The Navigator provides insight into stock market events with an outlook.

“The Bear’s Paw.” Expensive markets have suffered a severe blow. Without successful cushioning via strong stimulus, a deep recession threatens. Markets will find themselves in an environment of even higher debt, globally low interest rates, and further weakened growth.

Market review

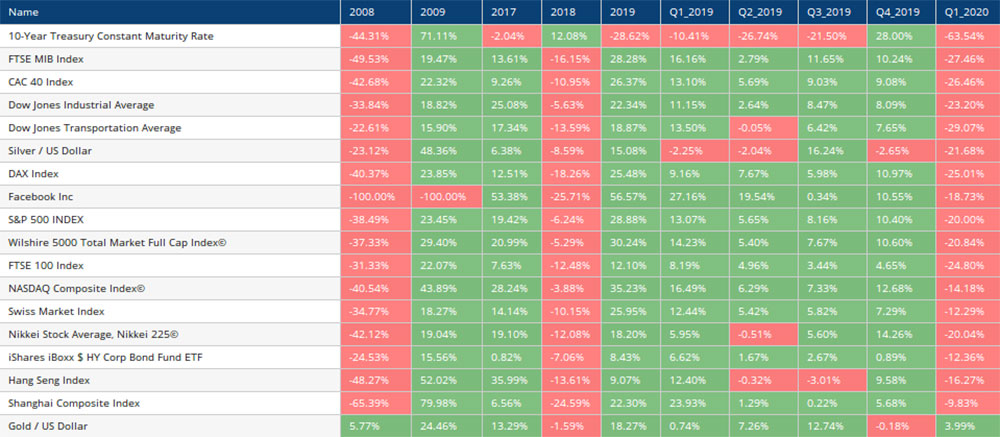

The first quarter was dominated by one theme: the Covid-19 or Corona crisis. The year, however, began favorably, and markets continued their path towards even higher valuations. As described in the Q4 2019 Navigator, earnings growth slowed relative to the increase in valuations, meaning increasingly more had to be paid for a unit of return. We all knew about the virus for some time, but it wasn’t until mid-February that the first, still relatively mild, sell-offs occurred. Almost out of nowhere, the stock market bear then struck. As the number of infected individuals approached and their curves rose, markets reacted panically. The government-mandated closure of businesses added a new dimension to the entire predicament. However, not only the Corona virus but also the relatively expensive markets and the market structure after the 2008/09 financial crisis contributed to this severe correction with thinned liquidity. While high volumes are traded, liquidity has increasingly thinned over the past few years due to a new market structure: more and more capital is managed through structures like ETFs, and large proprietary trading books at banks, which can intervene counter-cyclically when end customers lose their nerve and sell, are decreasing.

Stock markets all collapsed, interest rates reached new record lows, and spreads for corporate bonds, especially those with weaker balance sheets, experienced increases last seen during the 2008/09 financial crisis. After fast or weaker hands reduced positions, sales of leveraged investments likely followed later – on March 13 and March 16.

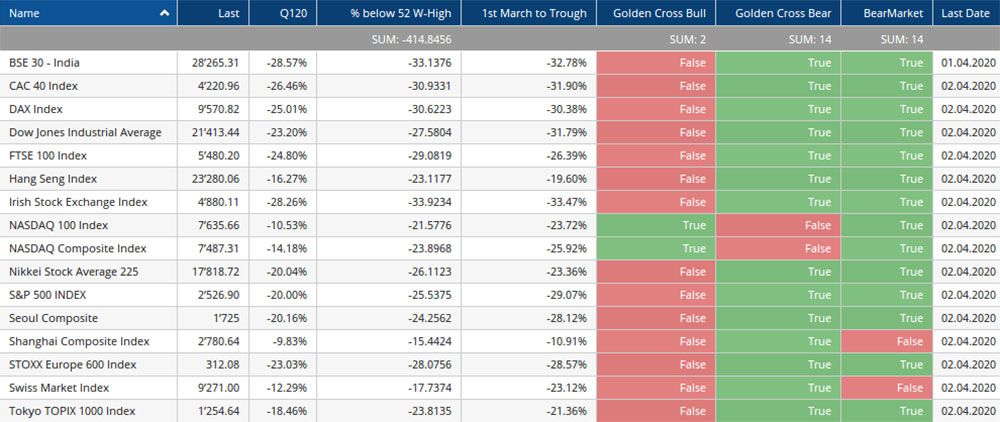

The losses measured from the beginning of March to the troughs mark the provisional peak of panic selling (around mid-March). Most markets are already in a bear market in the interim.

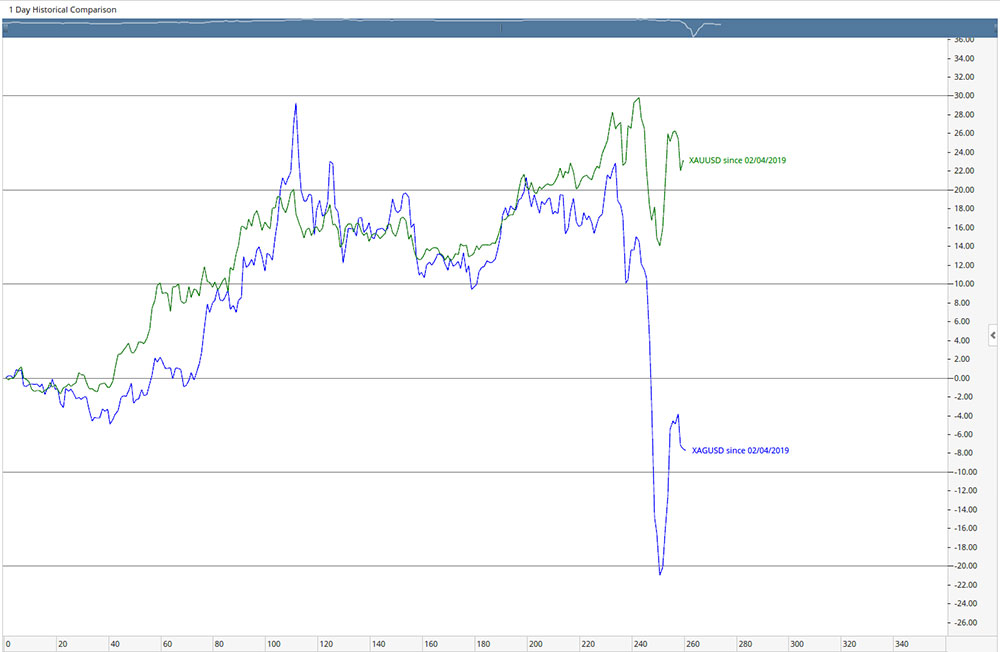

Gold also declined after an interim peak, as did silver. In the case of gold, it is to be assumed that, in addition to the demand for cash, investments with involved external capital (leverage) also had to be sold. For silver, the additional factor of reduced industrial activity contributed.

As if the Corona crisis wasn’t enough, the dispute between Saudi Arabia and Russia regarding oil production volume and oil price was added. The consequences were a supply shock in the form of ramped-up capacity or production volume, which put pressure on the price. With the lockdown and the shutdown of the economy in combating the virus, demand also experiences an unprecedented damper: we hear that global oil demand has collapsed by up to 1/3. Strategic reserve stockpiles stepped into this breach and increased. In this regard, it is interesting to see that a negative correlation exists between the oil price and inventory build-up. This is evident, as shown below, in the longer-term horizon, but also in the short-term window. Additionally, it is to be expected that the USA will pressure the Saudis to stabilize the price (this has happened before in history, when President Reagan, together with the Saudis, pressured the Soviet Union with lower oil prices – this time, however, the USA needs higher prices). The US oil industry in the “fracking” sector will face major problems at prices below USD 40 per barrel WTI, and a large number of bankruptcies is unavoidable. The Saudis themselves can produce oil cheaply but need an estimated revenue of USD 60 per barrel to keep the state apparatus running and probably closer to USD 80 per barrel to be deficit-neutral. The only beneficiary could be Russia, which – detached from the US dollar – is relatively self-sufficient and, with large gold reserves, intends to profit from a languishing Western economy in the long run. Ultimately, it is to be expected that the current upheavals will also geopolitically set a lot in motion. The oil price is likely to remain under pressure for the foreseeable future – until the economy is ramped up again.

Interest Rates

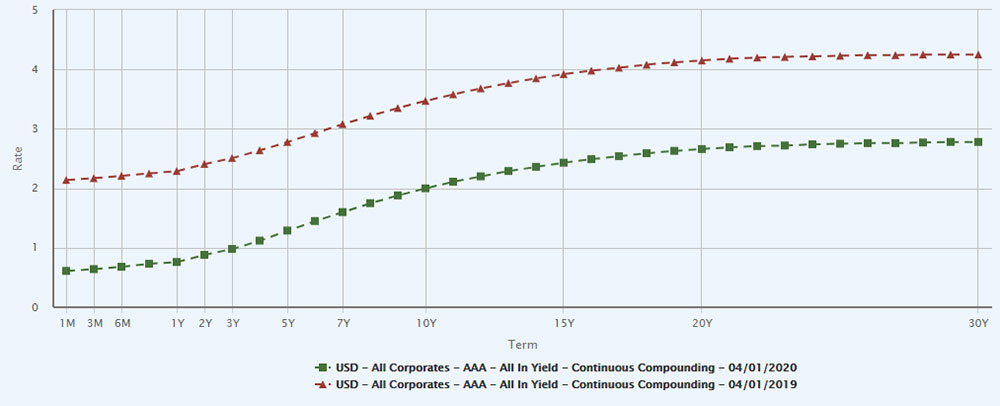

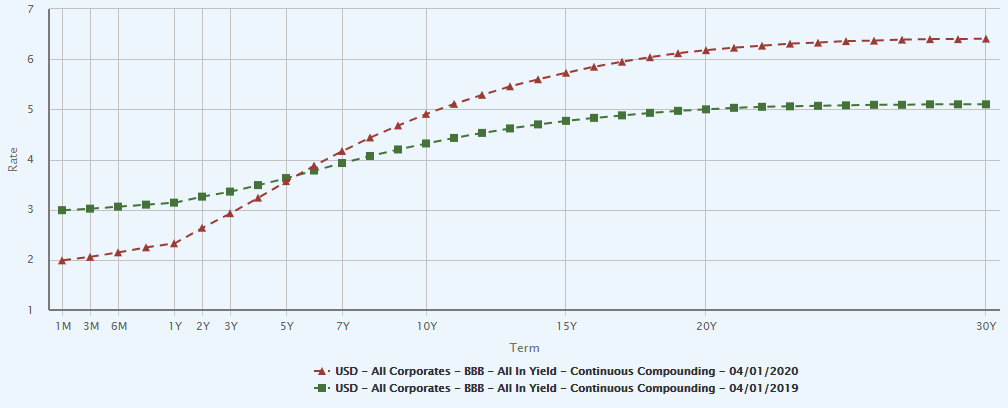

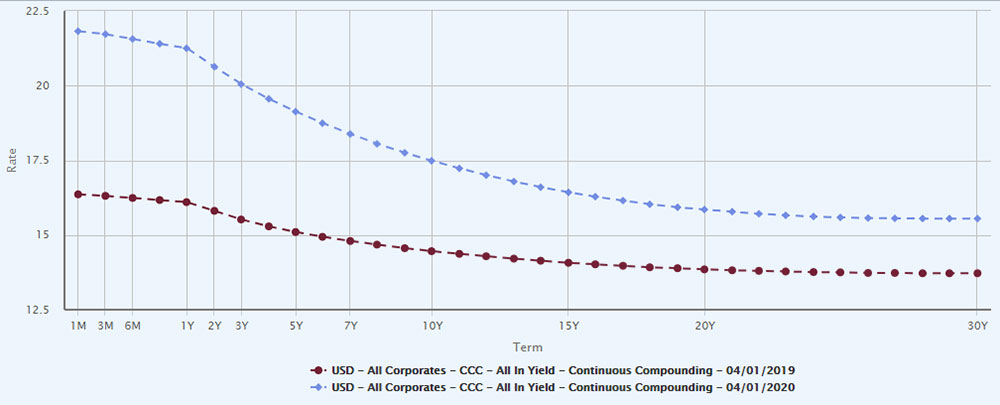

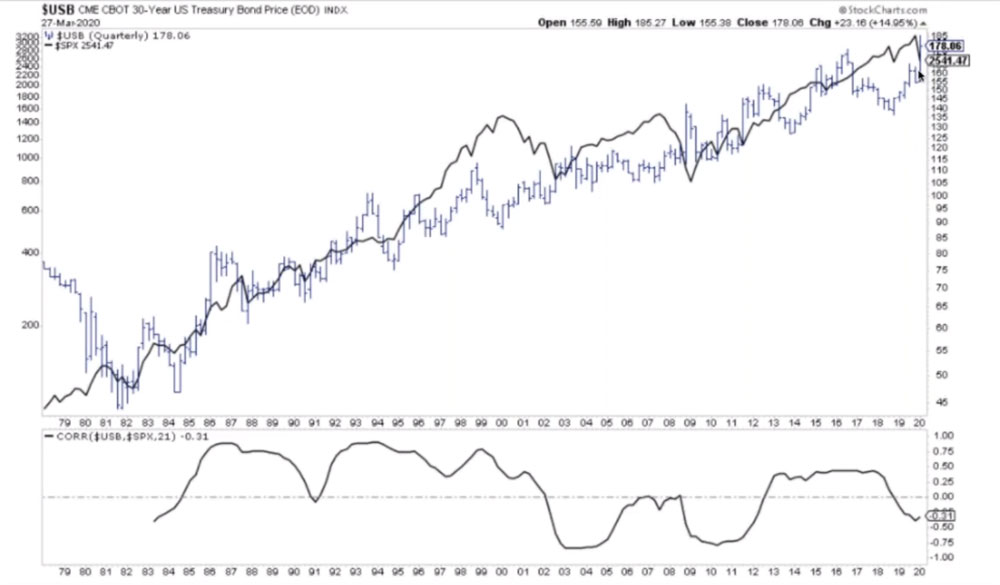

With the Corona crisis, there was also a flight to so-called safe havens. Yields on government bonds have fallen to new record lows – due to its sheer size and global significance, the US government bond market is primarily to be considered here. The US Fed once again opened the floodgates in crisis mode and launched a massive monetary stimulus of around USD 4 trillion (about 1/5 of US GDP). US dollars are increasingly needed within the country itself, which causes a certain scarcity in the Euro-Dollar sector and puts emerging markets in a difficult position (USD debt). With the onset of a deep recession, credit spreads have also widened – levels approached the stress in the system of 2008/09. Corporate bonds with weak ratings have had to accept price losses. In the investment-grade sector (BBB and higher), several downgrades are to be expected soon, which technically implies sharp price reactions (downwards). The number of bankruptcies will increase.

Market technology

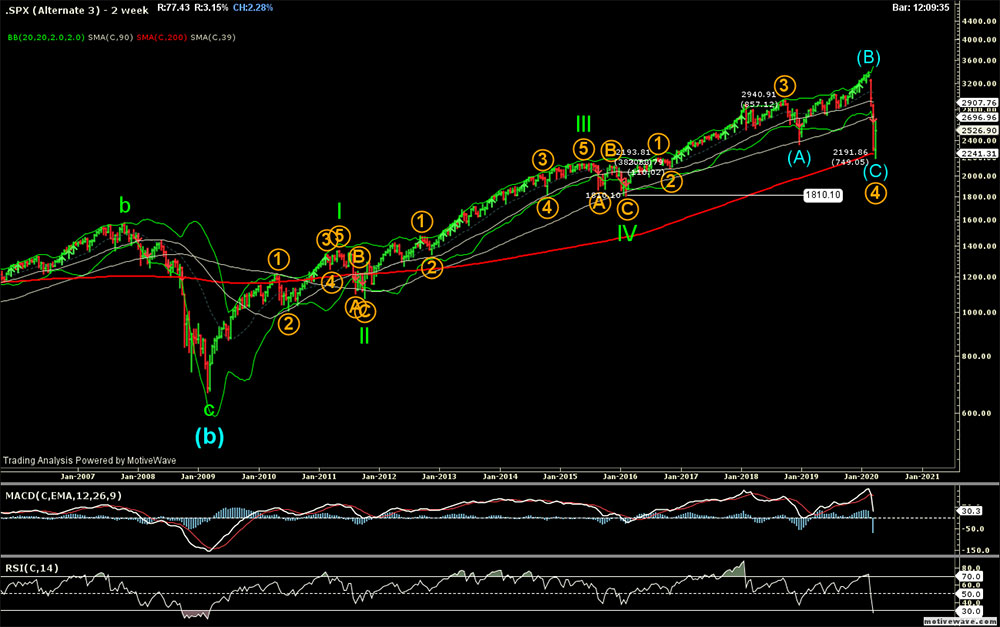

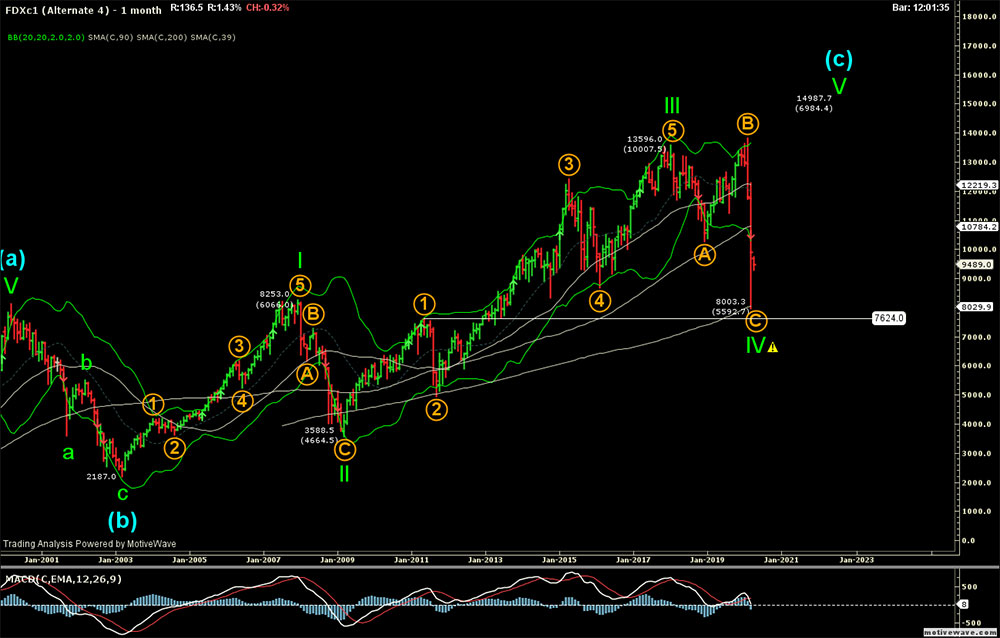

Economists like to compare today’s situation with the crash of 1929 or – less headline-grabbing – with the correction of 1987. 1987 is closest to the course of the current price correction in terms of duration and extent of loss. The recovery immediately after the correction was also around 40% in 1987 (measured from the previous peak to the low point of the movement). In 1929, the first slump with around 40% recovery also lasted about 1.5 months. And this is where we stand now, seen this way; in 1987, another uptrend started afterwards, while in 1929, worse was yet to come.

In addition to even lower interest rates, the option of fiscal stimulus is increasingly being used, which floods additional money into the markets. Due to the correlation between interest rates and equity valuations, further support for the markets could come from this side. While interest rates are near or at zero, the question arises as to how long this can last. If the state now additionally pursues MMT/fiscal policy, this additional money could stimulate the markets again.

Outlook

With the Corona virus on everyone’s lips, we believe the actual damage will be felt indirectly and with longer-lasting effects in the economy and society. The health aspect, with its tragic consequences for every death or severe course of Covid-19, will hopefully soon turn for the better. The stock market has reacted and accounted for one scenario, currently the most probable, with the price decline that has occurred. Investors who, unlike other market participants, pursue a longer-term perspective can use such weak phases for selective acquisitions. If the shutdown continues longer, however, the correction will continue. The current price correction is likely to have factored in a 1-2 month economic shutdown along with aid measures. Already now, we find an environment with even lower interest rates, and alternatives for investments with positive returns will be even scarcer than before this current crisis. Money will thus increasingly be pushed into risk assets like equities. However, unlike before this crisis, the quality of the investment is likely to play an even greater role in the future.

The traces of the measures taken will make the state appear more powerful and restrict individual liberties. As after the 2008/09 financial crisis, where the state rescued banks and subsequently adopted new, costly regulations, politicians are likely to want to have a say this time too. Added to this are the immense costs, which have arisen in the form of debt or advance payments and must be borne by taxpayers or premium payers. This money is lacking elsewhere, including for investments. One also fosters a “full-coverage mentality” in society when the state supports companies (apart from certain bridging loans). Competitors with fuller coffers could have prevailed and secured margins. Without a departure from this policy, growth is likely to be increasingly modest, as it has been in the past 10 years. This, in turn, will not be conducive to long-term stability, and the fragmentation of society, with political upheavals as a consequence, could also further intensify.

Diversification and quality stocks are also suitable in the current environment. Favorable valuations also offer the opportunity to use existing liquidity for acquisitions. Because if nothing is added to savings accounts and social welfare systems tend to be thinned out, the demand for alternative investments such as equities could rise.

“Patience is the foremost virtue of the investor.” — Benjamin Graham

EDURAN AG

Thomas Dubach