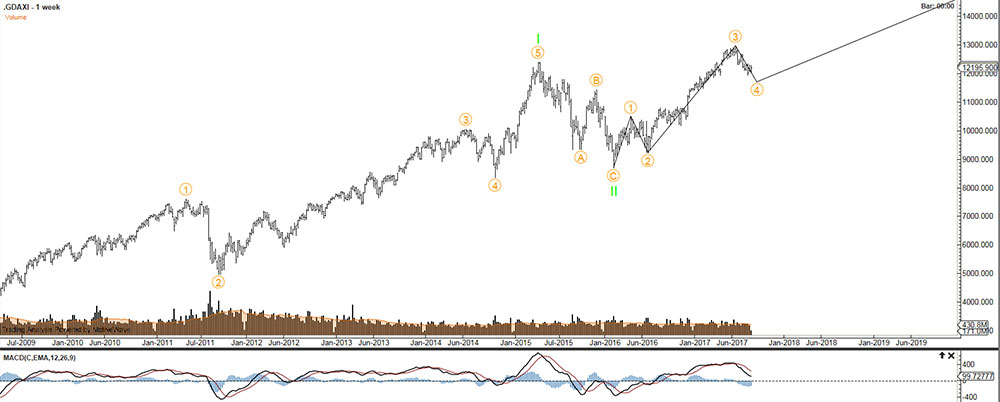

There will be many stumbling blocks and a clear investment strategy will help you not to lose your bearings.

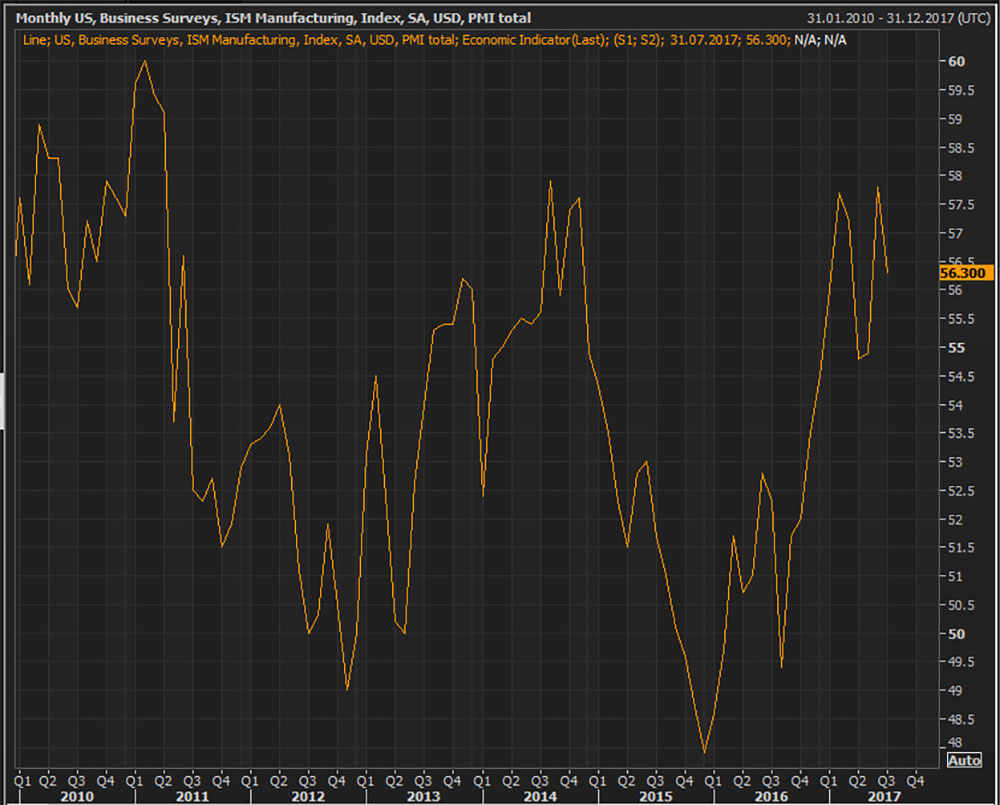

On average, companies’ latest earnings figures show an improved earnings situation and more stable business. 90% of S&P companies have reported above expectations for the first half of the year, with an average profit growth of around 10%. As published on various occasions, order books are well filled and consumer sentiment is back to the level seen before the global financial crisis around ten years ago.