There are always stumbling blocks on the way of the stock market. If the driving forces of the prices are solid enough, the hiker is fit enough, stumbling blocks cause at most short-term imbalance, some unrest. One catches oneself again. If the hiker is tired, or converted to the stock markets: if the driving forces of the stock market prices are not solid enough, a fall can result. The driving forces of this stock market boom are mostly to be found in the loose monetary policy. Not necessarily in great growth of the economy, sales or profit margins. Of course, there is also the structural change, which brings an upswing to certain branches of the economy, such as in technology stocks. But even there, prices have been driven by low interest rates. The cheap money brought blossoms to light such as dividend payments financed by bonds (Apple) or share buybacks instead of investments (various companies). Or simply the flight of capital, in search of yield, into risky assets such as shares.

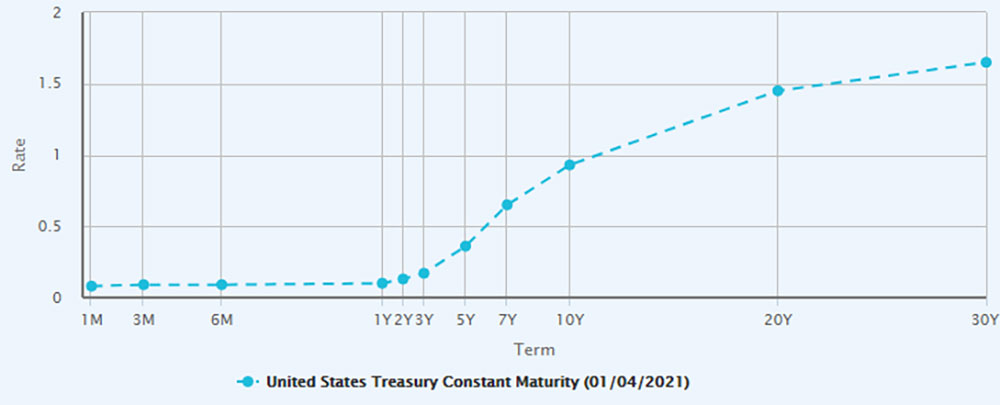

In addition to stumbling blocks, there is a fork in the road here and there. Whether we are close to such a fork will become apparent in the coming months. In addition to the fundamental question of whether interest rates are bottoming out or whether we will continue to see falling interest rates, there are concrete events coming up: A victory for the US Democrats in the Senate (by-elections in Georgia) would give the Democrats the power to tend towards a new edition of globalization. Where Trump has resisted this and wanted to put China in its place, which has been able to emancipate itself during Obama’s term in office, the profiteers of the old, familiar order should be able to gain a foothold again. On the other hand, due to the 2020 elections, the political landscape in the U.S.A. could change sustainably. With Biden/Harris in particular, but also elsewhere, higher government spending would be more likely. And the central banks will continue to buy up bonds vigorously. As a result, they are putting pressure on private buyers, which could put pressure on yields. However, should interest rates rise (emerging inflation, increase in risk premiums), this would be an advantage for the “value” stocks that have been lagging behind the growth stocks in recent years. A steeper yield curve at least should give the financial stocks additional air. Finally, however, not to be forgotten, there is still the run-down economy, where with each week it becomes more difficult to get going again. Many no longer go to work, but are currently still receiving money from the government. Which stumbling block will bring a fall is difficult to foresee. Since the financial crisis, the markets have been able to recover again and again thanks to the supports. Keeping this in mind and still being part of the positive price development is the challenge.