The Navigator provides insight into stock market events with an outlook.

July 03, 2023

«The Magnificent Seven». As with the star-studded Western from 1960, a select few showed the others how it’s done. The first half of the year was characterized by a certain lethargy; the broad market was not quite sure where the journey should go and traded in a broad sideways movement. However, this was different for a few large-cap technology stocks. After the hefty correction of 2022, these stocks recovered, some close to their old highs, and at least lifted the corresponding indices out of the swamp. Thanks to artificial intelligence, although much of it, as so often, still lies in the future. In the present, however, is the fact that the interest rate hikes by the central banks are leaving their mark and the broad market is characterized by uncertainties regarding economic development. Inflation is showing first signs of flattening, but the central bankers are hesitant and state that they will stick to the course of rising interest rates.

Market review

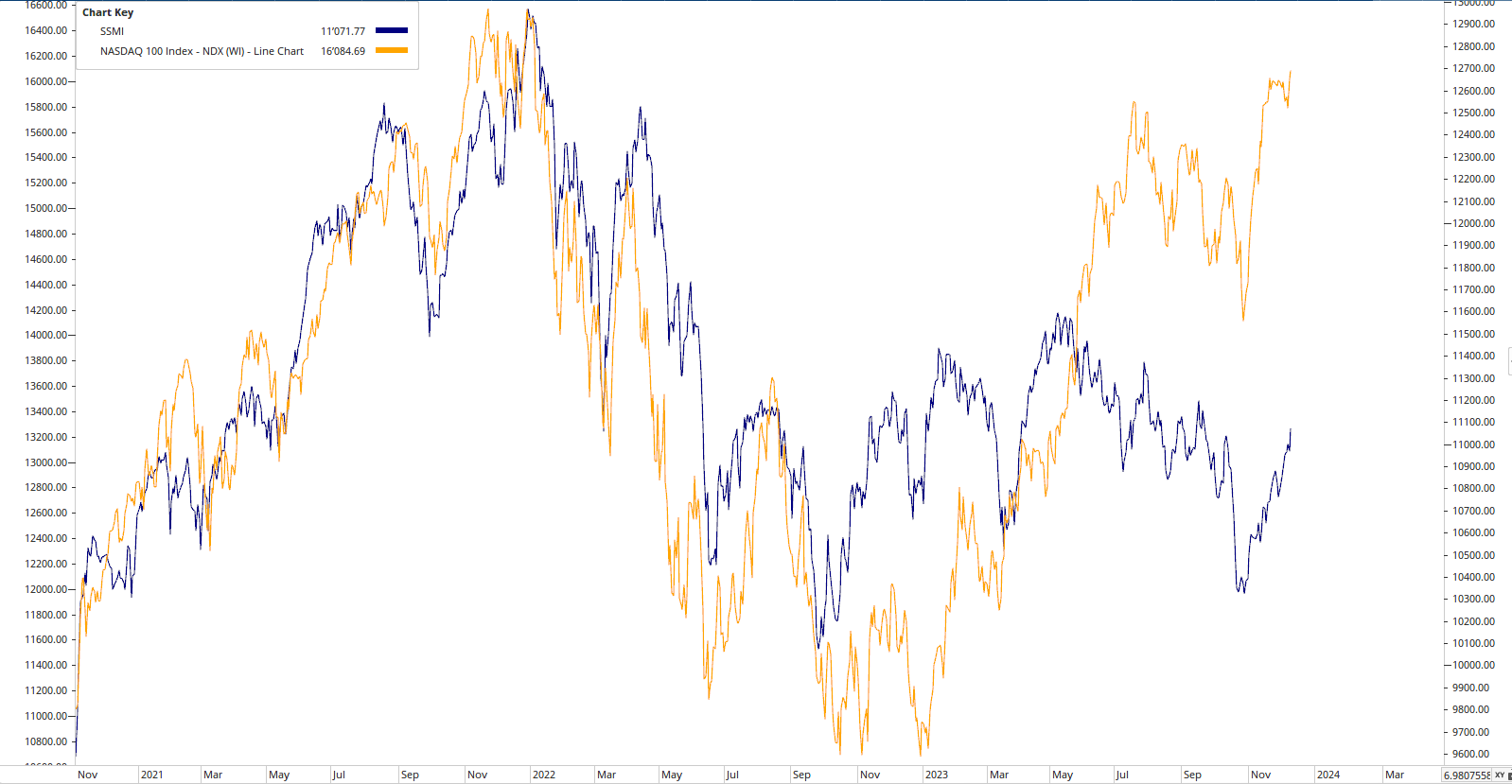

Expectations were there that the markets would recover somewhere after the correction from 2022. Inflation flattened increasingly during the second half of the year and thus the worst could be over – so the opinion. And it happened in this way or similarly, because the stock indices started with verve into the new year – but then corrected again in the meantime. Not so the Nasdaq or the S&P500, which showed a nice recovery due to the strongly positive price development of a few stocks.

SMI vs Nasdaq 100

Most sectors were at least able to stabilize price levels to a certain extent. Only the energy sector fell further back after the strong increases during the Covid crisis. But also the utilities did not get far and again showed weakness.

Overview sectors

For precious metals, gold came close to its old highs. A breakout is near after it has already failed to overcome this (technical) hurdle twice.

In focus

The Magnificent Seven have pulled the markets out of the swamp. The hoped-for recovery has thus occurred, if you look at the index. In many portfolios it may look a little different, be it in a broadly supported Swiss portfolio or in the European context, plus the time window. Because the markets ran in a broad sideways movement with occasional attempts of further slumps. The feat of these few titles helped to turn the sentiment Schluss Amend. Or perhaps it was simply the realization that inflation is coming back a bit and interest rates should not rise too much. In any case, it seems that capital has found its way back into the stock market, although the money market has gained in attractiveness. Nevertheless, the first half of the year was an act on the tightrope and who was traveling with a longer-term optics, ran less risk to lose money through the sharp and fast ups and downs.

We are still of the opinion that inflation has primarily resulted from the circumstance of the lockdowns during the pandemic, with simultaneous continued payment of wages or wage replacement. If there were no government, we would be stuck in a deflation. As described in earlier Navigator articles, we will probably see more of the same: The governments (and society) still have money to redistribute it further, to spend against credit and thus to clear the upcoming problems for the time being. We therefore expect lower interest rates, due to the weakening inflation, and higher price quotations in the medium term.

Outlook

The central banks are sticking to the pace of fighting inflation with higher interest rates. This, although there is a risk that the record high as well as record fast increase in key interest rates will leave skid marks in the economy. The labor market, one of the most important indicators for this handling, still shows little signs of flattening. But the details in the data collection show that not all that glitters is gold and not all data are correspondingly conclusive with the conclusion drawn so far. We would not be surprised if, if not in the coming half-year, then at the beginning of 2024, inflation weakens again and interest rates are not raised further or even lowered. However, inflation or interest rates are unlikely to fall back to the level before Covid, due to the aforementioned tendency to distribute money on the part of governments. As Paul Krugman commented in an article in the Wallstreet Journal, a higher basic level of interest rates is to be expected, also because the economy will increasingly produce locally in the region and thus investments after decades away from the focus in software and intellect, should switch to production facilities and infrastructure. This requires a higher demand for capital, which is likely to make the price, the interest rates, tend to be slightly higher.

“Either we find a way, or we make one.” Hannibal

EDURAN AG

Thomas Dubach