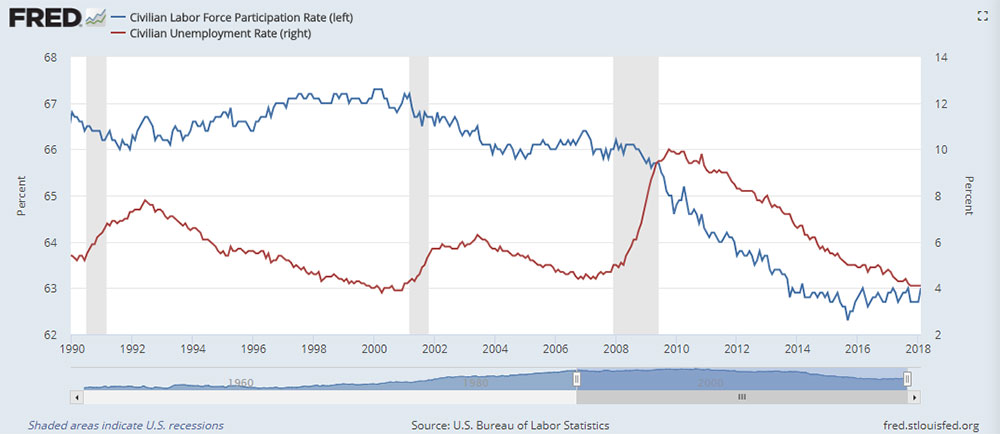

Interest rates continued their rise from the last quarter of 2017 at the start of the quarter. The rise in wages in the US, 2.6% for 2017 and then 2.9% for January 2018, the strongest increase since 2015, was a talking point. Voices predicting an imminent rise in inflation have become louder. Critics of rising inflation in the near future point to the still large pool of potential workers on the sidelines. When unemployment is relatively low, there is typically upward pressure on wages. Not so these days. Although the economy is doing well and unemployment figures in the US, for example, are also historically low, there has been no sharp rise in wages. The latest figures are rising, but were also seen in 2015 and then flattened out again. The 200,000 new jobs created per month in the period after the financial crisis in 08/09 is a good figure. In terms of the growth in newly created jobs, however, it is weaker than what was seen before the financial crisis. In the years before 2000, monthly job growth averaged 2.6% per year and even 3.1% in the 1980s. The crux of the matter probably lies in the denominator of the percentage of unemployed. With the financial crisis, millions of workers have dropped out of the labor force and subsequently out of the unemployment statistics. The proportion of the working-age population in the labor market (i.e. either with a job or looking for one) has fallen from just under 68% in 2000 to around 63%.

If the economy picks up, some people might consider looking for a job again and, as a consequence, wage growth would lose some of its momentum.

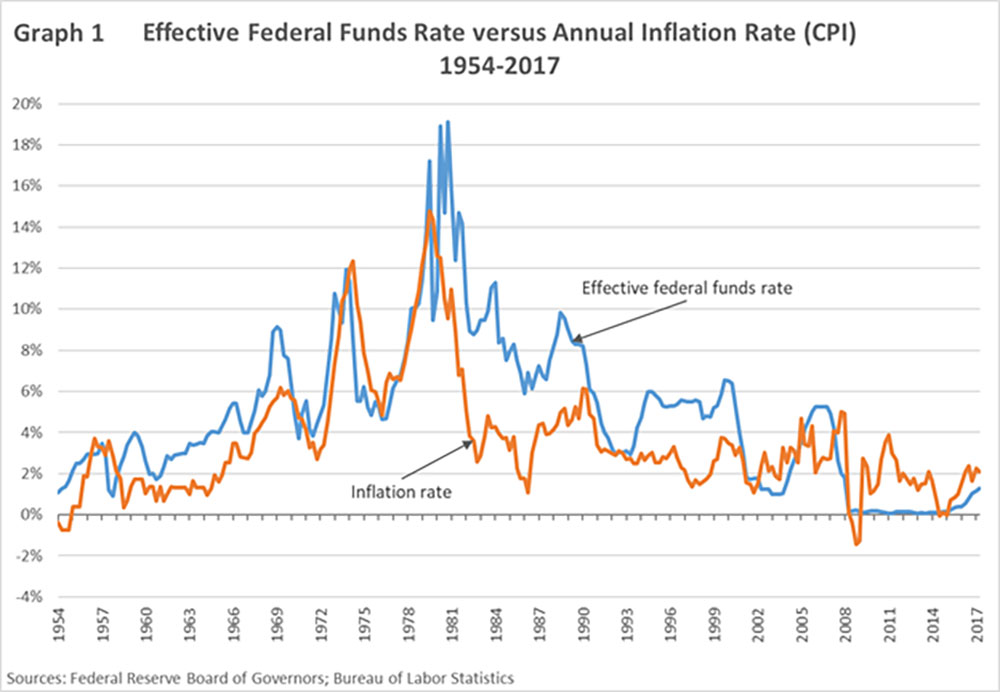

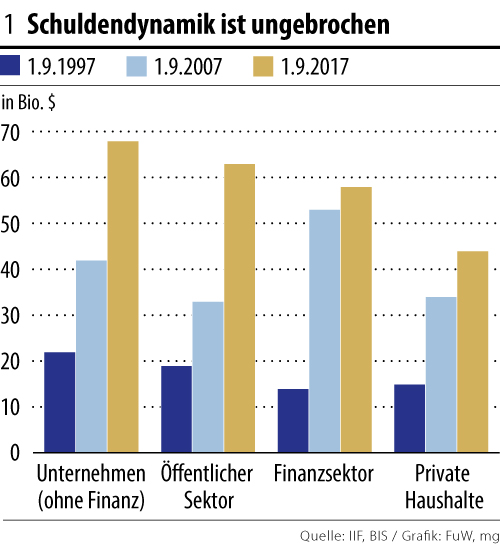

Inflation (CPI/official consumer price index) for the USA was 2.1% in February. After five years of an average of 1.3%, this is something of a revival. The situation in the eurozone is still somewhat different: although the ECB is still pursuing a very loose monetary policy, in contrast to the US Fed, inflation as at February 2018 is still some way off the target of 2% at 1.1%. History has shown time and again that inflation can rise relatively quickly and unexpectedly. The loose monetary policy practiced in recent years would typically be the basis for higher inflation in the future. When and to what extent remains to be seen. Political tensions, faltering globalization (recently discussed and threatened punitive tariffs) and, last but not least, the high debt burden are the cornerstones and are likely to have a significant impact on future developments.