The Navigator provides insight into stock market events with an outlook.

02.04.2019

“New Year – Old Regime.” The first quarter was marked by recovery. Central banks are showing leniency and continue to provide sufficient liquidity.

Rescuer in Times of Need

Following the significant correction in Q4 2018, a counter-movement began shortly before year-end (December 26 for the S&P 500 and December 28 for the Dax), which was expected to last for approximately the next three months. Besides a technically oversold situation, the shift by central banks – primarily the US Fed – back towards a generally looser monetary policy was decisive, especially towards the end of December. Interest rates are likely to continue rising, but more slowly than announced and expected. The markets have understood that if the economy falters or stock markets stumble, central banks will reliably step in as firefighters.

The beginning of the year also allows for a brief review of the past year: A year ago, many economists and market commentators were consistently positive. There was talk of synchronized global growth, and the return of inflation was announced. The US Fed allowed interest rates to rise throughout the year and reduced its balance sheet. Important resistance levels were broken, such as the yield on 10-year US Treasuries, which surpassed the 3.2% mark at the beginning of October. However, things turned out differently. With a clouded outlook for the coming quarters and tightening liquidity, markets turned at the beginning of October (the ECB also began reducing its purchase program).

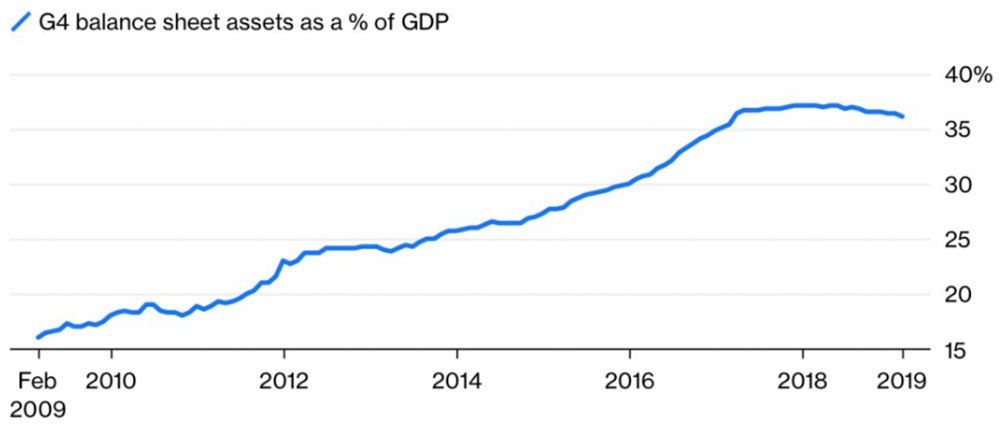

Now we seem to be back in familiar waters: generally low interest rates and central banks that continue to support markets with sufficient liquidity. It is difficult to bid farewell to the monetary stimulus policy initiated in 2011.

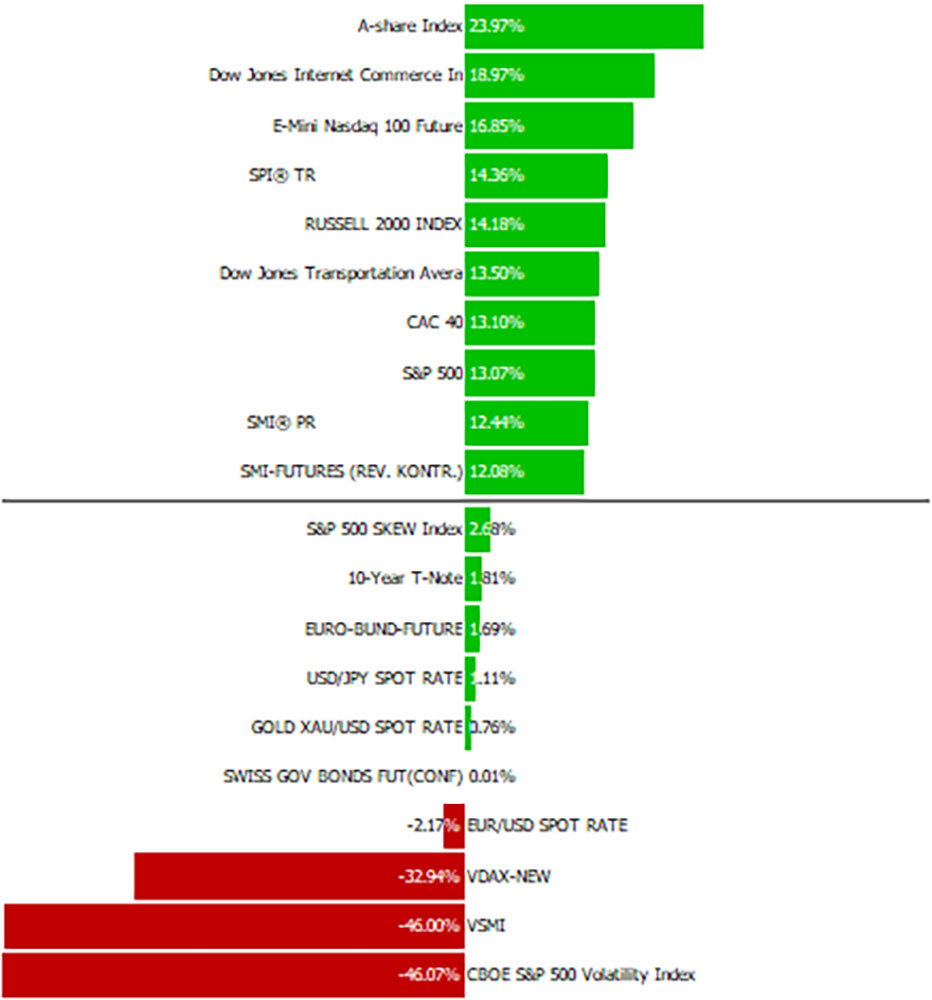

Broken down by region, Asia, with the Shanghai Composite Index, saw the largest gains, approximately 25% for the quarter. This was mainly due to the potentially brightening talks regarding the trade dispute between the USA and China.

US markets also saw strong gains, nearly 20% for the Dow Jones Index, and European markets generally followed with a slight discount compared to the US.

Europe and its export-oriented nations now appear to be more dependent on China and thus feel changes in available liquidity or economic adjustments (including the effects of the trade war).

Interest Rates

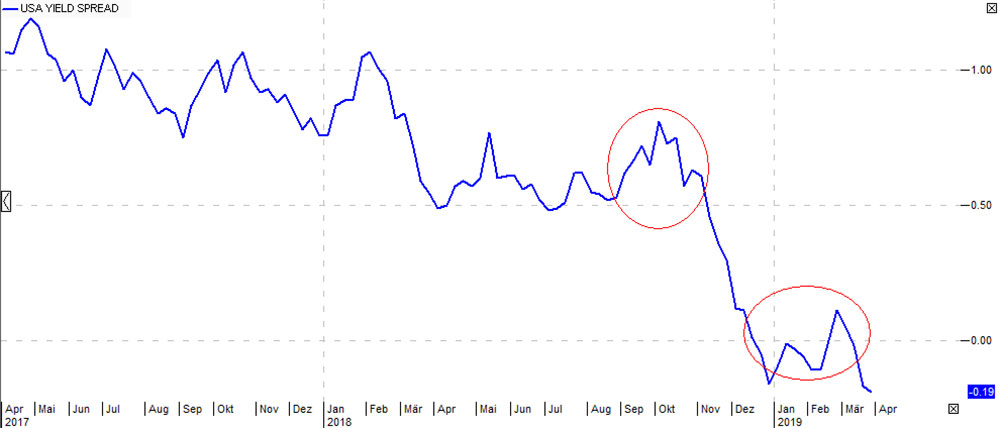

On the interest rate front, there was a further flattening of the yield curve, recently leading to an inverted yield curve in the US. Statistically, such a constellation increases the probability of a recession and a stock market correction.

Markets expect the US to tighten interest rates a bit further, but not much more will come. The remaining central banks are dependent on the US and will tend to provide additional liquidity. Because no one wants a strong currency in an environment of moderate or declining growth. From this perspective, we have a flattening yield curve, but probably still sufficient monetary stimulus, which provides support for financial markets.

Companies / Sectors

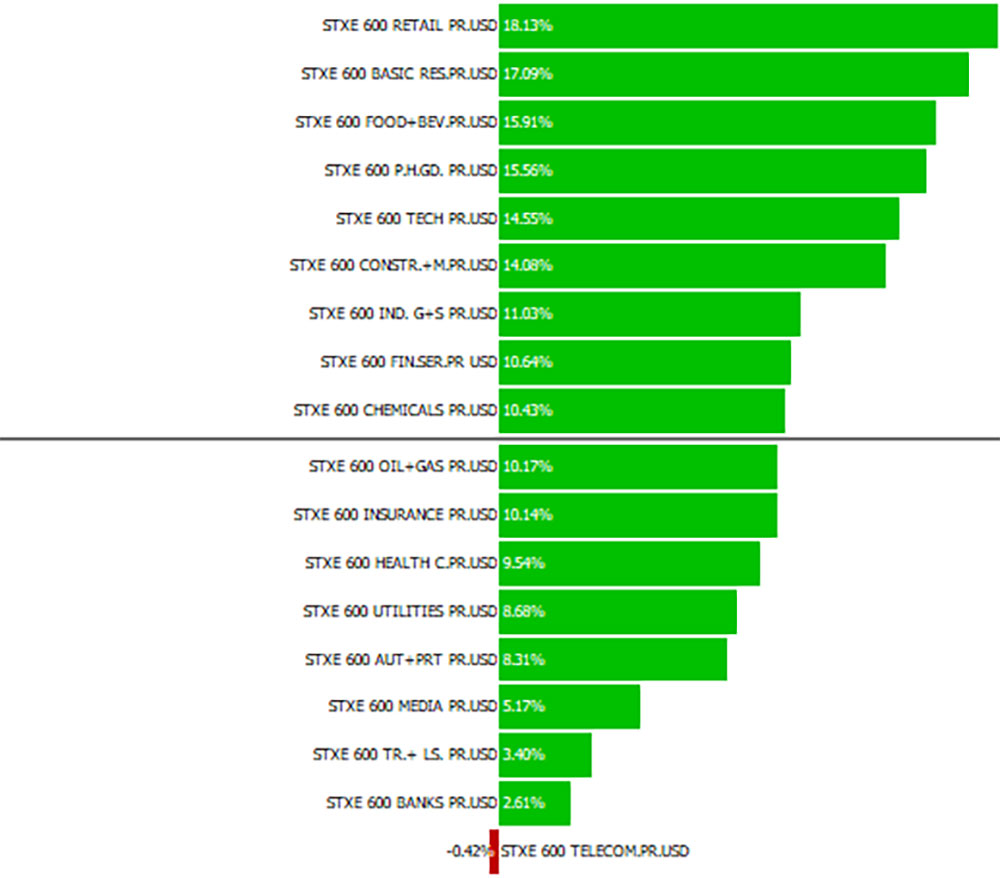

All sectors gained ground in the first quarter (the EuroStoxx600 telecom sector, valued in USD, did not see significant gains). Utilities and precious metals saw the strongest appreciation. Banks – once again – left a poor impression and ultimately traded only marginally higher.

Over the last two quarters combined, defensive stocks – primarily the utilities sector – saw the largest gains. With stable, not very cyclical business operations and generally relatively high dividend payouts, these stocks appear to be a popular alternative in times of low interest rates. The market thus seems not to believe in an imminent change in the low interest rate situation and invests accordingly to compensate for the missing income from interest.

The oil price ended its decline at the beginning of Q4 2018 and was able to recover somewhat at the start of 2019. Besides other factors, oil could benefit in the medium term from a generally weaker US dollar (US Fed nearing the end of interest rate hikes?).

The index-level recovery has not yet encompassed all stocks. There are still individual stocks that represent attractive buys from a valuation perspective as well as due to technical factors. For example, Swatch: the Swiss watch manufacturer has lost about half of its capitalization from its highs and has only recently seen moderate gains, which is also due to sales difficulties, e.g., in China. In our view, the stock is relatively inexpensive, and a purchase should be worthwhile in the medium term.

There are a number of other stocks (BASF, U-Blox, Sulzer, Continental, Hochdorf, etc.) that are attractive for purchase or that we consider interesting. From this perspective, the situation for investors has improved, as the last correction and the recent recovery have left some stocks with considerable price potential. Among other things, in our opinion, this is also due to market liquidity, which we have already described elsewhere (agent money and passive investing).

Market technology

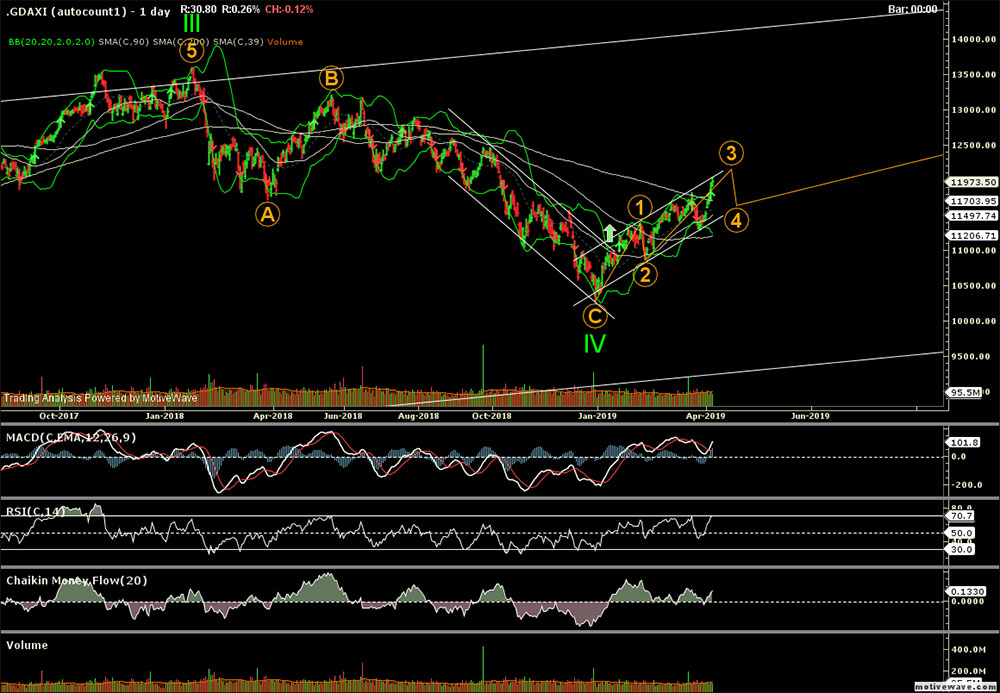

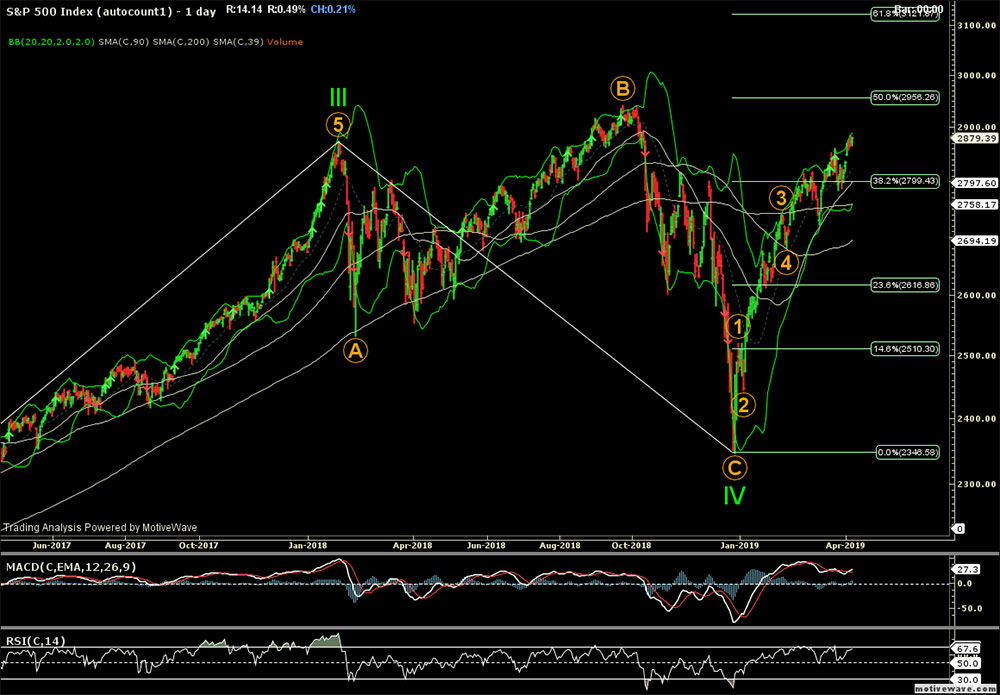

After a year of correction in 2018, 2019 could again be a year of some recovery. The first quarter has already made a start, and we will likely see profit-taking again in the course of the year, possibly soon. Technically, the long-term uptrend is still ongoing, as mentioned several times in the Navigator, but it is already far advanced, i.e., in its final phase. How long this will last remains to be seen.

In the scenarios depicted in the two charts, the correction would be complete, and markets would already be on their way up in the first step. As described in the first part of this letter, this year is likely to be determined by earnings development and economic performance on one hand, and central bank policy on the other. If the economy weakens and central banks continue their course of normalization, the correction is likely to continue. Otherwise, volatility is to be expected due to the constellation described earlier, and ultimately rising prices (because the economy is not collapsing and financial stimulus remains).

Outlook

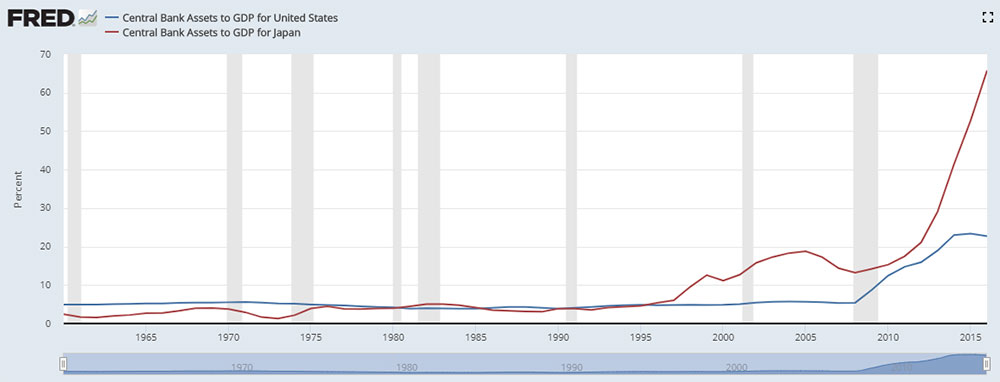

Although markets have been in a correction phase since early 2018, and this could also be the start of a bear market, we remain confident for now. Given that central banks are likely to reduce the intensity of interest rate hikes and balance sheet reduction in the future, and the economy will be weaker but still expansive, there should ultimately still be upside potential for equity markets. The ever-growing debt burden (USA: USD 22 trillion!) is likely to lead to a (further) increase in risk premiums sooner or later, which should also cause longer-term interest rates to rise. Fundamentally, the situation is not brilliant, but central banks can straighten out many things for now. Looking at the situation in Japan, one can see what else might be possible. Former Fed Chairman Ben Bernanke has already prominently commented on possible scenarios (helicopter money). Stocks remain volatile, but in the long term, within the known environment, they are almost without alternative as an investment.

Your EDURAN AG