The Navigator provides insight into stock market events with an outlook.

With just a few days to go until the turn of the year, it is a pleasure to look back on the performance of stock markets around the world. 2017 was a surprisingly good year.

The MSCI ACWI gained around 20%. The markets in Europe slightly less with the SMI 14% and DAX 15%. The USA was slightly stronger at around 25% (Dow Jones). The MSCI Emerging Markets and Nasdaq 100 were the high-flyers with gains of over 30%, while the FTSE 100 (U.K.) was at the lower end of the spectrum with 5%. Broader stock market barometers had a harder time, with smaller-capitalized companies generally posting lower gains than the large caps.

The markets were mainly driven by a combination of low interest rates and an improving global economic situation. A perfect environment – “goldilocks” times, so to speak.

Interest Rates

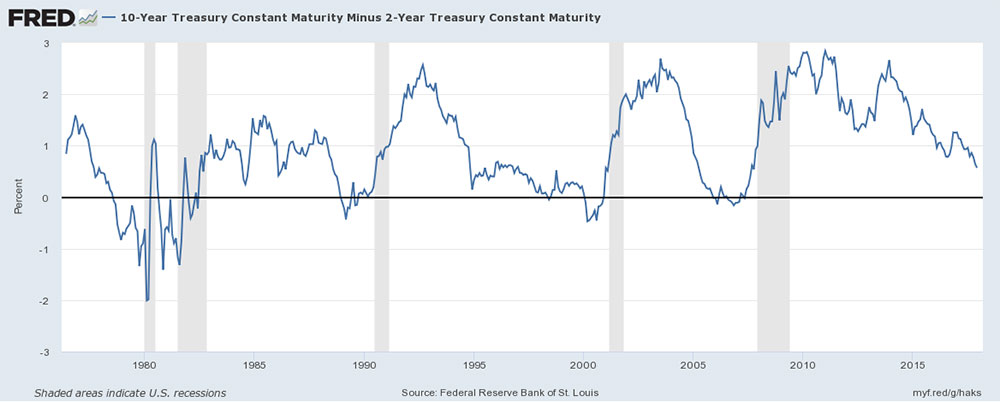

After years of falling interest rates, there was a reversal towards the end of 2016. In 2017, yields on 10-year government bonds moved sideways. Interest rates rose at the short end. This led to a flattening of the yield curve. The announced reduction in the US Federal Reserve’s balance sheet and the less aggressive expansion by the European Central Bank are tending to lead to a further firming of interest rates at the short end. There are many reasons why long-term interest rates have remained at current levels: on the one hand, there are no signs of a noticeable rise in inflation and, on the other, the market still seems to have doubts about the growth variant.

Another noteworthy circumstance is the central bank activity of recent years. The massive intervention of central banks in the price discovery process means that the yield curve no longer reflects the usual market forces in unison (the ECB, for example, holds bonds worth more than EUR 2 trillion, which is more than the entire national debt of Germany, Europe’s largest economy). New regulation has also forced certain market participants, such as the insurance industry, to buy bonds even if they do not generate income (government bonds, which are classified as risk-free). In view of ever-increasing public sector debt, one could also speak of financial repression. The private sector has also taken on additional debt, and in the case of listed companies, money borrowed was also used to buy back shares. Debtor quality has deteriorated in recent months.

In the past, a flattening of the yield curve (2-year yield compared to the 10-year yield) has led to corrections on the equity markets with a certain time lag but with good reliability.

It remains to be seen whether everything will be different this time. The central banks will probably want to try to bring interest rates back to a “healthy” level that is in line with growth. The states, on the other hand, would have to release money, i.e. implement reforms so that more money flows into the economy and into investments and does not disappear into bureaucracy and expanding social welfare systems. The lack of investment and the loss of interest income will have a negative impact on future growth.

The company

According to the OECD, the global economy is expected to have grown by around 3.5% in 2017 (revision from 3.3% in March 2017). The global economy is expected to grow by around 3.6% in the new year. The majority of companies were able to increase their profit growth in 2017. For the most recently reported third quarter, profits rose by an average of around 8.5% year-on-year. Almost three quarters of the companies in the S&P500 Index were able to beat analysts’ estimates. The price/earnings ratio for the next twelve months (Q3 17 – Q3 18) is around 18.5, which is above the long-term average of around 16. The coming months will show whether the nascent economic upturn will gain or lose momentum. Forecasters are positive about the future in this respect and the “Goldilocks” are expected to continue for the foreseeable future.

Broken down by sector, technology stocks had a good few months, followed by basic materials and industrials. Classic defensive stocks such as healthcare, consumer staples and telecoms struggled somewhat more in 2017. However, November saw a small rotation, with the more defensive stocks mentioned above catching up. In the coming months, the pharmaceutical sector should still be able to make gains in the medium term, while energy also has upside potential. In the US, the tax reform could support the cyclical sector and smaller capitalized stocks. Defensive stocks should be bought in the event of weakness.

Looking ahead to the new year, the commodities sector also looks promising. Overcapacities have decreased (primarily in the metals sector, crude oil as a special case with OPEC reduction) and demand is good. Compared to the broad equity market, commodities are at low levels compared to the early 1970s or late 1990s. Gold mines – especially the smaller and medium-sized capitalized ones – are among our favourites.

Market technology

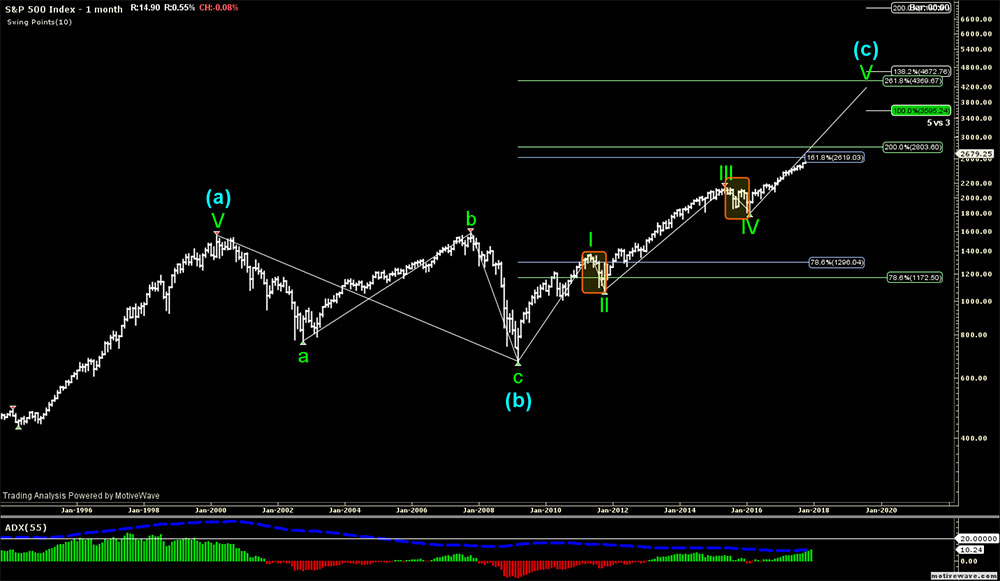

Various sentiment indicators point to a positive mood. Whether euphoria is already present may be doubtful. Looking at the charts, the S&P 500, for example, is increasingly encountering resistance and support (Fibonacci levels) in the 2615-2875 range as well as at around 2600 and 2550 (50 and 90-day moving averages). We see further accumulation of resistance between 3300-3700. These ranges, at the latest the latter, signify the end of the current uptrend.

Generally speaking, the markets still have good momentum, but could correct (or consolidate) a little in the short term as they tend to be somewhat overbought.

Bottomline / Outlook

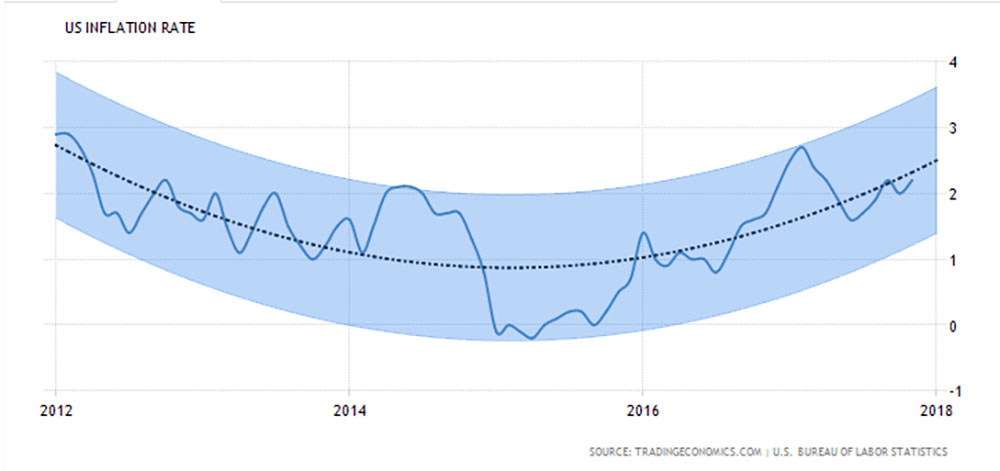

What can be seen as a crystal ball is actually a frozen soap bubble (picture at the beginning). Stock markets are relatively expensive, but given the current environment, this situation could continue for some time. We are still focusing on equities, albeit with as conservative an approach as possible. Fixed-income securities are likely to become more popular again in the coming months as interest rates rise slightly (especially USD and selectively). With the weakening USD, inflation in the US could also pick up (plus tax reform). This would make the central banks’ balancing act even more difficult and the stock markets could be caught on the wrong foot.

There are also other potential stumbling blocks that we see for the coming months. On the whole, we would not be surprised if volatility were to pick up again. With our medium to long-term strategy, your investments should be able to weather turbulent times as usual and benefit from them in the longer term.

We wish you good luck, good health and many happy hours in the New Year!

EDURAN AG

Thomas Dubach