The Navigator provides insight into stock market events with an outlook.

“What goes down must go up”. The stock market boom is getting on in years, and this year’s weak phase has not yet been able to break the existing upward trend.

Recovery in the 2nd quarter

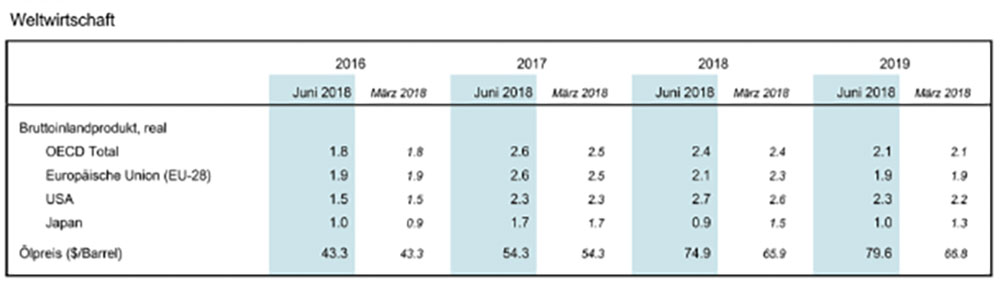

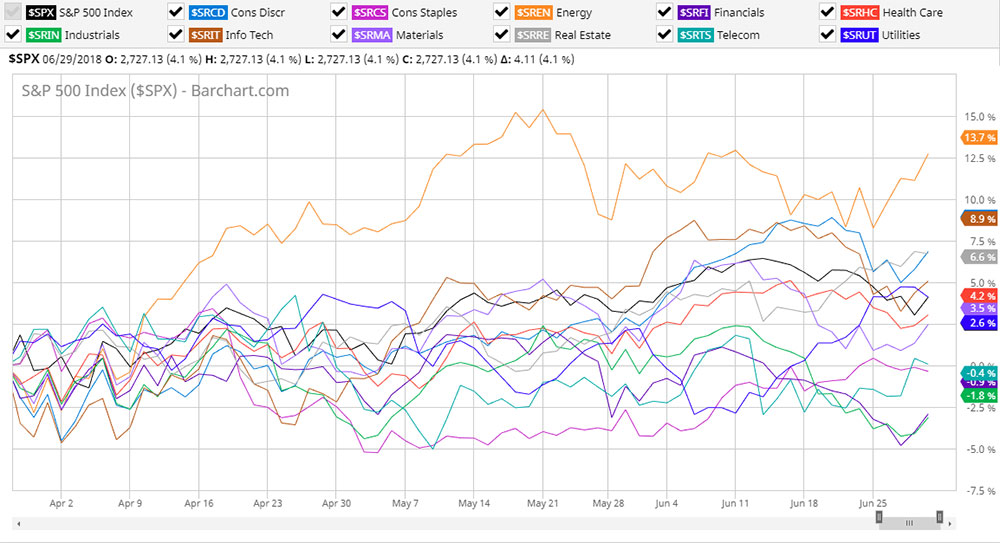

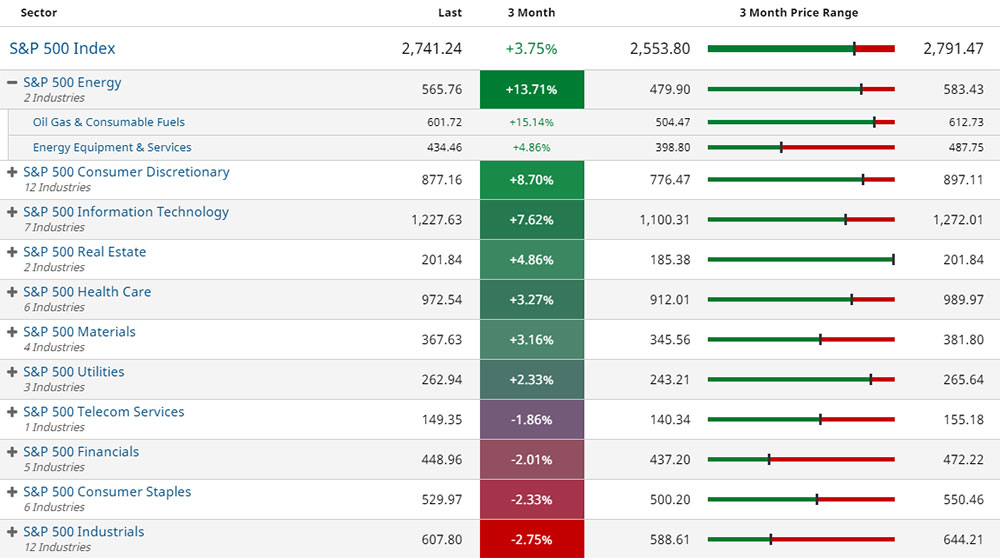

The markets were able to recover from the lows of the first quarter. However, there was a lack of strength or momentum to catch up with the old highs across the board. Exceptions are, for example, the Nasdaq 100, where technology stocks were able to stage a strong rally. On the other hand, the Shanghai 100, which has only known one direction since the beginning of the year: down. Generally speaking, the fundamentals are still intact. The global economy is doing well, even if growth is likely to be somewhat slower in the second half of the year after a strong expansion. The latest developments in global trade, where punitive tariffs are weighing on individual sectors and companies, are having a dampening effect. China is suffering as the trade barriers come at a time when the Chinese economy is already experiencing a slight dip in growth. Exports to the USA account for around 3% of China’s gross national product, and the punitive tariffs could cost up to 0.5% of this. A trade war is underway, some predict. But perhaps everything will turn out differently, as the aim – as also announced by President Trump – should be the lowest possible tariffs for all and fair global trade. The temporary tightening is intended to get China to allow a level playing field for everyone. In the US, companies have received a noticeable boost from tax cuts and business-friendly policies. Europe is also worried about the increase in protectionist measures, especially the German automotive industry.

Interest Rates

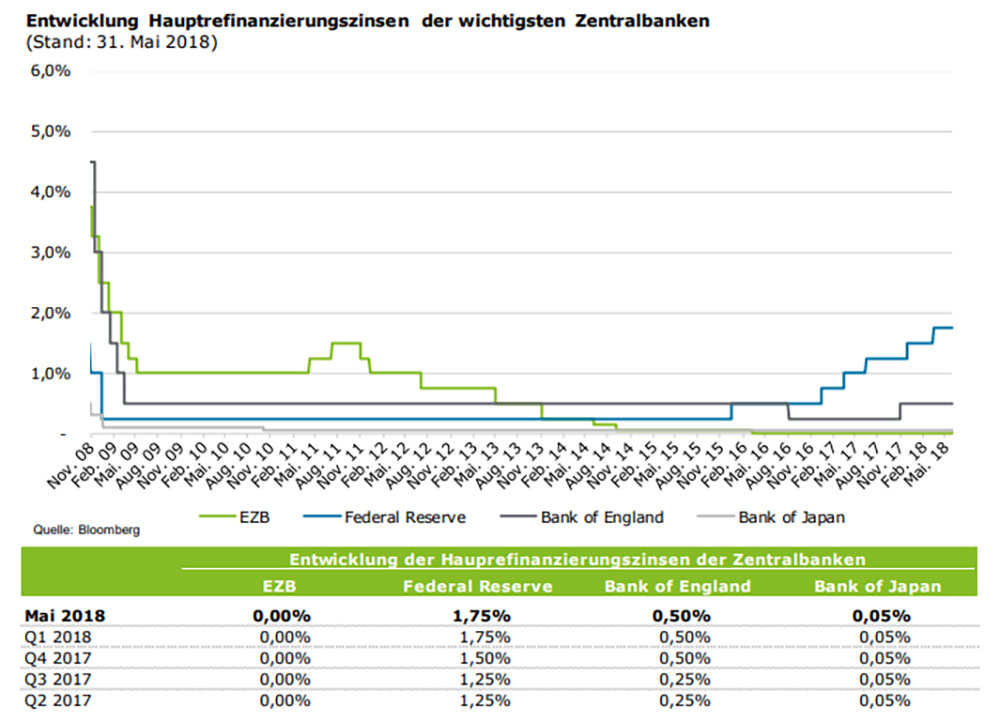

When it comes to interest rates, the focus is still primarily on the US Fed. The course is clearly set for further interest rate hikes as long as the economy is doing well and, above all, as long as the stock market is doing reasonably well. The central banks, and the Fed in particular, want to prevent a potential crisis emanating from the financial markets. With the US economy doing well, the Fed is the most advanced in terms of raising or normalizing interest rates. The US dollar has already gained ground, which in turn could cause problems in the emerging markets. There is a question mark over whether much consideration will be given to emerging markets. The ECB, on the other hand, is sticking to its current position and said at its most recent meeting that key interest rates could be expected to remain at this current level “at least until summer 2019 and in any case for as long as necessary to ensure that inflation developments are consistent with our current expectations of a sustained adjustment”.

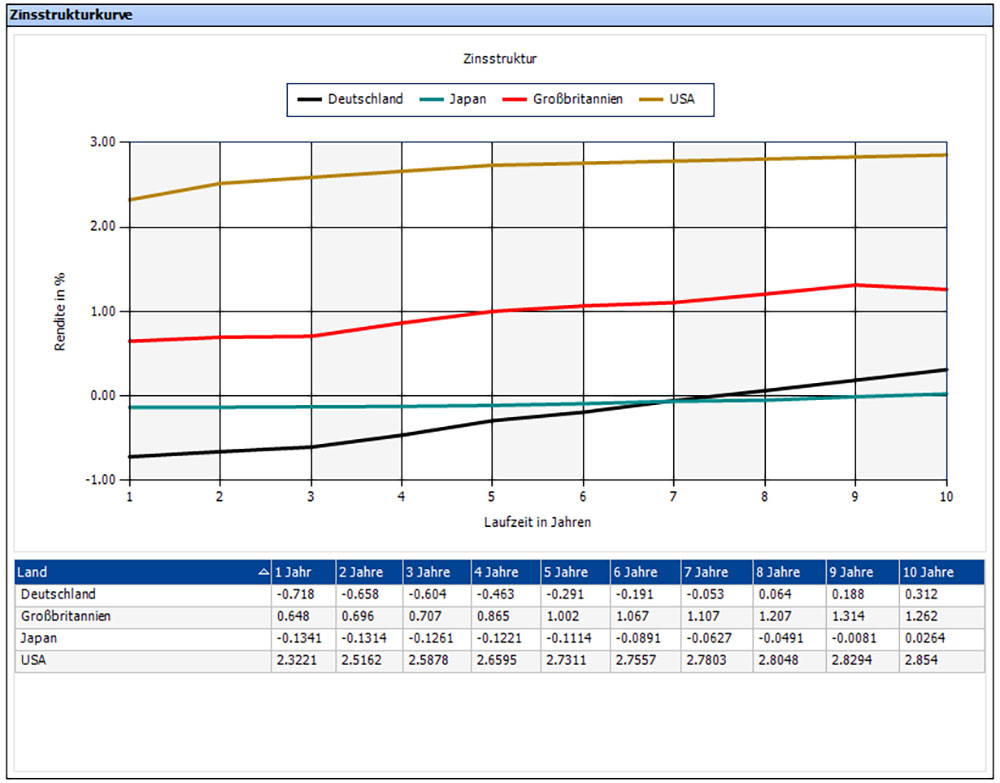

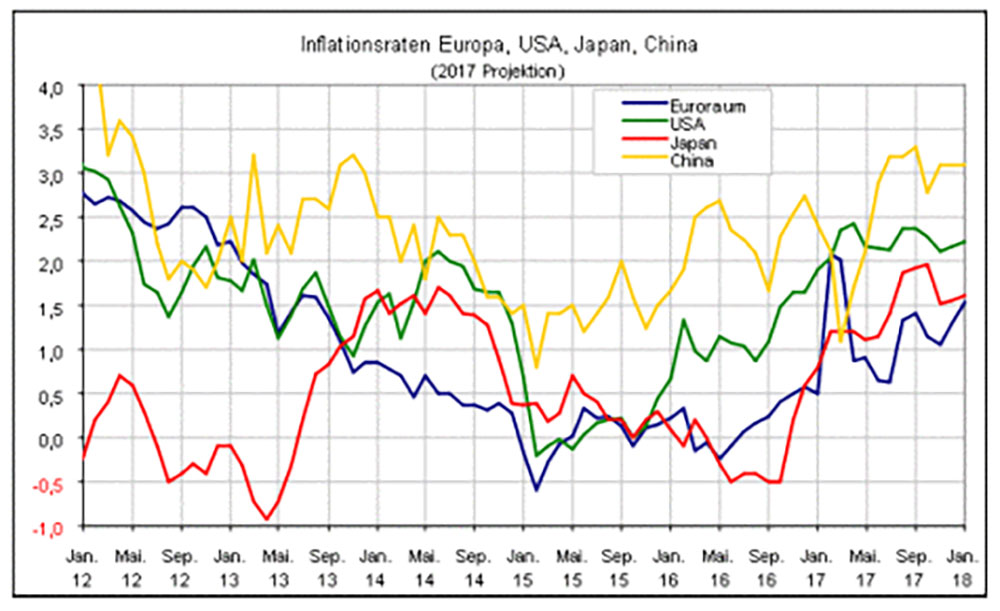

The development of inflation will therefore remain at the center of attention in the future. Bond yields have risen globally due to higher inflation expectations and rising real yields. This is not surprising in the context of an improving economy. The USA is probably at the center of this focus due to its advanced stage in the economic cycle.

To date, inflation figures have regularly fallen short of the central bank’s expectations. When and whether this will change remains to be seen. Inflation is likely to pick up, albeit only slightly (rising wages, low unemployment rate, etc., favor rising incomes/prices). There are also voices predicting that inflation will spiral out of control due to the extremely loose monetary policy, but perhaps somewhat less so than a few years ago. As mentioned here at earlier points in time, there is little or nothing on the markets to suggest any noticeable inflationary potential for the time being. Interest rates and the yield curve at the long end are at a similar, flat level.

Companies / Sectors

With interest rates on the rise and inflation being watched with suspicious eyes, some investors are also considering switching investments from one sector to another.

Not much different from the previous first quarter, consumer goods and cyclical stocks generally made gains. Technology stocks were also among the winners – after a brief but sharp correction. Momentum in technology stocks picked up again strongly towards the end of the quarter. Energy stocks, which have been benefiting from the rising oil price for around a year, are also new. This sector has been badly battered in recent years and there has been a shakeout on the supply side.

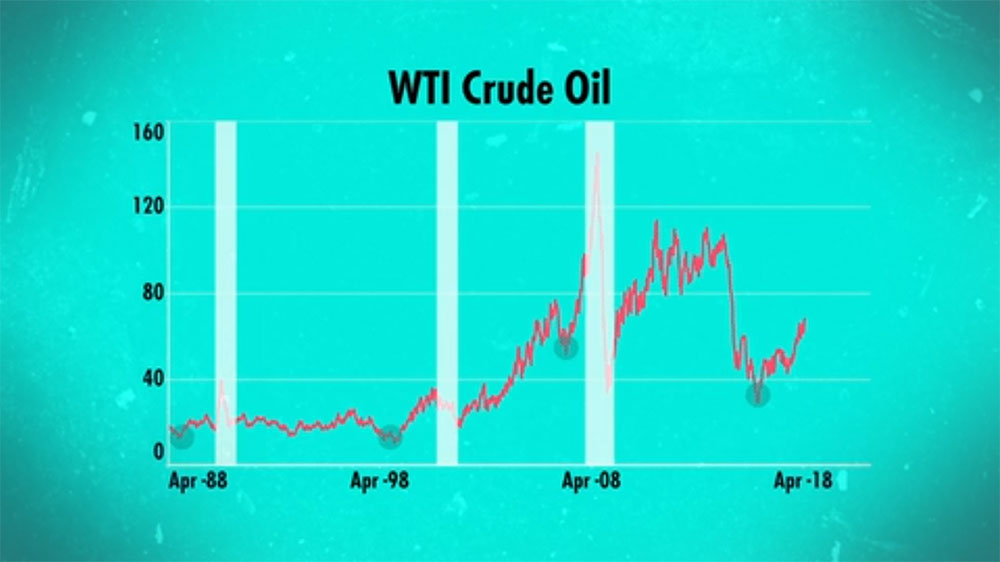

The industry can live well with an oil price of over USD 60 since the beginning of the year and investors have rediscovered it to some extent after months of avoiding the sector. Many doubt whether the price will remain at this attractive level in the long term. One observation also shows that when crude oil has experienced a noticeable price increase after a temporary low, in the past there has been an economic slowdown around 1-2 years later.

Market technology

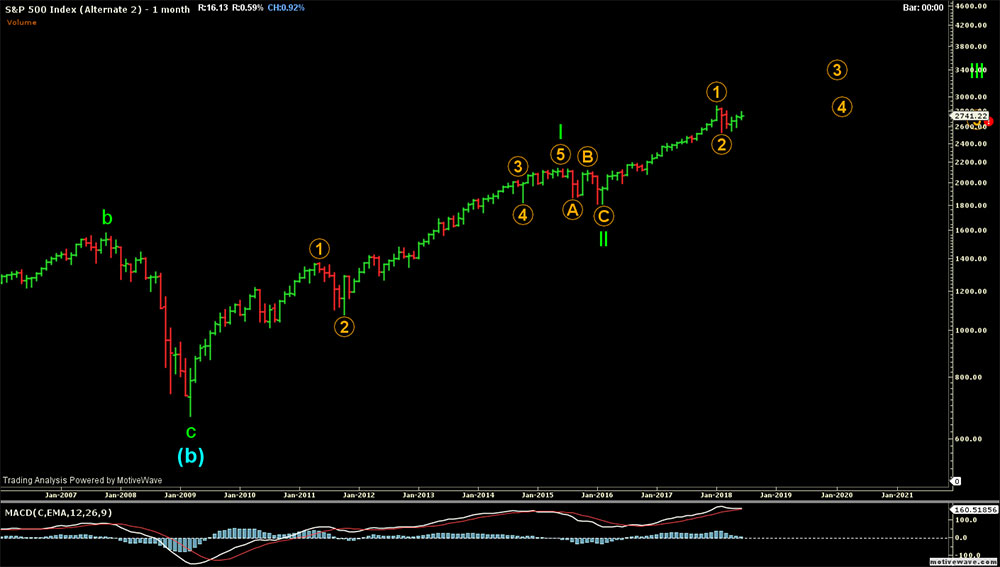

The majority of markets started to correct again towards the end of the second quarter. The impression is that the markets are at a crossroads. From our point of view, there is a good chance that the upward trend will pick up speed again. Whether the correction is already complete will only become clear in the coming days or weeks. If the markets break through the envisaged support lines, momentum is likely to break out to the downside. Market technicals aside, the structure with still few attractive investment opportunities (low interest rates) continues to speak in favor of equities.

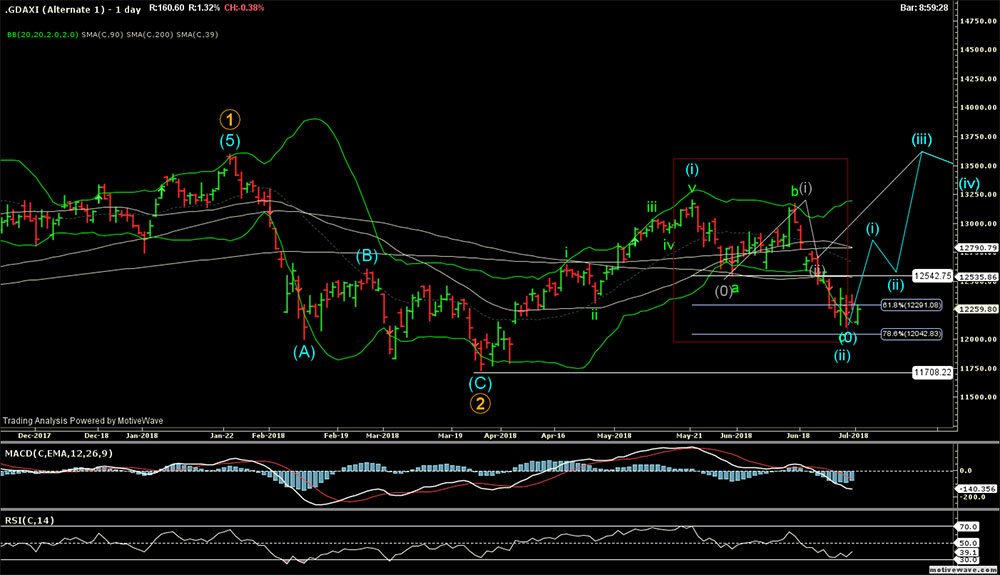

In the DAX, the correction that occurred in the first quarter seemed to be over for the time being. We doubted this version and expected a second wave down. The break came with the new (interim) low on June 21 at around 12540 points. The next important support zone is between just over 12000 and 12290, the most important below that would be at just over 11700. For the time being, it remains to be seen when the correction phase will be completed.

Outlook

The recent correction has brought some nervousness back to the markets. The high valuations and in some cases rather thin liquidity are contributing to this. However, the option premiums and credit spreads in particular show that the generous availability of liquid funds in the search for yield has so far prevented risk premiums from widening. The rise in interest rates is slowly releasing some of the air. The central banks intend to leave the markets to their own devices again, despite all the caution. But only as long as everything goes well: in the event of difficulties, they would return to the old waters and the central bank(s) would intervene to support the market, according to the tenor. The US Fed has a new chairman in Mr. Powell and, statistically speaking, the stock markets will return a negative return for the first six months of a new chairman. Seen in this light, the current correction fits well into the picture. In terms of policy, there are no significant differences to be seen. The term of ECB Chairman Mario Draghi expires in October 2019 – there will certainly be a lot more to read about possible successors. In general, we expect volatility to increase and, together with the structural upheaval that is underway, our focus will be on these issues in the medium term.

EDURAN AG

Thomas Dubach