The Navigator provides insight into stock market events with an outlook.

“Yin & Yang.” After two opposing quarters, the stock markets are temporarily finding a kind of inner peace – as good as it gets. The weakened economic growth is putting pressure on interest rates. Gold is breaking out upwards.

Interest rate policy gains

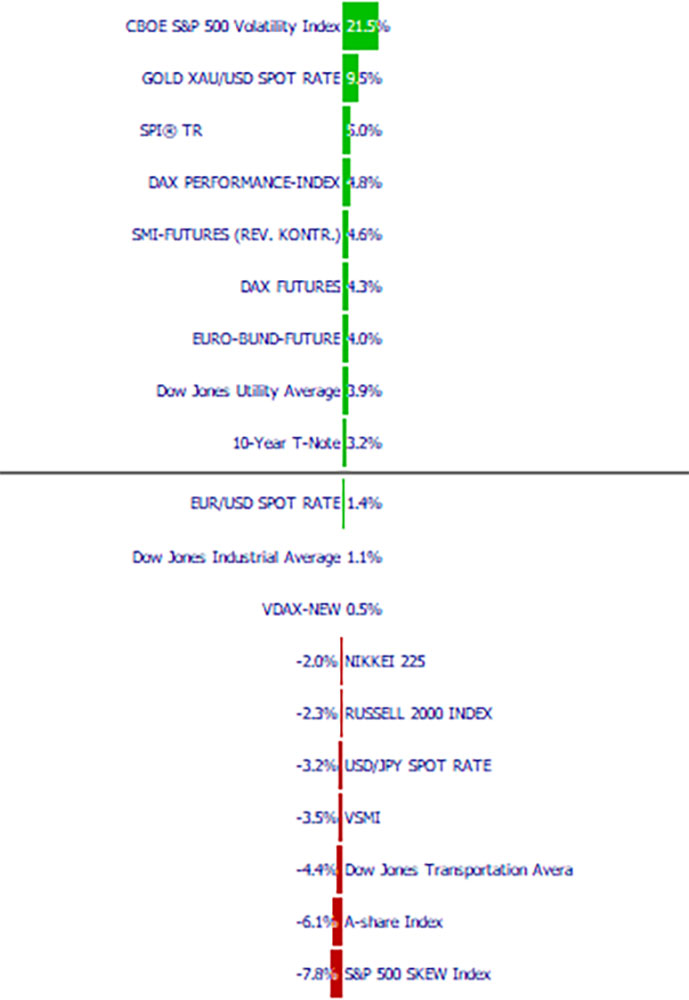

The second quarter was marked by consolidation or – one can also say, by a weakened continuation of the recovery. After two opposing quarters (correction in the 4th quarter of 2018 and rally in the 1st quarter of 2019), the stock markets (index level) are roughly near the level from the end of the 3rd quarter of 2018. Broken down to individual stocks, however, there are striking differences: active stock selection can pay off! Over the quarter, the major indices in particular were able to gain somewhat again under the line.

The broadly based stock indices or those with heavily weighted cyclically sensitive stocks had to give way. Asia, especially China, suffered disproportionately (after an equally disproportionately strong 1st quarter). In terms of sectors, the quarter also delivered – as a result – a mixed picture (see section “Sectors”). Also worth mentioning is gold, which was able to break through the critical hurdle of USD 1350/ounce upwards. The VIX (volatility index S&P500), as well as the German VDAX, was at the end of the quarter again above the 3-year average (the CH volatility index is still noticeably below the 3-year average).

Unlike in the two previous quarters, the balance of power was relatively balanced, and positions have been largely cleared. The bulls and bears seem to have similarly strong arguments. On the one hand, there are the central banks, which have recently turned the script upside down. Further interest rate hikes are being abandoned, and the markets are being prepared for interest rate cuts. The economy has lost momentum. In the short term, growth could be fueled again, because the US presidential elections will take place in a year. It’s the economy, stupid! – President Trump knows that too. The bears, on the other hand, see a progression of the misery: It is to be feared that the profit figures will disappoint, or the expectations have already been revised downwards. In the medium and longer term, the debts are weighing on growth. If interest rates remain at a low level, savers, future consumers and investments are being disserved. Profits or income can hardly be increased, and bankruptcies would increase as a result. Sooner or later, risk premiums would have to rise.

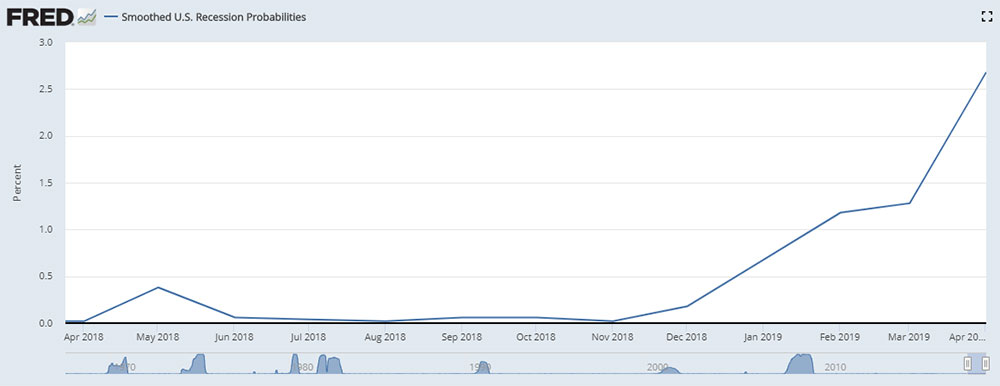

The central banks have the great task of finding the optimal level of monetary stimulus – and communicating this correctly. If the support is too generous, the markets are likely to experience another revaluation. But it could also be, according to the bears, that we are already in a recession and the central banks, primarily the dominant US central bank, are taking back interest rates too little or acting too late. If one examines the leading indicators as well as the development of the latest statistics in general, there are indications of at least a temporary weakness. We will learn the effective numbers and sizes from the statistical offices, but only at a later point in time, as it is in the nature of things.

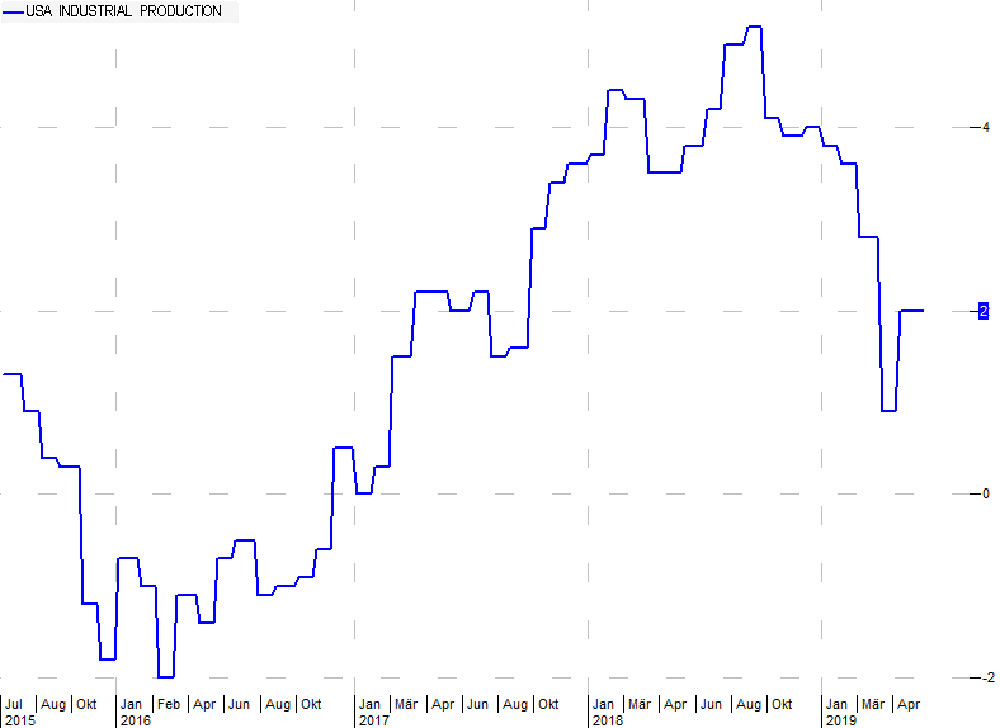

One of these leading indicators is the index of the New York Fed shown above. This index takes into account various factors such as the creation of new jobs, industrial production, the income situation, etc. (https://fred.stlouisfed.org/series/RECPROUSM156N). The weighty industrial production of the USA, for example, has put an end to the previous increase over the turn of the year for the time being.

If in the 4th quarter of 2018 the markets were driven by growth fears and in the 1st quarter of 19 by the interest rate turnaround and a strong recovery in equities, in the second quarter these two forces held the balance to some extent. The position adjustments seem to be completed for the time being. With the breakout in gold, the turnaround in interest rates, the trade tariffs as well as a possible tightening in the various crisis areas worldwide, the temporary calm could soon be over again.

Interest Rates

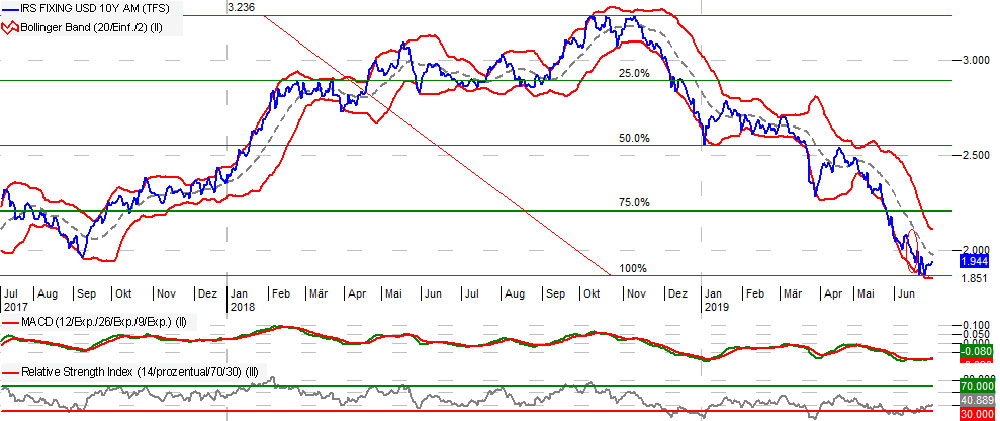

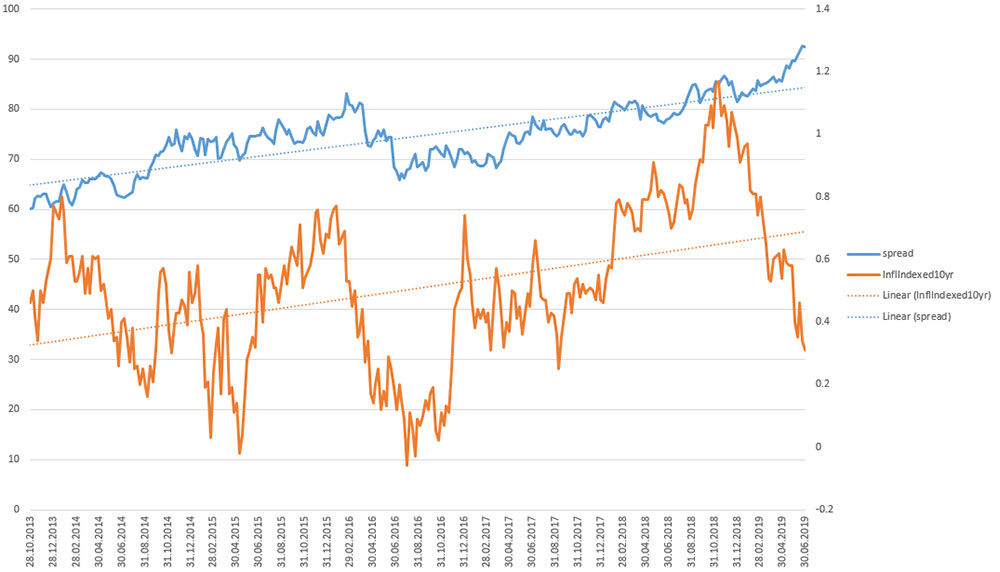

With the increasing signs of a weakening economy, interest rates have consequently come under pressure. Readers of the Navigator will remember the description in the fourth quarter of 2018, when interest rates collapsed along with the emerging growth fears. Since then, there has been a dramatic downward movement, which continued in this second quarter. The yield on ten-year US government bonds fell below 2% in this quarter – one feels transported back to the interest rate desert of 2016.

Or, in other words, the “normalization” of interest rates announced by the central banks – namely the US Fed – is turning out to be a flash in the pan, as of today. After the ECB began to throttle bond purchases in October and, according to the schedule, wanted to start raising interest rates about a year later, in October 2019, some of this is currently being called into question again. The striking difference in the interest rate level between the USA and the EU seems to take place more with a movement of the US interest rates downwards, instead of the euro interest rates upwards (with consequences for the USD-FX). With the low interest rates, the topic of inflation also seems to be off the table for the time being. The low interest rates or the inability to bring the interest rate level close to economic growth (EU) is reminiscent of the situation in Japan and thus of the specter of deflation.

If one speaks about inflation, it makes sense to define what exactly one is talking about. Following the Austrian school, for example, one can distinguish between monetary inflation, asset inflation and consumer inflation. Only asset inflation has taken place so far. The monetary one has so far failed to materialize, i.e. has not yet reached the size targeted by the central banks. Because despite record balance sheet totals of the central banks, the velocity of money has been near the lowest levels since the financial crisis of 2008/09.

Consumer inflation has recently increased somewhat, at least in the USA. Food, for example, has experienced the strongest increase in 4 years. Raw materials have come back slightly, probably also due to the trade war/lower demand from China. With the recent turnaround in the trade war towards the resumption of negotiations, the probability increases that the price level will not rise greatly (the opposite would be a rise in the medium and longer term to be feared).

The big question of inflation or deflation is likely to continue to occupy the markets in the near future. The velocity of money shown above should increase again when the banks are restructured and take on more risks by granting loans. The reality, however, still shows in the opposite direction: In 2018, for example, European banks deposited a record EUR 7.5 billion with the ECB. Recently, for example, the Euribor (as well as the short-term forwards) has also reached new record lows.

Should the economic slowdown consolidate, this could lead to an increase in risk premiums. Due to the low interest rates, many companies (primarily in the USA) with weak business performance and low margins were able to finance themselves well on the capital market. With an economic slowdown, some are likely to get into difficulties, bankruptcies will increase, which will increase the risk premium.

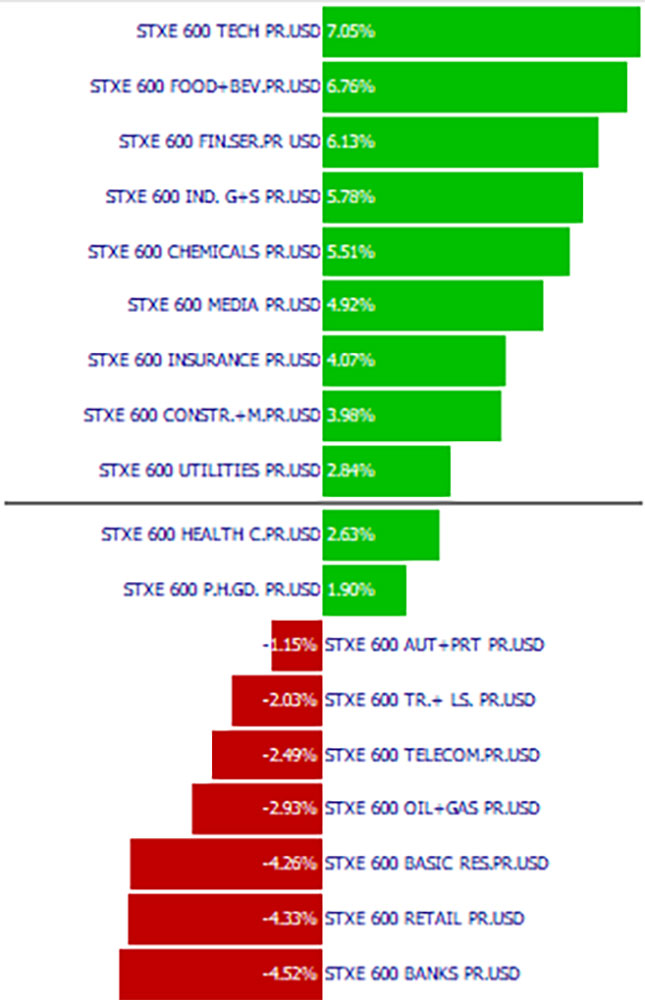

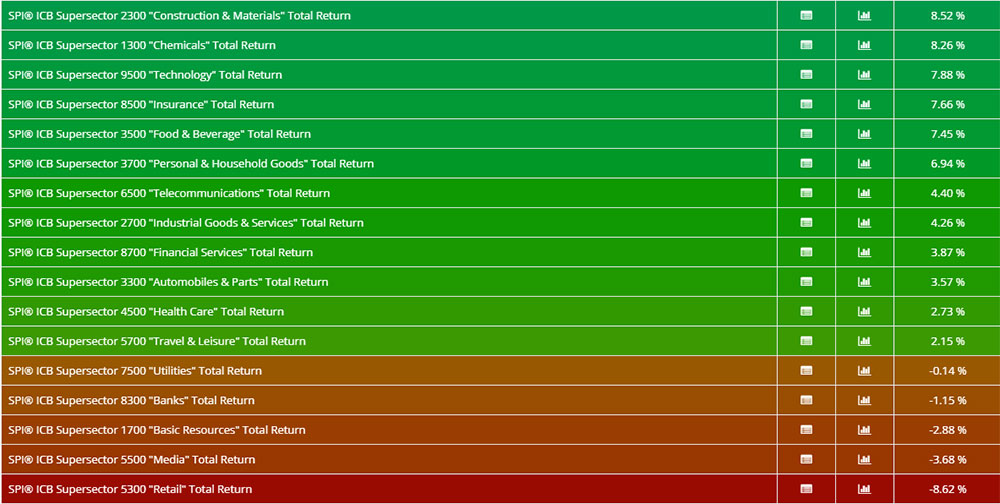

Sectors

The sectors coped differently. The majority was able to gain, led by the technology sector.

The banks – once again – disappointed and have marked interim lows (e.g. Deutsche Bank). At times, the defensive values were able to float on top, due to the economic slowdown. The industrial sector had to deal with growth losses, where the Purchasing Managers’ Index (PMI) fell again a bit further below the critical 50 mark, to 47.6 recently in June. The average value of the PMI in the 2nd quarter is as low as it was last in the 1st quarter of 2013.

The automotive industry, together with the suppliers, were able to gain somewhat, partly reduced to the price, even if the business is tough or still associated with relatively high risks. On the stock exchange, the prices are traded. Thus, in this quarter, automotive suppliers, which had suffered greatly since the beginning of last year, were also able to find ground and partly record price gains.

With the rise in gold, most mines were able to gain, for the time being mostly the large and well-known names. Smaller and medium-sized titles are likely to come into play in a second round – especially those with a solid balance sheet.

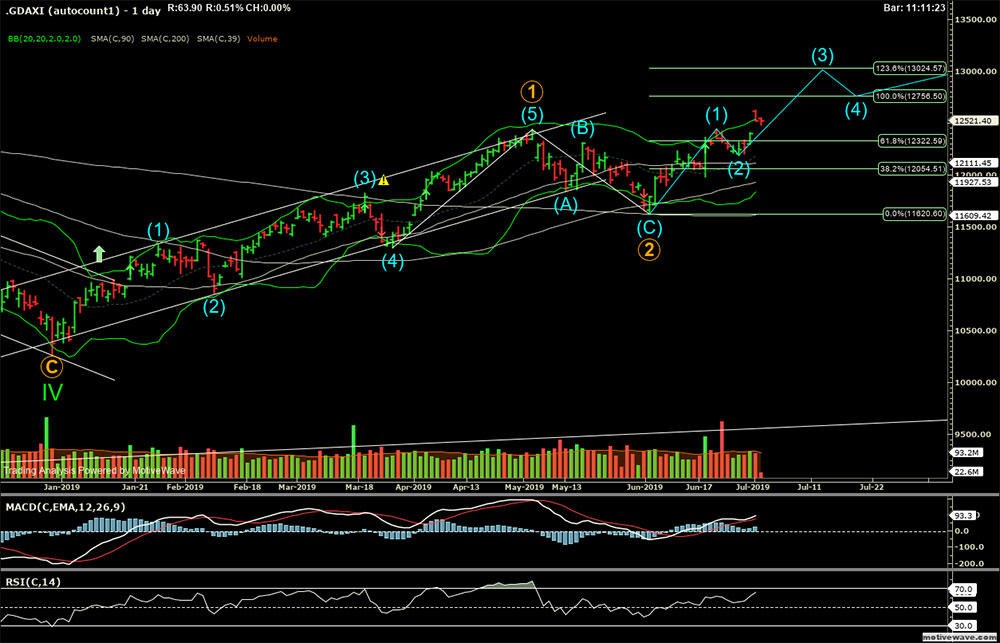

Market technology

The upward trend has remained intact over the 2nd quarter and has even undergone a correction in May. There were repeated dangers that the old lows could be undercut again. However, this has not proven true.

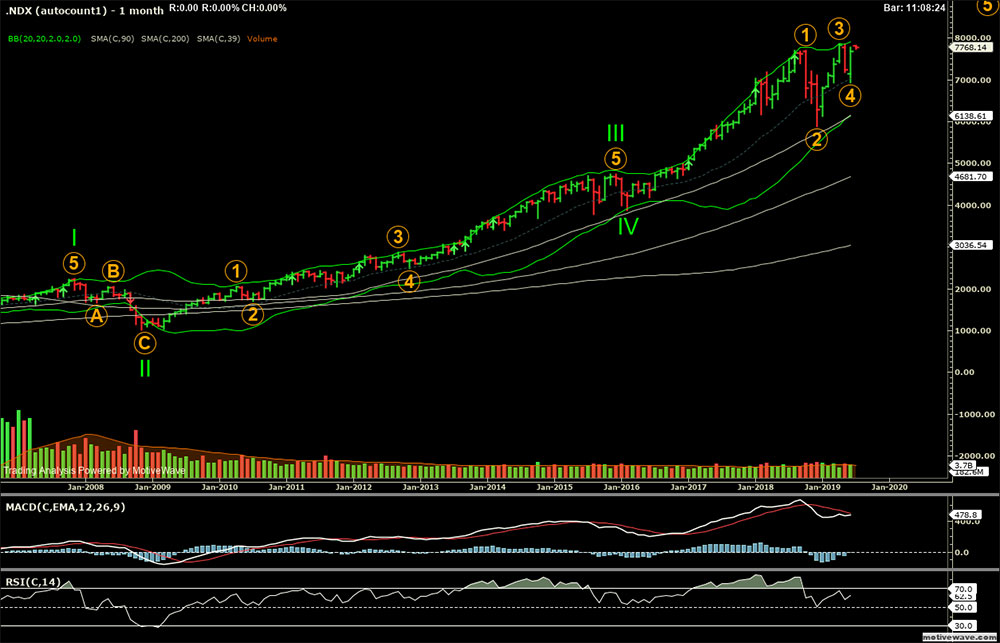

The US markets seem – technically speaking and unlike the European stock markets – to be more advanced and to be in the last phase of the current upward trend. An example is the technology exchange Nasdaq, which represents a part of the large-capitalized US stocks.

There was a significant technical breakout in gold. For years, gold had somewhat fallen out of the focus of the broad (investment) public. With increasing stimulus and ever higher rising stock and asset valuations, more and more well-known fund managers stated that they invest in gold and gold mines. Now comes possibly the next phase, where the general public slowly gets a taste for it again. According to our chart, the current price target should be at USD 1600-1700, stop at 1350/1300.

With the breakout in gold, the ratio of gold to silver is also of interest. The ratio is considered by some observers as an indicator regarding the future inflation development.

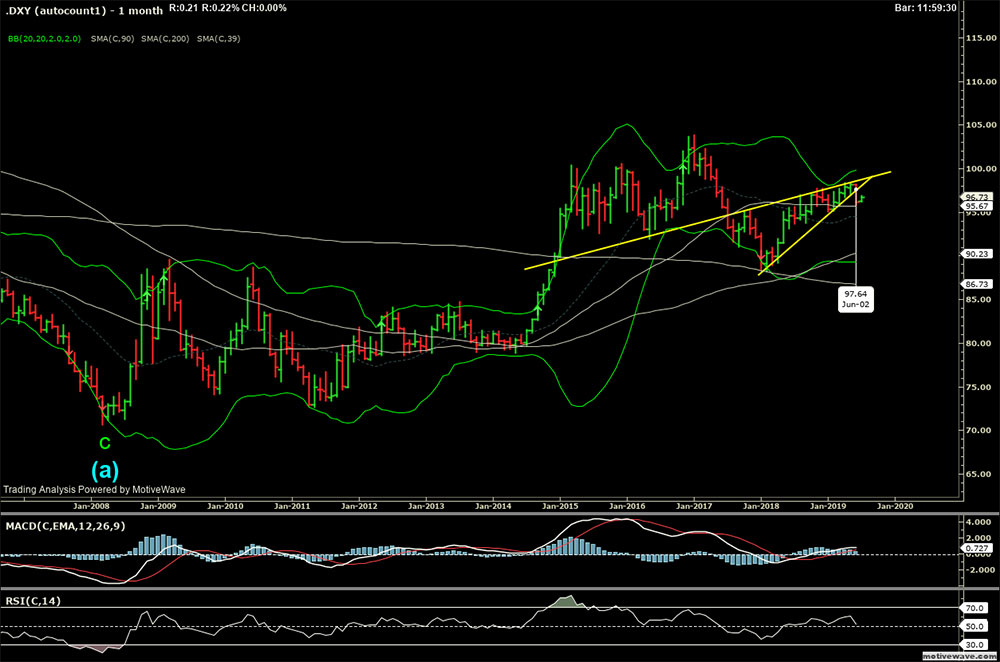

The USD, at least against the basket with the most important currencies (DXY), looks technically battered and should, according to the chart, tend to weaken. However, if one looks at the situation in the markets, especially the indebtedness of the companies, it could well be that the USD will be in strong demand in the next major refinancing round. A record number of around USD 10 trillion in debt has grown over the last decade, almost half of the economic output of the USA. Private households and banks have tended to reduce debt. Thus, two contradictory views, which must be kept in mind.

Outlook

The markets continue to be in the area of tension between the financial stimulus orchestrated by the central banks (positive, but ideally must be reduced in due course) and a battered economy or an economy growing without great dynamics. If the economy weakens, this puts pressure on profits and, as a reaction, the central banks lower interest rates (or try to bring money into circulation in other ways). If the economy is doing well or strongly, so that inflation even rises (Phillips curve), the rising interest rates will put pressure on valuations. A tricky situation. The art is, as generally announced, to be able to manage the balance between increasing economic output and normalization of interest rates. Not enough, at the same time a restructuring of the economy is taking place. Technology as a driving factor will create new markets or market segments or simply turn existing processes upside down. Growth stocks can strategically represent a glimmer of hope. It is important to identify sectors and stocks that benefit from such trends. Here, too, one will be wiser in retrospect and know which stocks and sectors have been the successful ones. Here, too, all the more, disciplined investing with strict risk management is recommended.

The interest rate policy is likely to continue to be decisive, the supporting pillar of the current bull market. It is to be expected that the political pressure on the central banks will increase, even if only in the medium or longer term. For the time being, for example, President Trump wants lower interest rates. In the best case, however, the interest rates will find themselves at a level where savers are not penalized (interest rates in line with growth). As time progresses, the situation is intensifying, but the current interest rate policy can remain in place for some time – in the worst case until the bitter end, a currency revision. With the MMT (modern monetary theory), attempts are made to make debts palatable. In our opinion, however, there is no such perpetuum mobile for almost infinite growth via money printing – not this time either. For our portfolios, all this means that we can continue with our chosen strategy, but begin with selective profit-taking and make tactical reallocations in the equity investments as needed and as the opportunity arises.

Your EDURAN AG