The Navigator provides insight into stock market events with an outlook.

September 28, 2018

“Take a break”. The markets were able to continue their upward trend across the board. Individual stocks or even sectors have corrected noticeably in the meantime.

Continuing the upward trend

Across the board, the markets were able to continue their positive performance. The MSCI World Index gained around 5% over the quarter. This was mainly thanks to growth stocks, where the Nasdaq 100, for example, gained around 7%. On the other hand, the emerging markets suffered from the strengthening of the USD against the domestic currency. These countries have more than tripled their debt in the last 10 years or so (whereas the industrialized countries have increased by around 25%). Turkey also made headlines, with major capital outflows. In the meantime, the MSCI Emerging Markets lost around 4%.

The punitive tariffs have continued to be the focus of attention, with new threats and countermeasures. We believe that the US sees the whole story as a means to an end and ultimately has free trade as its goal, with comparably long spikes for everyone in trade terms. From this perspective, our focus is more on interest rate developments and, as a consequence, on the USD.

Interest Rates

The US Federal Reserve seized the opportunity and, in line with its announcements, raised interest rates for the third time this year before the end of the quarter on September 26. Four more are to follow by the end of 2019. The Fed is making clever use of the opportunity because the ECB and the Bank of Japan are continuing to provide sufficient liquidity to ensure that there are no bottlenecks in the US either. Next year, the screw will also be tightened in the eurozone – by which time the US should have virtually “normalized” its central bank rates at 2.75-3%. Nothing has changed in the trend towards an ever flatter yield curve (USA). Even if everything or at least some things are supposed to be different this time than in the past, a flat yield curve will sooner or later lead to an erosion of profit margins. If not the free economy itself, then the question is what means – also outside of interest rate policy – should be used in future to steepen the yield curve again. We will probably only be able to comment on this in future Navigator reports.

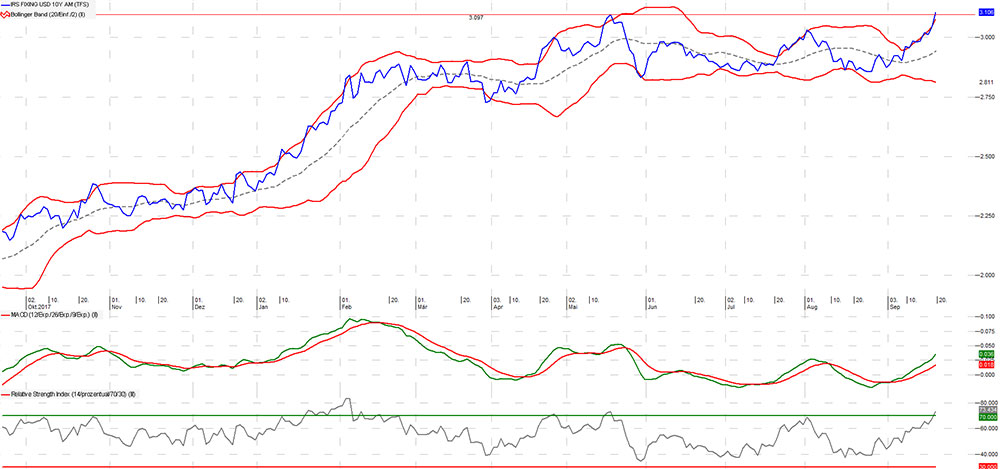

The yield on 10-year US government bonds made a fresh attempt towards the end of the quarter to leave the 3% hurdle behind (at around 3.1% as resistance). The die has not yet been cast in this respect. If the capital markets are to be believed, interest rates are unlikely to rise much further. Technically speaking, however, the 3.3% threshold could lead to a possible adjustment of positions.

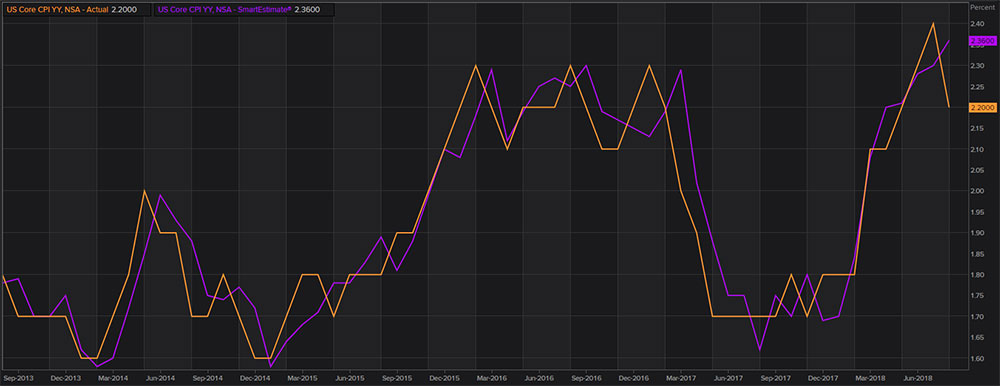

In the US, inflation has picked up speed since 2015 and continued to do so in the past quarter, albeit at a somewhat flatter rate.

Companies / Sectors

Broken down by sector, healthcare stocks were able to regain the ground they lost in the first half of the year. The same applies to industrial stocks and technology shares. The latter were a talking point, as some well-known stocks were subject to major fluctuations. Facebook, for example, lost around 19% on July 26, the largest single-day loss ever recorded for a company on the stock exchange. The day before, the company announced that profit and revenue growth were likely to be slightly lower in the second half of the year.

Another company, Tesla, also made a name for itself when CEO and co-owner (19.7%) Elon Musk announced on Twitter on August 7 that he was considering delisting the company. The share price was very volatile over the quarter. On August 7, it came close to its all-time high from September 2017, only to find itself around 30% lower on September 7, again close to this year’s low from April. Netflix is another well-known tech stock that has lost some ground and now offers hope of regaining (almost) its former strength.

In Switzerland, too, there were some rather sharp corrections: around 1/5 of the stocks in the SPI corrected by 10% or more. This again included companies that had revised their growth prospects downwards. Or simply those where the thin liquidity could not withstand the profit-taking (see also Spotlight article from September 18, 2018 in the blog). Some of these, such as Hochdorf, could soon find some ground.

Mining stocks also tended to be on the solid side in some cases. We have also been focusing on gold mining stocks for some time, preferably those with low levels of debt. In this quarter, they were able to post nice price gains. Oil stocks have also gained interest.

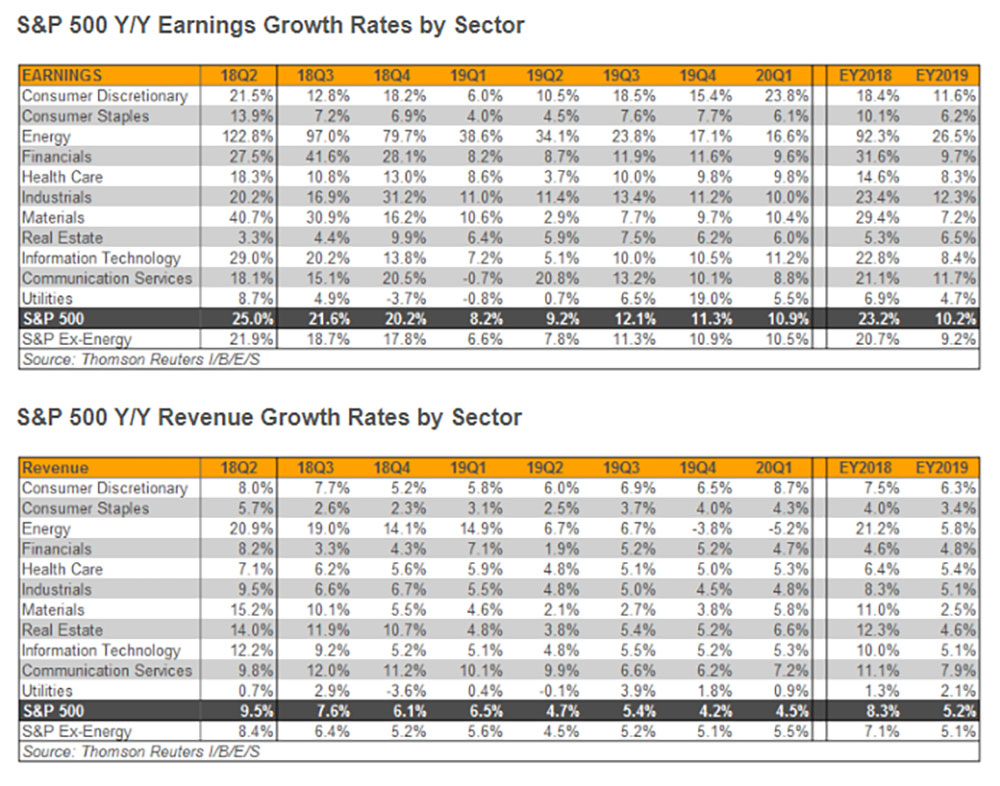

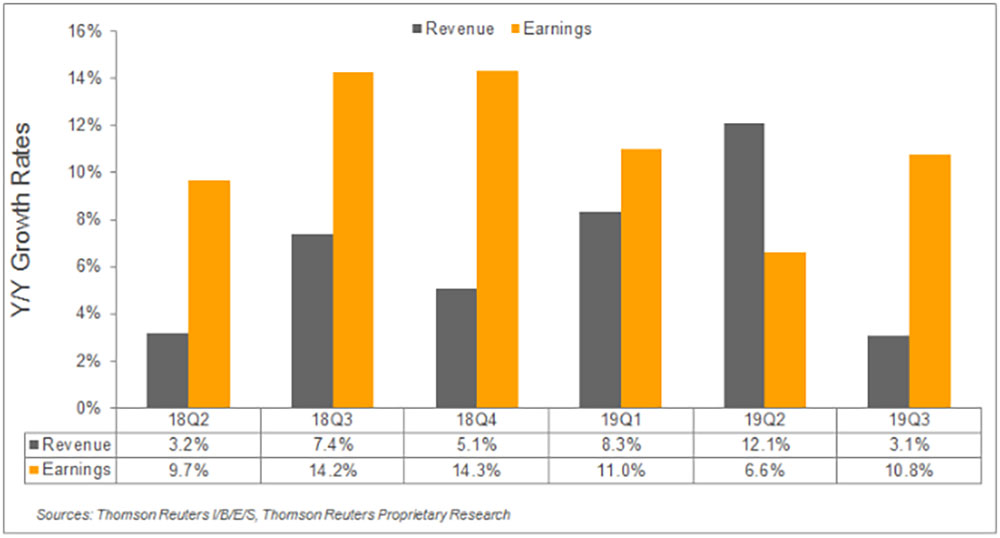

In general, solid growth figures are needed for further share price gains, especially in an environment of rising interest rates. Expectations were and remain high. Slightly lower profit growth rates are expected for the STOXX 600 Index from next year onwards, but higher sales growth rates for the first half of the year. It remains to be seen whether the companies can deliver here. The air may become a little thinner for some.

Market technology

There is not much to report at the index level. The market technique continues to show an upward trend that is still intact but is getting on in years. Since the 2008/09 crisis, the broad market has repeatedly undergone correction phases, including a smaller one this spring.

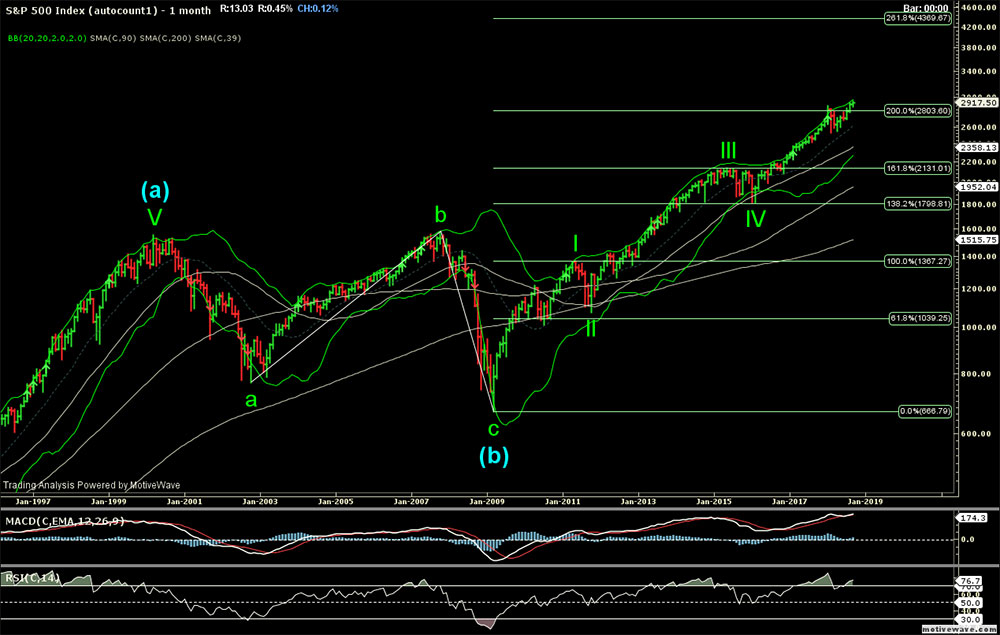

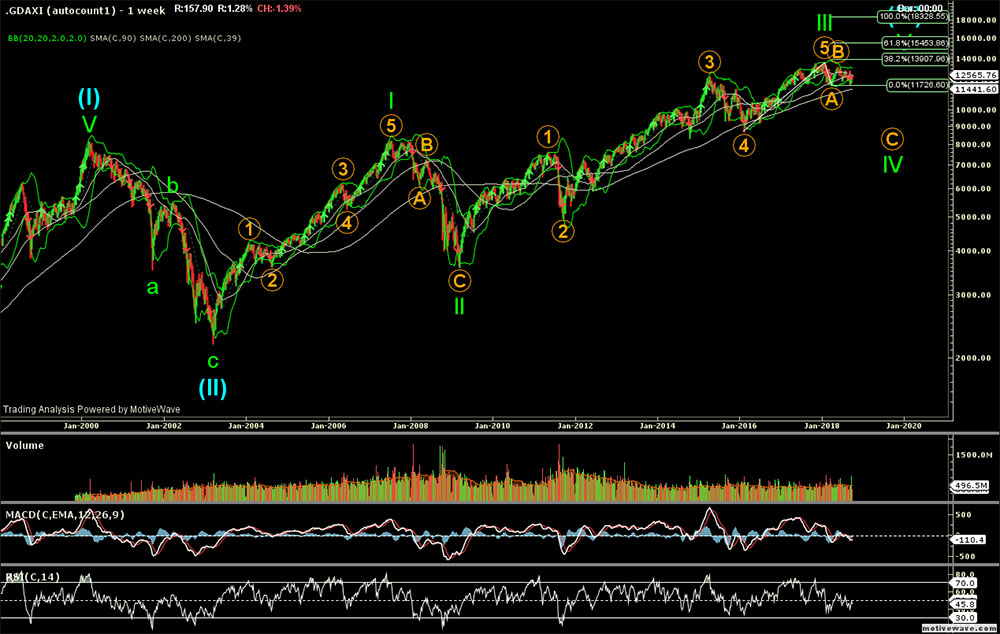

It should be noted that the regions have experienced correction phases of varying intensity this year. The German share index still does not appear to be fully out of the consolidation phase, whereas its American counterpart is already on the elevator up to the next level.

Individual sectors and stocks have partly corrected sharply or are still in correction mode. Technically, there is room upwards, also with the support of those stocks that will soon come out of consolidation.

Outlook

In principle, both are possible given the current state of the markets: the upward trend continues or we soon slip into a bear market. We favor the first option in advance. The US (S&P500) already completed its correction in the spring and has since made a new all-time high. The German stock index, on the other hand, is probably still in a correction phase, which should be completed soon (it also has lower valuations than the US). Currencies are once again likely to tip the scales (or show the flows) and herald the next movement on the equity markets. Globally, however, we are getting closer to the possible end. The question is whether this will be around 2019 or a few years later. The US Federal Reserve already announced last Wednesday that it would react to market turbulence or an impending recession by cutting interest rates. Risk premiums are likely to rise further overall because rising interest rates will cause more debtors to falter and because it will become increasingly difficult for companies to keep their earnings figures on track after years of cost savings and share buybacks.

We are hoping for a year-end rally (where we could also realize some profits again). A lot can still happen before then, but we want to remain confident.

EDURAN AG

Thomas Dubach