The Navigator provides insight into stock market events with an outlook.

28.12.2018

“Nice mess.” October has ushered in the fourth quarter and has once again lived up to its reputation as a dangerous stock market month.

Necessary correction

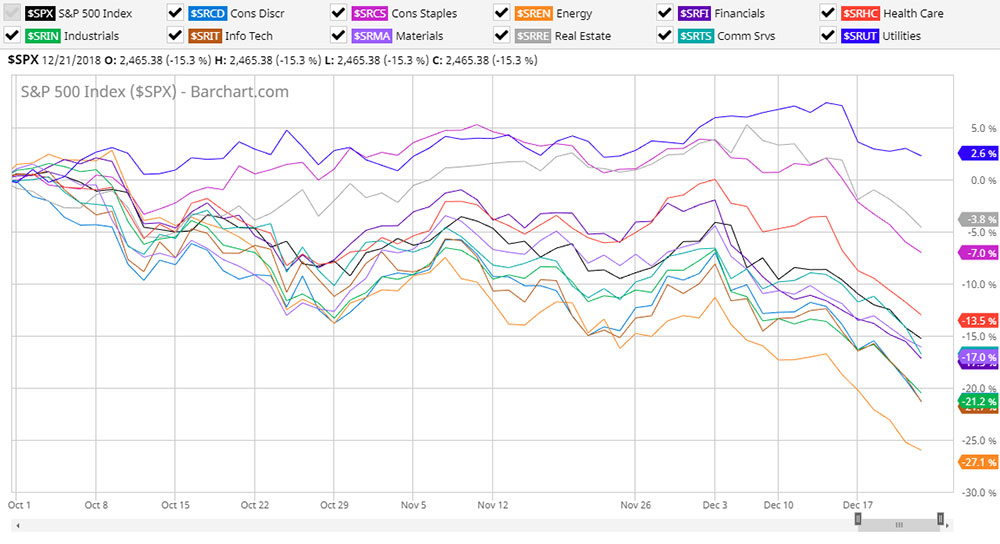

Throughout the quarter, the markets have primarily done one thing: corrected. After a wave of selling had already rolled in during the first quarter of 2018, the correction in the fourth quarter was immensely more severe. The only sector that came through unscathed was utilities.

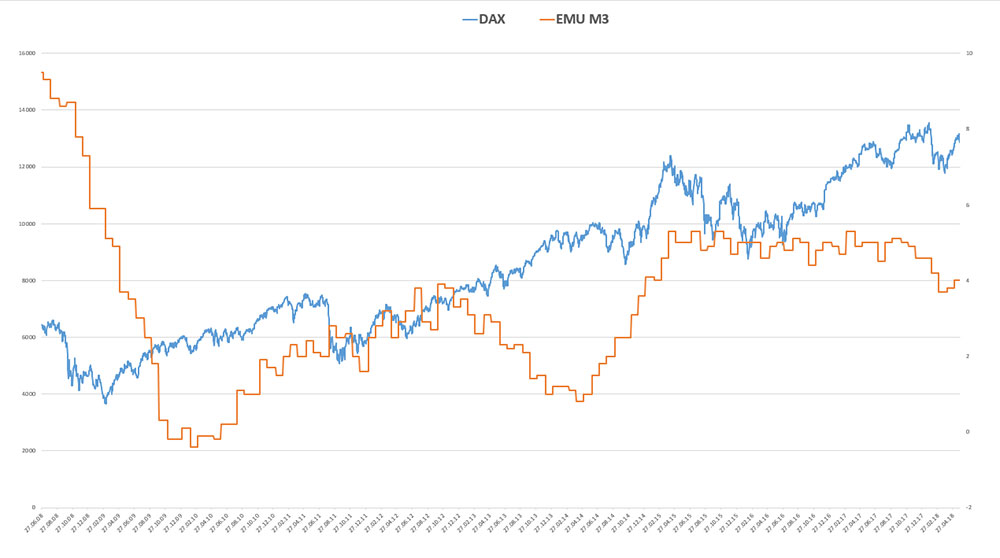

In our opinion, the theme of this last quarter for the year was the tightening liquidity. And along with the no longer favorable valuations, the correction was necessary. The reduction in bond purchases by the ECB (EUR 15 billion per month) implemented at the beginning of October took some of the pressure off the financial markets. At the same time, there was a pause in share buybacks for US companies that entered the blackout period in the first half of October. Both together probably tipped the scales so that the markets could collapse right on time with the start of the dangerous stock market month of October.

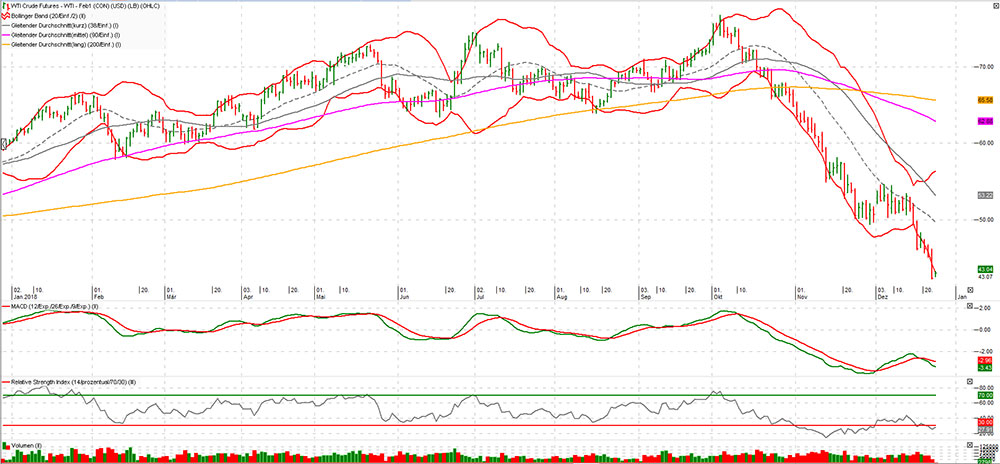

The oil price has also corrected and interrupted its rally that started a year ago. With the US sanctions against Iran, it was assumed that the supply could become scarce. However, the gap has been filled by other sources such as Russia, the OPEC states and the USA, and with additional growth fears due to trade sanctions, the oil price (futures) joined in the sell-off mood and there was a veritable price crash. On the other hand, the gold price has gained momentum with the tense situation on the stock market. Gold mining stocks should remain interesting, also because they have somewhat stepped out of the focus of the general public over the last few years. Other capital-intensive (industrials) or credit flow-dependent sectors (consumer discretionary) had to accept price losses – probably also due to the focus on tighter financing options. The high valuation of technology stocks has been trimmed.

In summary, it can be said that the market has temporarily made way for a somewhat more negative – also more realistic – view from a previously rather optimistic one.

Interest Rates

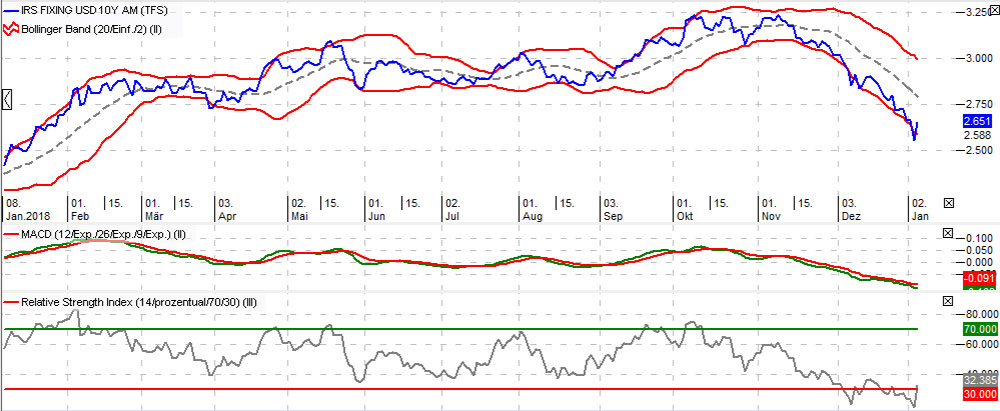

At the beginning of October and in the first half of November, it looked as if interest rates would break out to new highs and leave the resistance mark at around 3.2% (10-year yields on US government bonds) behind. In the meantime, this has turned out to be a damp squib. Yields have fallen below 2.7%. The capital market still sees no signs of rising inflation. This is despite the fact that the unemployment statistics are at a 50-year low, which, according to the Philips curve, should lead to higher inflation (as has already been described in the Navigator).

The world and its economy are reorganizing. The globalization that has taken place over the last decades seems to be coming to a halt and we could be on the way to a tripolar world. The USA is bringing the value chain back home or to neighboring countries, its immediate sphere of influence. China is in the process of expanding the domestic market and is moving away from being the global workshop and will increasingly produce for itself in and for the region. Europe is mainly concerned with itself, is treading water and is finding it difficult to find a suitable role in this dynamic.

Uncertainties are also likely to persist in the new year. In addition to the political and trade headwinds, the markets are likely to remain all the more volatile.

If the ECB keeps its word, Europe or the euro will catch up on what the USA has already implemented. Bond purchases will be further reduced and interest rates may be raised from autumn 2019.

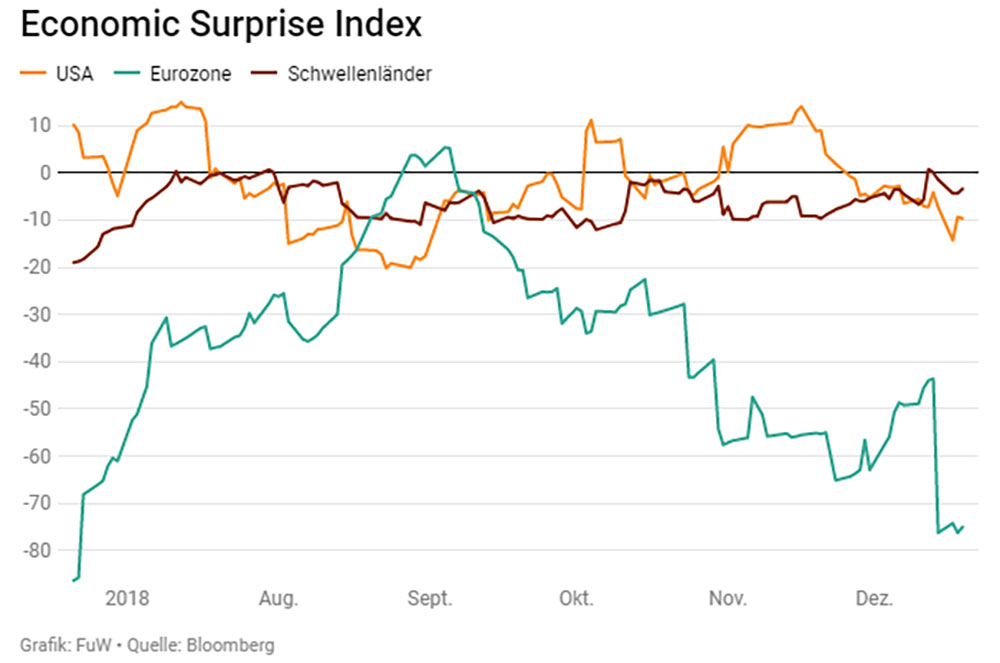

Indicators such as the PMI (Purchasing Manager Index) have weakened, especially in Europe, where the index is as low as it has been for 49 months. The Economic Surprise Index, which compares the data received with analyst estimates, has also turned out lower – again more drastically for the Eurozone than for the USA. What still looked like so-called synchronized global growth at the beginning of the year is no longer the case. Whether the central banks, including the ECB, will adhere to the timetable for a “normalization” of interest rates will have to be seen under the aforementioned conditions.

Also not to be disregarded is a certain sensitivity of the central banks with regard to the financial markets (financial stability risk), because a major crash can, as last seen in the crisis of 2008/09, negatively affect the real economy.

Companies / Sectors

The 4th quarter was eventful. Small-cap stocks and growth stocks tended to be among the biggest losers. Profit-taking after quite strong increases for the last months as well as thinned-out liquidity led to partly drastic corrections. Even if there was no Christmas rally, the gift is all the greater for those who have created or maintained liquidity early on and or generally have the means to buy something at more favorable valuations.

Various euphonious names are currently on special offer. Sectors that are ahead of the overall economy, such as the chemical industry, have already corrected sharply over the year and are presenting themselves at current levels with reasonable prices.

Market technology

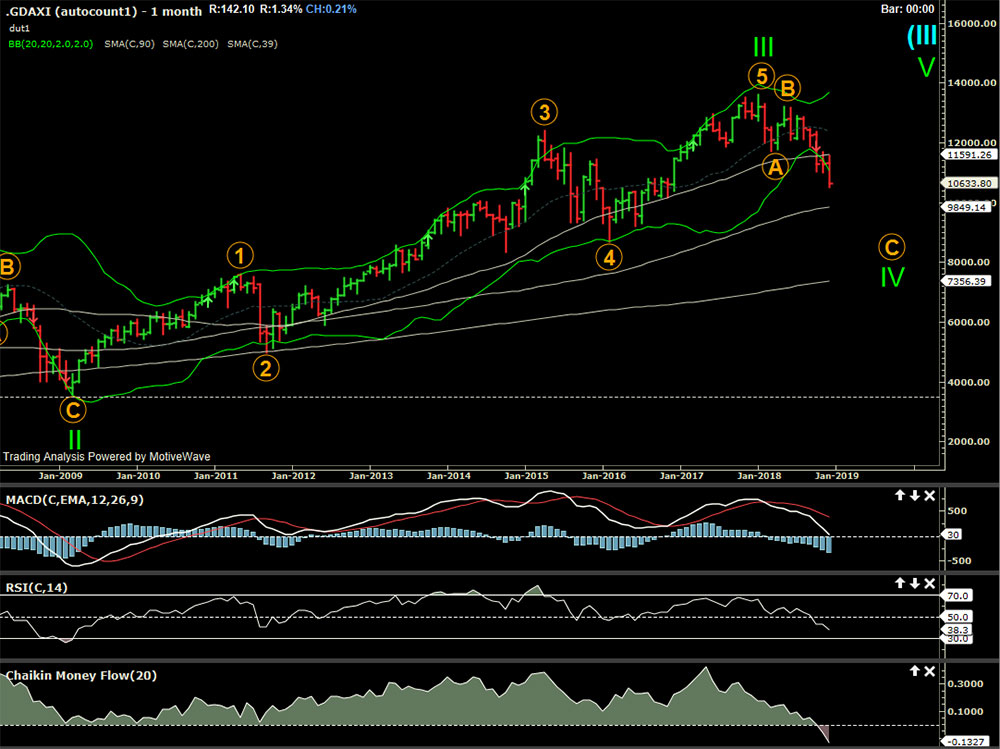

2018 was marked by the correction, but the overriding upward trend is not likely to be over yet. A few important support lines have been broken and it can be assumed that the correction will continue for a while. Whether this will run sharply downwards or rather sideways remains to be seen.

Over the year as a whole, the markets were able to recover after the correction at the beginning of the year (end of January to end of March/April), in some cases even reaching new record highs (S&P500). The US stock exchanges have been able to detach themselves from the rest of the world for some time anyway and play their own composition, driven by capital repatriation (tax policy) or quasi-absorbed global liquidity. Broken across the board, the markets are still on course, in an upward trend and currently in a longer-lasting correction. If the downward momentum should increase, the correction could be more severe, but last less long in terms of time. Due to the macro picture with low interest rates and a central bank policy that does not want the markets to crash (or rather: cannot let them crash because of the stability factor for the overall economy), the markets could move into a longer-lasting, sideways-trending consolidation phase (triangle correction).

Individual sectors and stocks have partly corrected sharply or are still in correction mode. Technically, there is room upwards, also with the support of those stocks that will soon come out of consolidation.

Outlook

With the end of the quarter, we can also look back on the past decade since the financial crisis of 2008/09. In September 2008, Lehman Brothers went under and the central banks set interest rates at record lows in crisis mode. With the path taken since the 2008/09 crisis, we assume that nothing fundamental will change so quickly. The central banks are in the process of, or have announced, shortening their balance sheets. Debt has continued to increase since then and the quality of growth is questionable. Whether the announced plans of the central banks can be completed under such circumstances may be questioned.

With the dwindling liquidity, some “market” is coming back, weakly capitalized companies should have a harder time and share buyback programs as well. Valuations would have to be lower overall and increasing volatility is to be expected along the way. But just, everything in a certain frame – because if it becomes too bad, the central bank will probably step in again. Interest rates should still remain low in historical comparison and this in turn gives the shares fundamental support – especially the companies that have healthy balance sheets and intact growth prospects (even if the expectations should not always be met). In our basic scenario, we expect the markets to strengthen again sooner or later, which we will once again use for a certain reduction in equity positions. However, we would continue to keep the equity ratio relatively high, because in times like these with an uncertain outcome (deflation or inflation – equity selection is important!) equities offer good protection for your capital in the medium to long term.

We wish you a happy new year!

Your EDURAN AG