The Navigator provides insight into stock market events with an outlook.

Market review

That’s how it can happen: At the end of 2018, there was a cold shower, and the market augurs didn’t see much good coming our way. Then Merlin didn’t come, but the central banks did, and they loosened monetary policy. The US Fed has abandoned the path towards “normalized” interest rate levels and has swung back towards lower key interest rates – to where the other relevant currency areas have been for some time. This circumstance alone helped to create a brilliant first quarter. As is well known, the fourth quarter also brings the year to an end – measured by stock market valuation, the fourth quarter continued what the first had begun, and the bottom line is a pleasing and successful stock market year 2019. In between, over the summer, fears arose about a weakening economy.

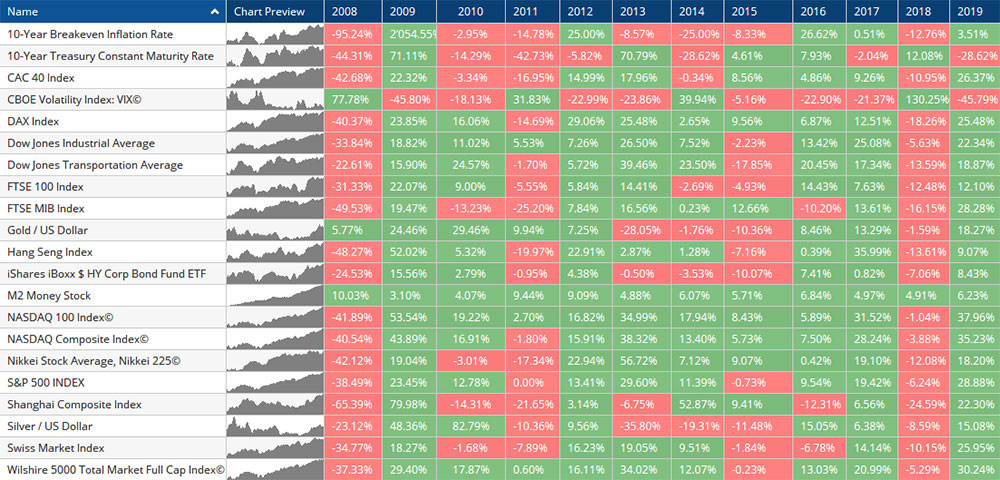

The bottom line is that 2019 has become the most successful year of the 10s decade for some markets, such as the Swiss Market Index. In addition to lower interest rates (higher bond valuations), gold also had a good year with a final spurt in the very last week.

It wasn’t just the stock market that experienced ups and downs. The world is also changing. While the change on the stock market was mainly due to the changing liquidity, a number of fundamental realignments are added in real life. This process continued in 2019, both socially and geopolitically, and in some cases intensified. The hegemon USA is being challenged by the growth region of Asia with the strengthening China. The globalized economy is experiencing headwinds and the value chains may be reorganized and handled regionally in the future, in a tripolar world (Americas, Asia, Europe and/or Russia). Geopolitically, it can already be seen today that the regional powers such as Russia, Turkey, and Iran are acting self-confidently and gaining influence. Added to this are demographic change, digitization and, last but not least, the urge to prevent climate change or simply to restructure the economy.

The stock markets are of course not isolated from these described tendencies, but investors pay little attention to the dangers arising from them. The course of the listings has so far been primarily determined by interest rates – and then by the course of the economy. After recession fears and a sideways movement or consolidation in the 3rd quarter, a change in sentiment came up in time before the start of the year-end quarter. The companies seem to be able to continue to hold profits, or in some cases even expand. In the tendency, however, it shows that the profits are weaker to lay down and more and more must be paid for a unit of future earnings.

If you look at the metrics regarding the state of the economy, here primarily the industry, these continue to show a rather sad picture. China as the previous growth engine has come to a standstill, the USA with President Trump’s tax reform, on the other hand, seem to float on top in the tendency and even if the first positive effect is over, capital will continue to flow back into the country and stimulate growth.

The PMI (Purchasing Managers Index) has deteriorated visibly over months and is still tending to be in recessive territory or is only moderately expansive. For large parts of the 2nd and 3rd quarters, this was even more sad. First signs of a recovery came towards the end of the summer and in time before the start of the 4th quarter: The trade dispute between the USA and China could soon – even if only in the sense of a paper – experience a relaxation. In addition, the consumer, which is so important for the western economies, still seems to be immune and not to show any weakness. This despite the battered industrial sector where short-time work has been introduced in some cases or various jobs are being cut (e.g. German automotive industry).

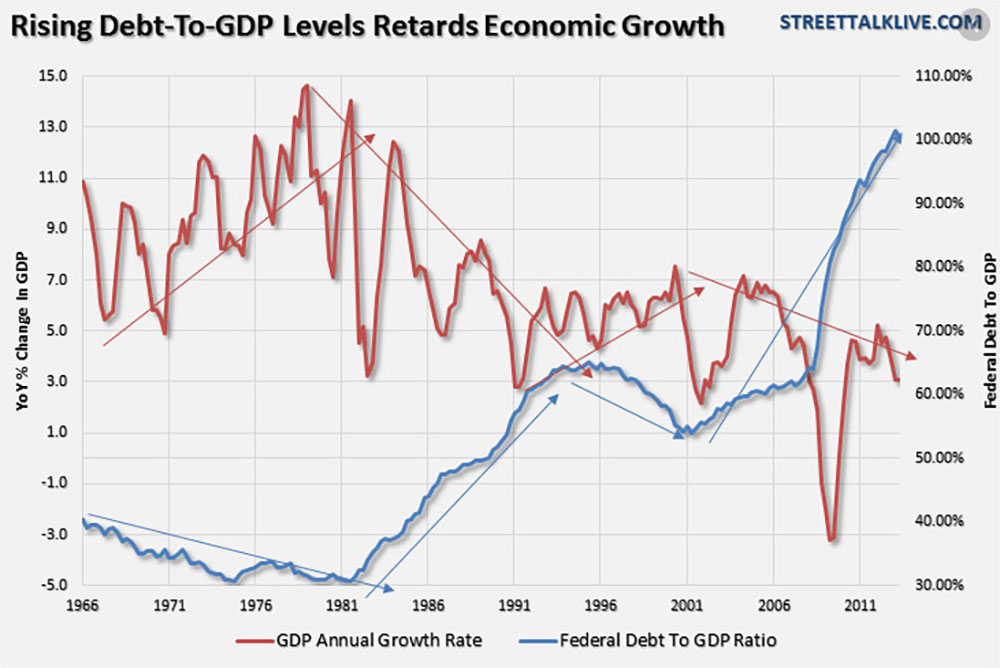

The economy is expected to continue to have a difficult time. The demography in the West, the high level of debt, etc. are weighing on growth. The central banks as sorcerer’s apprentices, which seem to be able to control the economy at will, are doing everything to ensure the necessary mood on the stock markets. Inflation does not seem to be an issue for the foreseeable future and this is where opinions diverge: If you look at the capital markets, interest rates could come under further pressure in the future, but risk premiums could rise. If profit growth slows down, private borrowers will come under pressure despite low interest rates. The states can continue to finance themselves cheaply. This although even more debt is to be expected, the OECD also insists on more government spending to stimulate economic growth. In recent years, public debt has increased more than gross national product.

Market insight

The capital flowed back into the stock markets. With the lows after the correction in the 4th quarter of 2018, the starting position arose to achieve dream returns in the past year. The valuation difference from the end of Q3 2018 to Q3 2019 or from summer to summer is less than half compared to the calendar year performance, and is still good at around 10%, but already closer to the long-term average of good stock market years.

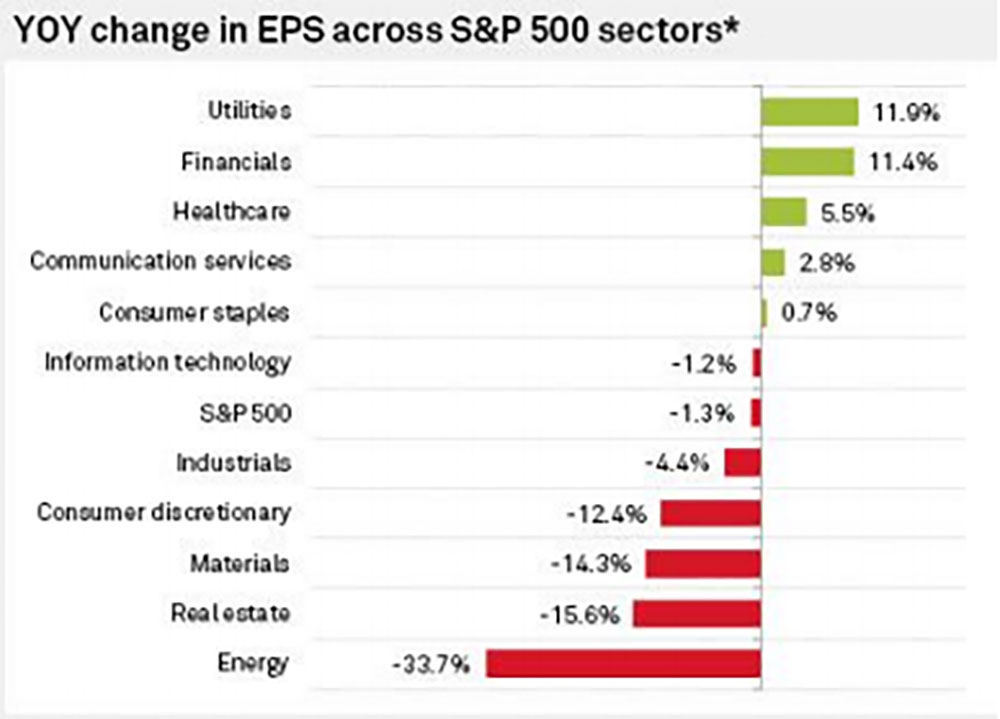

Above all, the technology stocks led the year-end rally. The change from a cautious, more defensive approach to a “risk-on” view was the main driver. Earnings figures have recently been reported a few in December, and of the few, most were able to surprise positively (in the S&P500, all four were able to exceed expectations, on average +1.8% better than the estimates).

However, it should be noted that after years of margin expansion, through cost savings and share buybacks for higher profit margins per share, this has recently been replaced by a valuation expansion. Over the year, earnings per share according to the latest figures (estimates) in the S&P 500 have grown by around 0.8%, thus less than the official inflation rate. The dividend yields have fallen from 2.1% to 1.75%.

The uncertainties regarding the trade dispute paralyze the companies to some extent with regard to investments. Also to be mentioned is the crisis of the automotive industry, which applies even more accentuated in Germany, and has just cut a notch in the order books of many suppliers in Switzerland. For the banks, after years of stock market malaise of recent years (!), there is again some hope: The yield curve is getting a little steeper and it is hoped that the institutes will adapt to the changing environment so that growth can happen again.

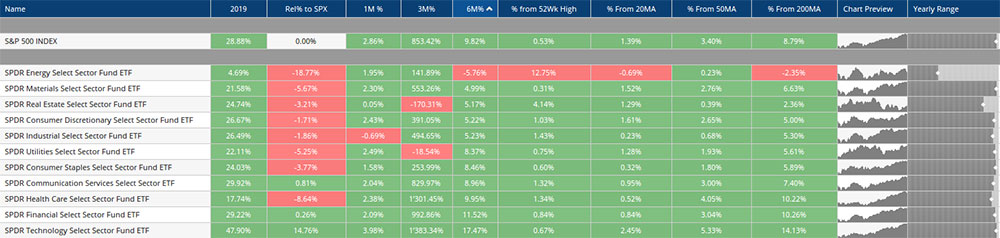

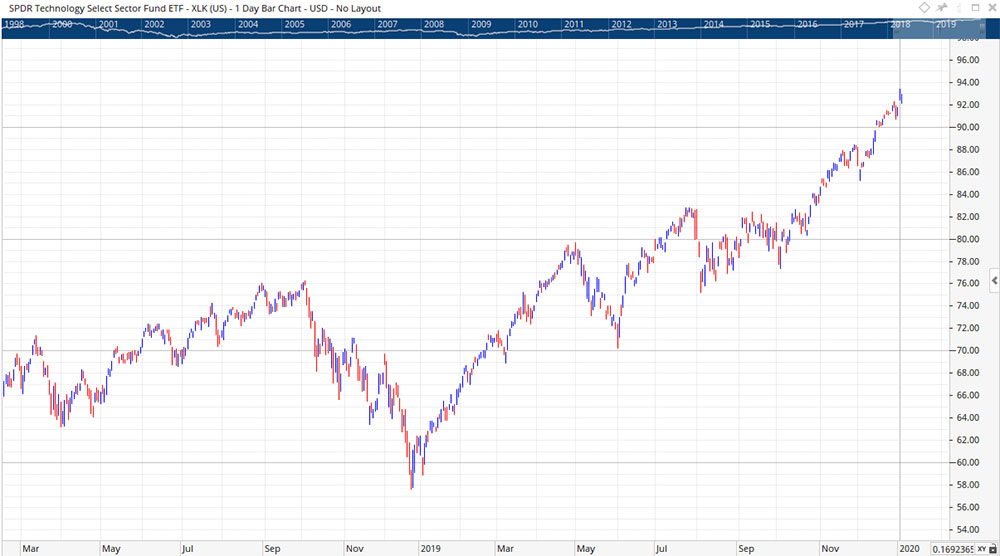

Broken down to the sectors, the technology-heavy Nasdaq Index showed the strongest appreciation since 2013 with +36% over the whole year (the SPDR Technology was even able to gain around 48%).

A workhorse was Apple, which gained around 86% in value over the year (around 31% in the last quarter)! This with a market capitalization per year-end of USD 1.3 trillion! (Total valuation of the US stock exchanges around USD 30 trillion).

Generally speaking, the growth stocks were in the lead. In addition to the technology sector already mentioned, which was able to gain strongly again as in the first quarter of 2019, the healthcare sector was also able to gain strongly. But also the industrial sector has been able to gain ground after a consolidation phase over the summer months.

The energy sector lags behind and is almost neglected by the investor community. We have placed an eye on this and see potential in some stocks in this sector. The cyclicality of this business extends over several years. After a years-long dent, the green wave of “climate change” has additionally inhibited investments, especially in certain energy sources such as fossil fuels. As a result, a supply shock could lead to higher prices in the future. Anyone who positions themselves today can – in addition to relatively favorable valuations – benefit from such a scenario.

Interest rates

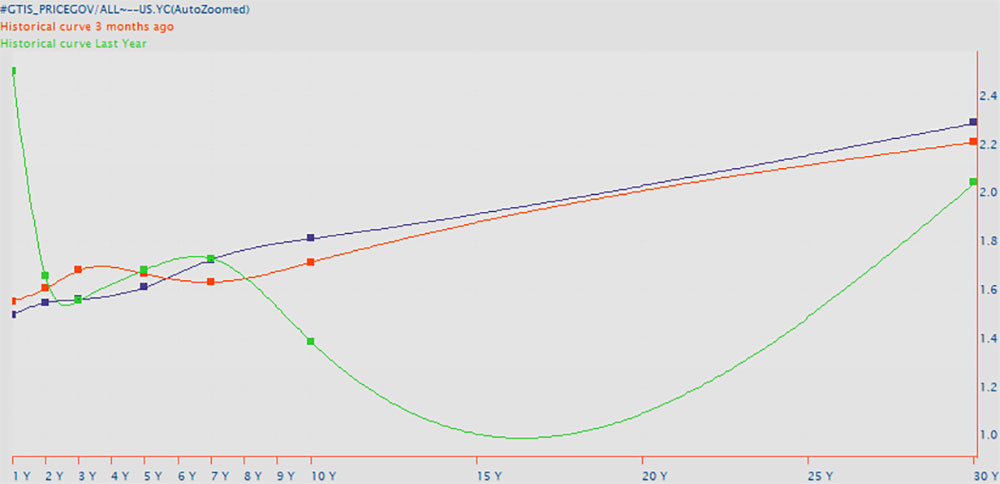

As in previous years, interest rates remain a very important factor for the stock markets. If you look at the big picture, there is not much new to report: Since the financial crisis of 2008/09, the central banks have kept interest rates low, first to help out, then because they could not bring themselves to get out of the emergency or first-aid mode again. In the lines of our Navigator report, we have regularly reported on this over the last quarters and tried to show the resulting constraints. After it seemed that in 2017/28 one finally wants to say goodbye to the policy of loose money supply, we are today again in the old rut and there is a threat for the new decade to give an increase: in addition to low interest rates also government debt for the purpose of economic growth (fiscal stimulus). A new trend is nevertheless emerging: the longer-term yields (e.g. 10-year US Treasury) have risen since the summer. The market does not seem to believe in further, even lower levels in the negative range (negative interest rates) for interest rates and a certain stabilization could be emerging at the present levels. Also possible is a paradigm shift towards higher risk premiums.

Inflation prospects could also play a certain role here, where the inflation-indexed bonds (here 10-year US government bonds) seem to have found a bottom since August. Whether this is just a flash in the pan or whether the many created money finds its way into the real economy (velocity of money would pick up), remains to be seen. In any case, our focus is also on this matter.

Market technology

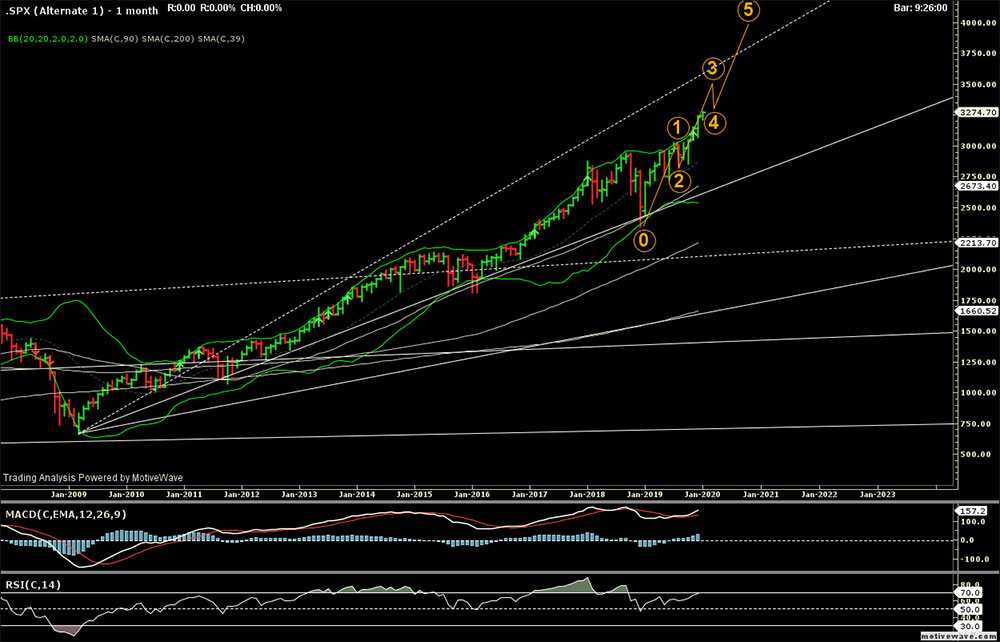

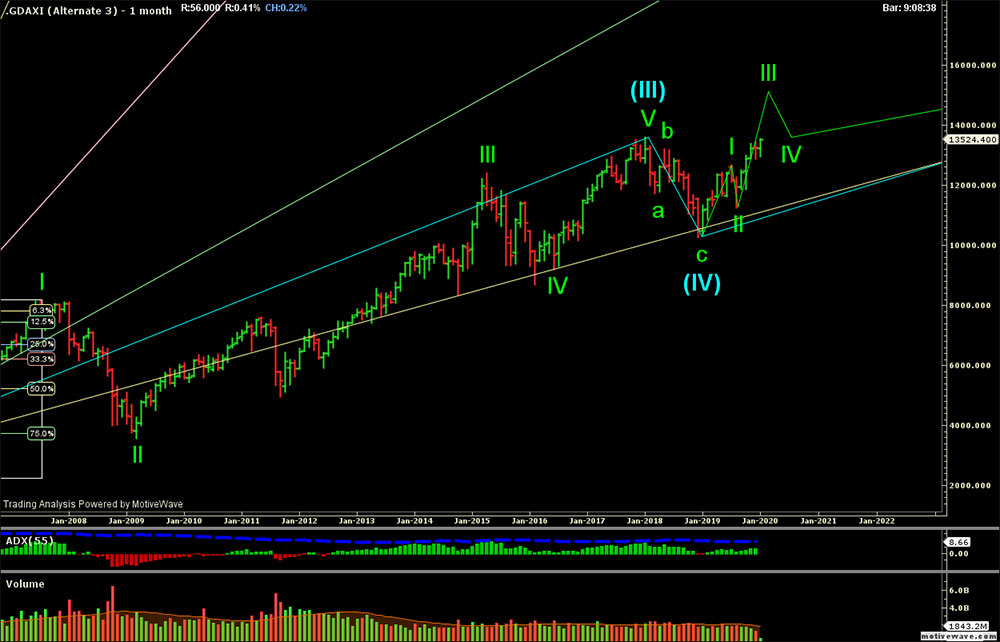

From a chart technical point of view, the markets are still in the already long-term upward trend – even if there is some indication that the bull market is in the area of the final phase. With regard to market breadth, the bull market has continuously decreased over the months since the summer, but since October there has been an improvement in this metric. The broad mass of stocks has been able to detach itself from the correction levels and increasingly gain with the large, index-driving titles.

If you look at the number of countries that reached new 52-week highs (market capitalization), although only about 20% of the 70 countries observed show new such highs, there is a strong increase in this number, which is crucial for the significance of this criterion. Seen in this way, the bull market has been able to catch itself and a further push upwards is possible.

Other, longer-term indicators, however, share – historically speaking – the view of an already advanced bull market. In the ratio between the total market capitalization measured with the Willshire 5000 Index (market capitalization) and the gross national product of the USA, one sees the record high valuations on the stock exchanges (30 trillion vs around 22 trillion).

Whether the valuations will continue to rise in a sustainable sense is doubtful. In the long term, it shows that the sum of price-earnings ratio plus the inflation rate is only able to exceed the mark of 20 temporarily (rule of 20). Recently, the profit growth has been surpassed by a valuation expansion. Without additional profit growth, the valuations are likely to experience a correction.

Outlook

As is well known, this year’s turn of the year also marks the beginning of a new decade. The 10s years on the stock market were marked by the interventionism of the central banks. There is some indication that we will not leave this rut so quickly. It is to be feared that in the new decade the governments will additionally come via fiscal stimulus. The OECD has been preaching for some time about higher debts, which should bring growth. Switzerland could also come under pressure here with its relatively moderate national debt. The new ECB chief Christian Lagarde also mentioned in her speech in the EU Parliament her goodwill towards Green Bonds. The fact that the price-finding process is further misled here does not seem to be of great interest. The views are changing to an increasing extent and voices that believe in the omnipotence of the central banks are gaining in popularity. The growth of the economy (and as a result also the control of inflation) should thus be able to be controlled almost at will, so the understanding (keyword Modern Money Theory, MMT).

With regard to the schedule, a more volatile stock market could already blossom in the spring of 2020. The Brexit is planned for the end of January. The USA is also in the election year where populism is likely to be booming (left as right). The valuations are rather high and the depth of fall as well. An environment thus where corrections are possible. If signs of a trend reversal show up on the interest rate side, i.e. signs of an increase in inflation (velocity of money), we will be more cautious. But also as before, we pay attention to the valuation, where an increase is likely to lead us to profit-taking. With the currently low interest rates or even negative interest rates, money is likely to continue to flow into the stock markets as well as into other risk papers in 2020 and, ceteris paribus, tend to bring high prices for future earnings.

We wish you a good start into the new year!

EDURAN AG

Thomas Dubach