The Navigator provides insight into stock market events with an outlook.

Market review

The third quarter was largely determined by a kind of vacuum between the two forces, namely the dampened growth prospects and a supportive counteracting interest rate policy. After corporate earnings were massively revised downwards by analysts over the course of the year, around 75% of the reported earnings were within or exceeded the estimates. For the coming year, analysts expect, for example, a renewed profit expansion of around 10% for the USA.

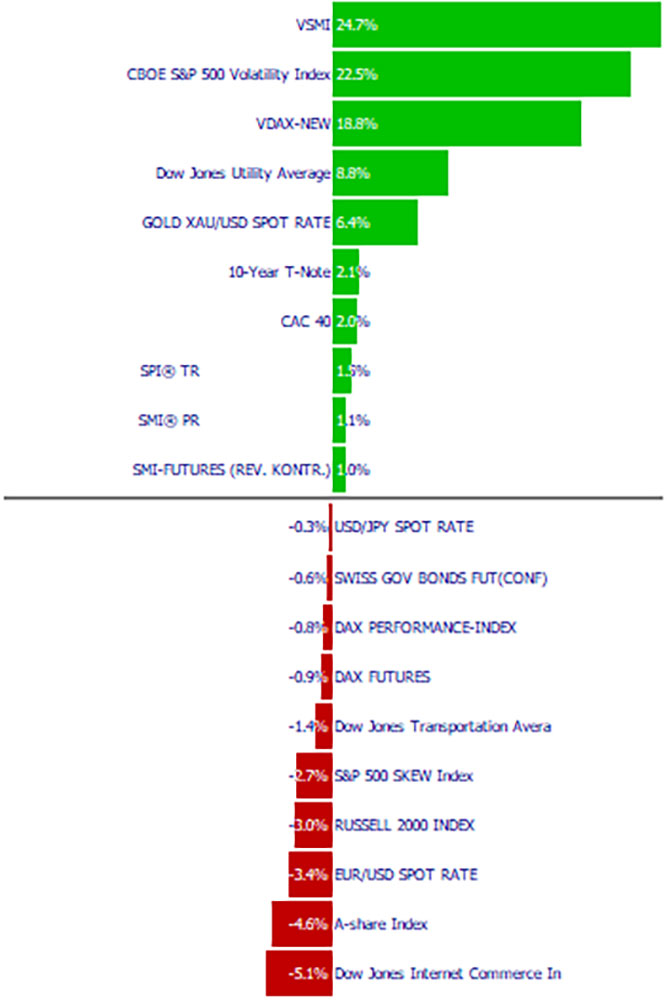

As can be seen in Figure 1, most major stock indices closed almost unchanged. On the interest rate front, there was lively reporting about the change in leadership at the ECB, where Christiane Lagarde will take over as chair and has already announced that more, not less, stimulus is to be expected from her. The markets have mostly moved sideways, but in a rather broad range. Investors’ nerves have been strained, which can also be seen in the increased volatility indices.

Gold – as mentioned in the last report, technically broken out of the resistance line of $1350/ounce from a market technology perspective – was able to gain over 12% in the 3rd quarter in the meantime. The small and medium-sized capitalized stocks were able to gain some ground for the first time in months towards the end of the quarter and make up ground. The lowest prices were marked together with the general weakness phase in August. Gold has brought the topic back into conversation somewhat, but we are still far from euphoria and are happy to buy a little more at current (or even lower) prices.

Market insight

Profit growth

Regarding profit growth, there is speculation as to whether there will be a broad recession or whether we are rather in a temporary period of weakness as last in 2015. There are signs and indications for both scenarios.

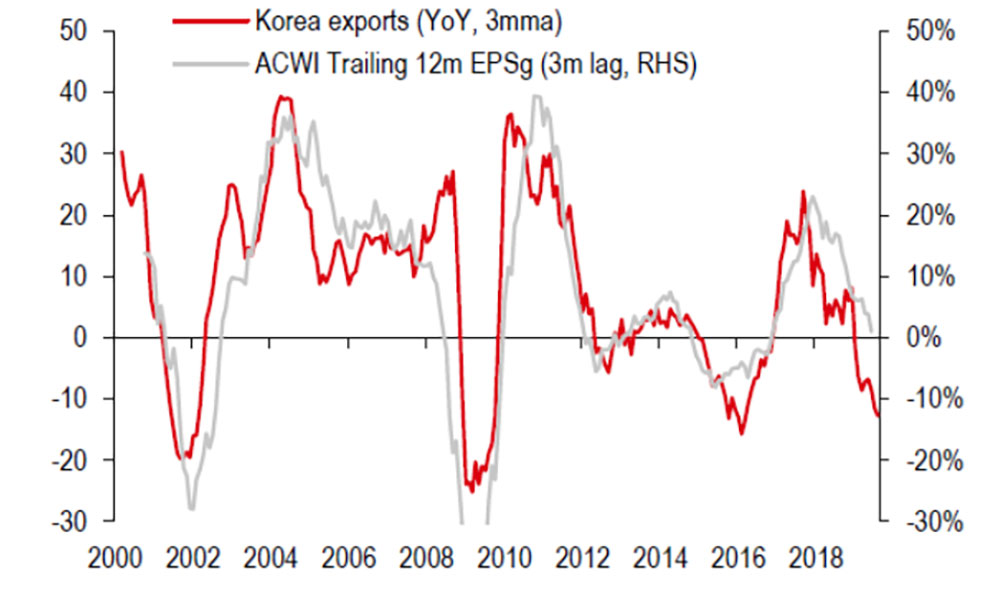

The open and export-oriented economy of South Korea has served as a reliable early indicator of global growth in the past. Recently, Korean exports have shown weakness; this could be an indication that corporate profits will follow suit and tend to weaken in the near future.

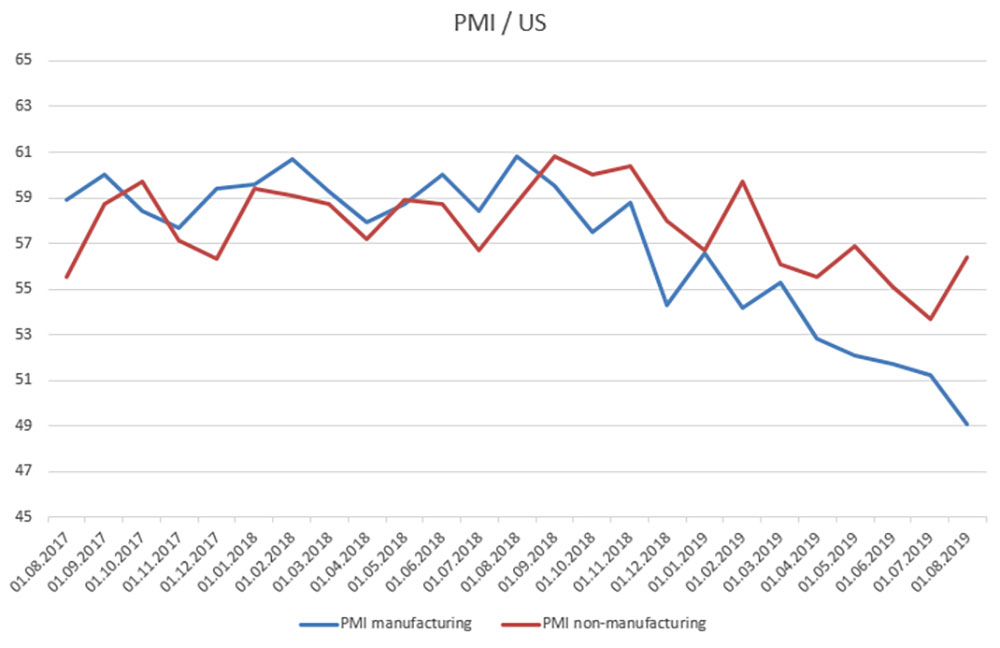

The purchasing managers’ indices of the most important economies have also weakened. The largest economy (USA) fell below the critical mark of 50 at the beginning of the third quarter and has not recovered in the course of the quarter, on the contrary.

On the other hand, there are first signs of a certain recovery, that the recession will not widen further. According to the German Association of the Automotive Industry (VDA), there was an increase in sales in September compared to August, and on an annual basis, around 30% more new registrations were registered in August 2019 than in August 2018. For the coming 4th quarter, however, a decline is expected, but less intense than in the 4th quarter of 2018. And in May, China passed a law forcing motorists to exchange gasoline engines with the “National 3” standard for new vehicles by the end of 2020 (this involves around 20 million such vehicles). The automotive industry and its suppliers are often seen as the cause of the current industrial weakness phase.

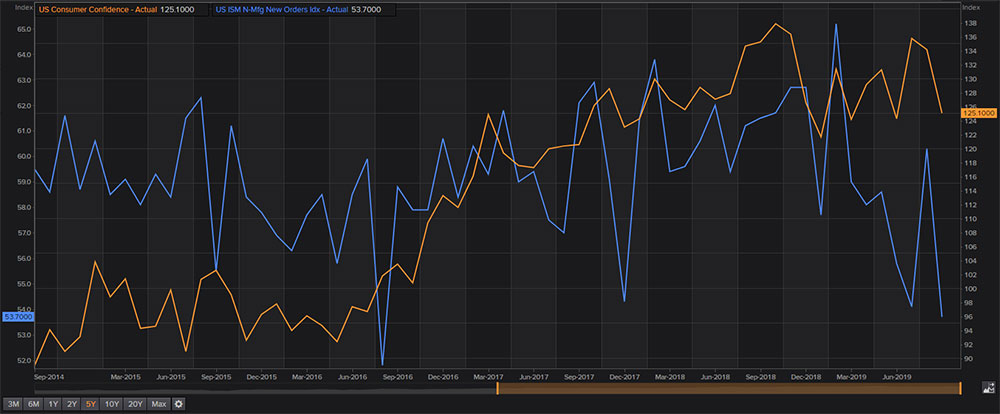

Consumption has so far remained largely unaffected by the crisis and remains at a relatively high level (measured by the consumer confidence index). The longer the crisis lasts in the manufacturing sector, the greater the likelihood that it will spill over into the consumer goods sector. Towards the end of the quarter, companies reported inquiries for short-time work.

Another important factor with regard to growth is and remains China. After almost 3 decades, the Chinese engine seems to be faltering. The Central Committee has already announced with the communicated “reorientation” that one should not expect 8 or 10% growth rates. Nobody knows how strong the effective growth is. It can be assumed that China is even more in the debt trap than the West. After the global financial crisis of 08/09, the government massively raised money, then again in 2015 plus in the following years – always to stabilize the economy. The banks are very weakly capitalized (assumption 2%) and increasingly dependent on external lenders (shadow banking system and USD borrowing via Hong Kong). US trade policy is hitting China at an unfavorable time. China could increasingly stumble, which would hit export-oriented nations like Germany much harder and thus the earnings prospects of companies.

Central bank stimulus

On the other hand, we have the aforementioned financial stimulus through low interest rates. The latest central bank decisions indicate that interest rates will not be lowered massively further into negative territory, but rather that the focus will be on securities purchases and other forms of economic stimulus (fiscal stimulus, MMT). Because not only in the central bank councils there is strong criticism of the negative interest rates, also from politics more and more opposition is to be expected. The money created has not flowed into the real economy, but via the financial industry into tangible assets such as stocks, real estate or even art. Christiane Lagarde is also expected to reissue bond purchases in a broader version in addition to the low interest rates. In addition, she is considering – preposterous – buying more green bonds as a “signal” and eventually – when the EU Commission presents its definition of “green” investments, which is in the works – to strike here as well. Monetary policy with a political tinge.

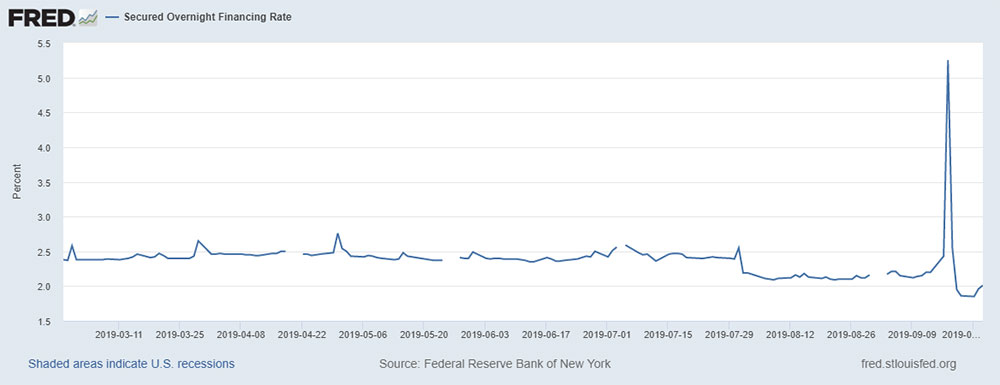

Despite the generous monetary policy, a liquidity bottleneck occurred on the interbank market on September 18. The repo rate jumped to as high as 10% in the meantime, where it would be conceivable that banks could finance themselves near or within the target band of the Fed Fund rates (old 2-2.25%, new (Sept 18) 1.75-2%). It seems that not everyone can finance themselves at the intended interest rates. Risk premiums are likely to rise (there seems to be a problem with the collateral). As a consequence, a steeper yield curve is expected, where the longer-term rates should rise in relation to the short-term rates.

Interest rates

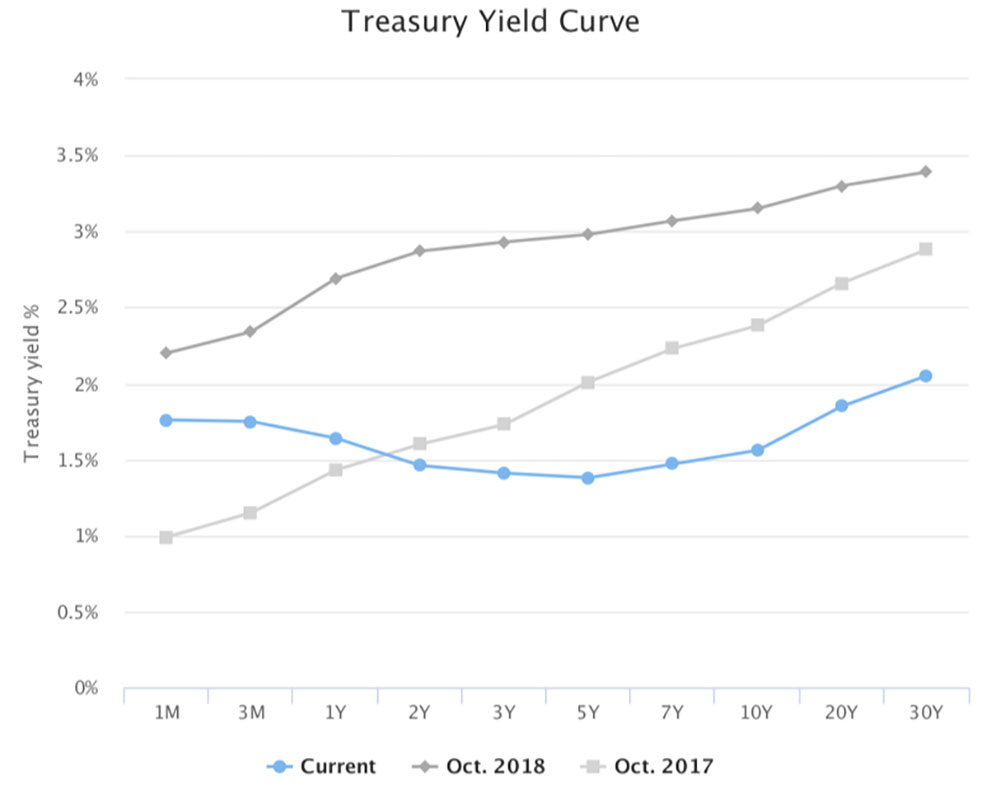

Yields have remained under pressure, with 10-year US yields coming close to the previous low from July 2016 at the beginning of September. Then came the turnaround and yields made a countermovement upwards. In other words, the yield curve in USD has become somewhat steeper (Bear-Steepener). The same applies to Europe, where interest rates or yields on 10-year German government bonds initially also came under pressure before rising again in September.

As reported earlier in the Navigator, the yield curves – especially that of the leading economy of the USA – have flattened. What is more, the spread (difference) between the short-term interest rates compared to the longer-term interest rates has slipped into negative territory (one looks i.d.R. at the 3-month rate vs the yield of the 10-year Treasury maturity), which historically resulted in a recession (since 1973 there was a recession within two years). However, in history there was also not such a bold intervention of the central banks to be observed.

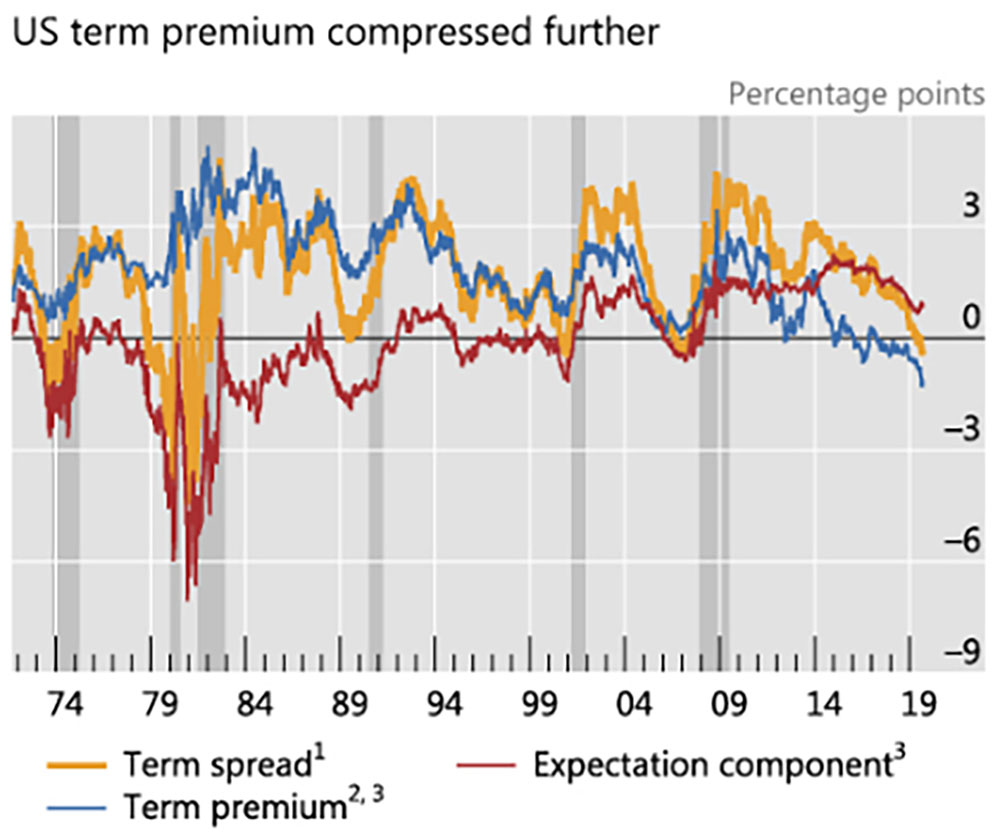

In particular, an impact on the term premiums can be observed here: In fact, the recent inversion of the US Treasury curve coincided with exceptionally pressured term premiums. Term premiums in the US Treasury market have been declining since the Great Financial Crisis, likely due to demand pressure from price-inelastic buyers such as central banks, pension funds and life insurers. Also, the current combination of a negative term premium and a weakening monetary policy stance is unusual, as a tighter monetary policy course was in tune in past episodes.

In view of such complications, it makes sense to examine other indicators of recession risk. In addition to the 10y-3m Term Spreads, the literature has identified several other measures that may indicate an impending economic slowdown. For example, a low short-term forward spread or a stretched excess bond premium, which under the line give a certain probability to the recession risk.

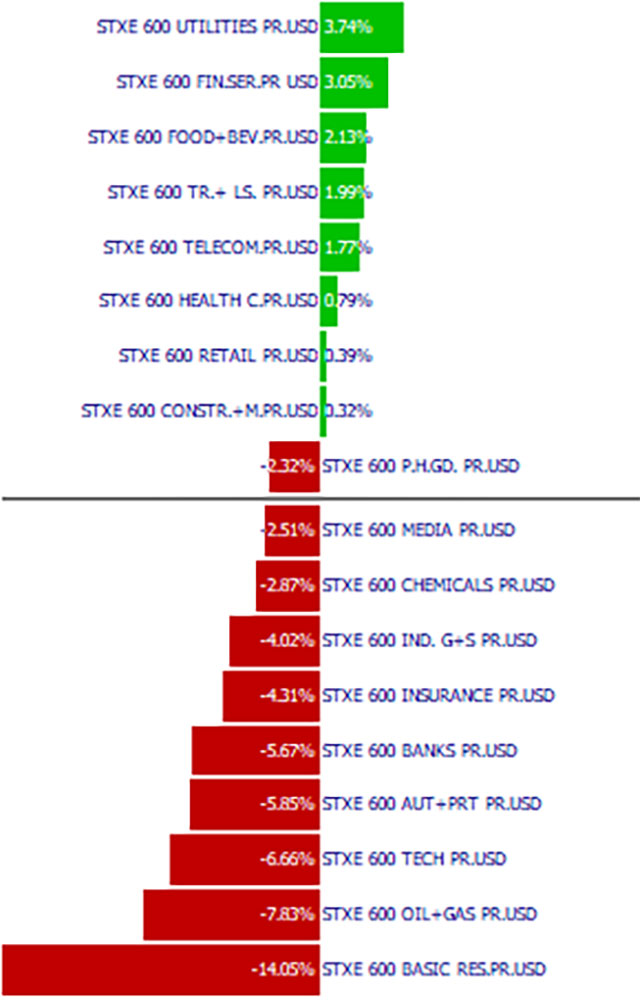

Sectors

Among the sectors, the utilities sector floated on top, followed by the financial services sector. Banks, in turn, were one of the worse sectors and closed the quarter across the sector (slightly) in the red. However, a little hope has arisen that these could be at the beginning of a technical bottoming, with at least a small recovery. Generally speaking, the defensive, non-cyclical sectors have been preferred. In the context of an economic slowdown, the cyclicals and above all – still under pressure – the automotive sector lost the most ground. Towards the end of the quarter, September, there has also been a small recovery here.

For the gold mines, the quarter began with a breakout to the upside and then came the consolidation at a higher level. How long this consolidation lasts is not predictable. With the pressure on interest rates, demand for the precious metal should remain intact. Technically, the gold would be ready to add another step up. Should this happen, we also expect a strong increase in silver, especially since the relatively low historical gold-silver ratio (Navigator 2nd quarter) could increase demand and attention in favor of the “industrial metal” silver. For oil, after the surprise attack on the largest refinery of the Saudis, there was a violent price spike upwards, which corrected immediately back towards previous levels, after the Saudi Arabian Ministry of Energy had fed in existing oil reserves. A temporary persistence in the range of $57 – 62 is likely, a breakout should then initiate a new trend.

Market technology

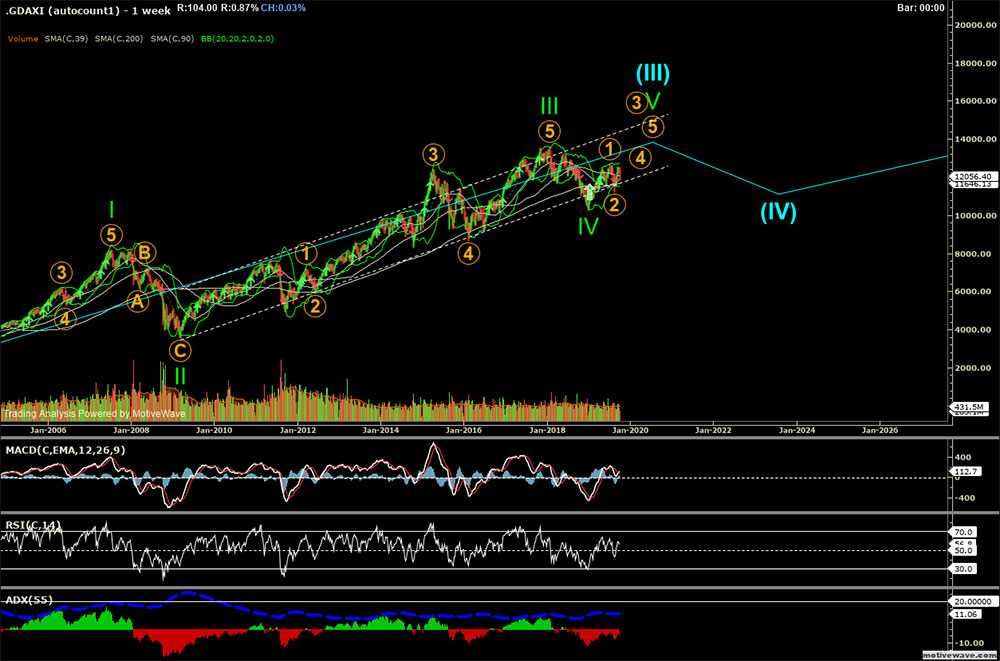

As described in the last quarter, the markets have apparently left behind the correction of 2018 with the 1st quarter of 2019 for the time being. At least in the USA, where a new all-time high in the S&P500 was marked at the end of July. In Europe, it looks a bit different, especially in Germany. The economy is suffering and the growth dent in China. Under the line, therefore, no clear trend can be identified technically, at least not in the medium term. One variant would be the continuation of the correction in the sense of a longer-lasting sideways movement (Triangle). The positive variant would be that we are already in the new upward trend (the last of the current upward cycle).

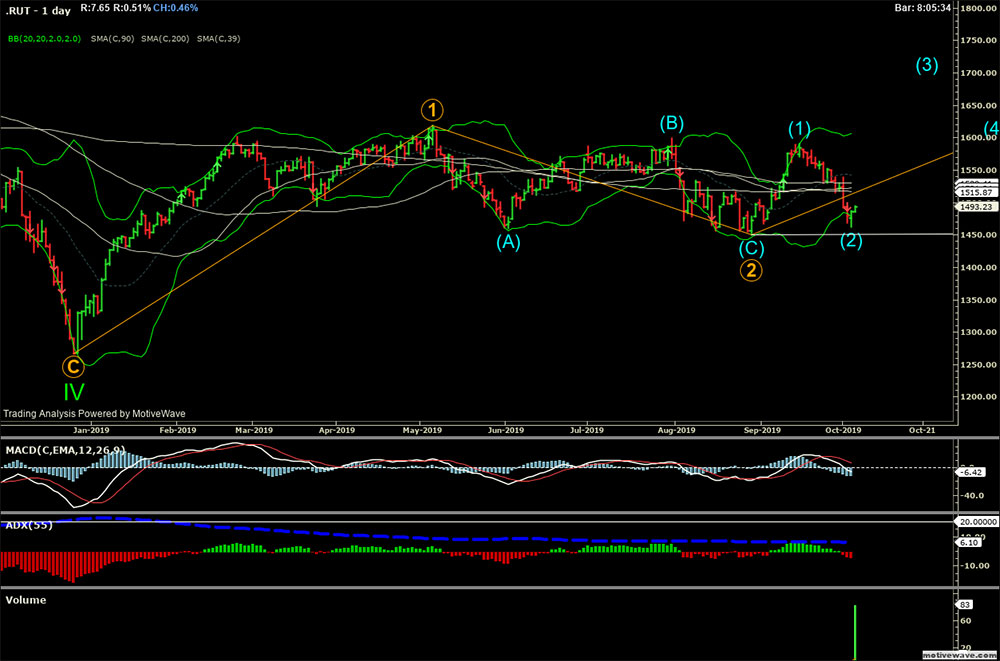

If you look at the broader indices, such as the Russel-2000 index, then this has corrected more strongly, or has more difficulty getting back on its feet. Most of the money flows into the large blue chips. In the positive variant, the smaller capitalized titles have good potential upwards. Important, however, that e.g. in the Russel-2000 the mark at around 1450 is not undercut.

Outlook

The coming months will bring clarity as to whether the economy slides into a recession or not. China as the driving force of the past years is busy with itself and will – sooner or later – have to remove the mountain of debt and thus forego growth. The West is also busy with itself, here especially the EU, which is also waiting for Brexit like the rabbit in front of the snake. The USA is rather in the process of shaping (and has strategically various trumps in hand like the USD, the domestic market, the technology sector and a better demography). Decisive for the markets will, however, continue to be the profit development of the companies in addition to the money flows. With the Frenchwoman Christiane Lagarde, it can be expected that more of the same will come, i.e. a loose monetary policy – possibly with new government debt (fiscal policy). The USA will probably also have to lower interest rates, as President Trump loudly demands (which should not be the reason).

The correction in the markets is getting closer. If not in the coming quarter, then probably in the first half of 2020. This is based on the thesis that the weakness in the industrial sector has enough emphasis that it finds ways into the consumer sector. Already with the change of quarter, industrial companies have inquired about short-time work at the office (D & CH). However, we do not expect a dramatic slump on the stock exchanges as in the crisis of 08/09. The markets are likely to generally increase in volatility due to the increasing uncertainties.

All that said, stocks as an investment vehicle are still to be favored in the long term, they offer the best protection against devaluation of money generate with the right choice recurring income via dividend. Gold is also still a welcome stabilizer in the portfolio context. Whoever can, does not invest in nominal values with negative redemption yield. With increasing volatility, it also applies to take profits – where it offers itself – and to build up or expand positions at lower prices.

EDURAN AG

Thomas Dubach