The Navigator provides insight into stock market events with an outlook.

“Price & Value”. Record-high economic downturn, short-time work, and bleak prospects. Yet, stock markets are back at record highs. At least in the short term, this is not a contradiction, as the market environment forces capital into the stock market. Viewed this way, it is a rational decision, with the drawback that, due to a lack of alternatives, massive capital flows into risky assets such as stock markets.

Market review

The immediate crisis with the virus seems to be history after the market crash in March. There is hope for a cure or a vaccine, while simultaneously attempting to live with the virus. The advent of the virus has ushered in a new era. However, much of what has come to light due to the virus was already in motion. For example, geopolitical tensions, including those between communist China and the USA. China, which has skillfully attracted capital and technology from the West over the past decades, is advancing and challenging the USA as a hegemon. The virus appears to be helping to cement and further expand this status. The debt situation has also worsened. Since the 1980s, debts have been steadily rising worldwide, including in the supposedly wealthy West. With the virus, debts have soared to new highs in many places.

While credit growth initially supported economic expansion, it has now become indispensable. Without credit growth, a recession looms. With the virus and the mandated measures such as lockdowns, the economy has slipped into recession, at least in the short term. However, even here: there were already ample signs of a recession before the virus outbreak.

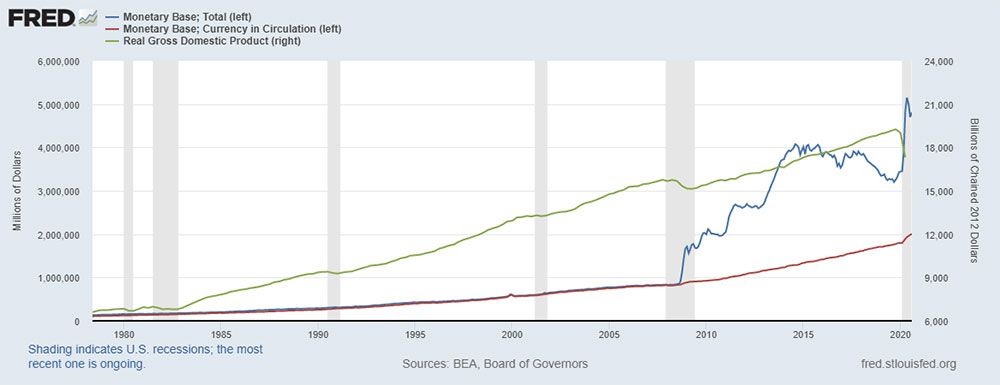

Monetary policy has been a recurring topic in our quarterly letter, as it attempts to avert or mitigate crises. Initially, central banks supported struggling markets with interest rate cuts (LTCM, Tech-Bubble-burst); later, more aggressive forms of open market interventions were added, where central banks directly purchase securities in the market. While initially government bonds, today it is already corporate bonds indirectly via ETFs (or even equities, as in the case of the SNB). Central bank balance sheets have swelled to unprecedented sizes (however, central banks have not been around for that long; the Bank of England since 1694, followed by the US about a hundred years later, and then the Swiss National Bank in 1907).

When a central bank buys securities, the selling commercial banks do not receive “real” money in return, but rather a credit to the reserves that commercial banks hold with the central bank. For this to become “real” money, the commercial bank must issue loans. Commercial banks have issued loans, but as the figures regularly show: too little.

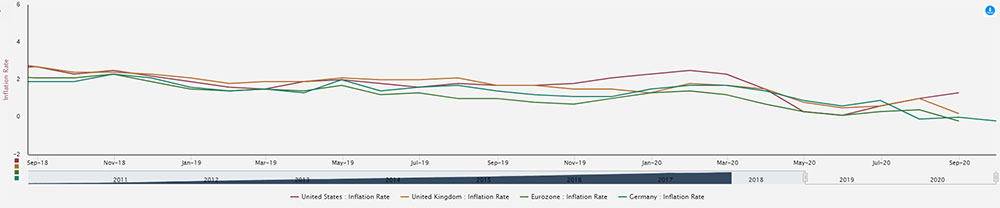

With the so-called “Corona” crisis, a new development is that politicians are also issuing loans or providing guarantees for loans. Thus, “real” money is directly channeled into the economy. Unlike central banks, which cannot directly fuel inflation without commercial banks or active economic participation, a continuation or expansion of “Corona checks” or guarantees issued by politicians would likely breathe new life into inflation.

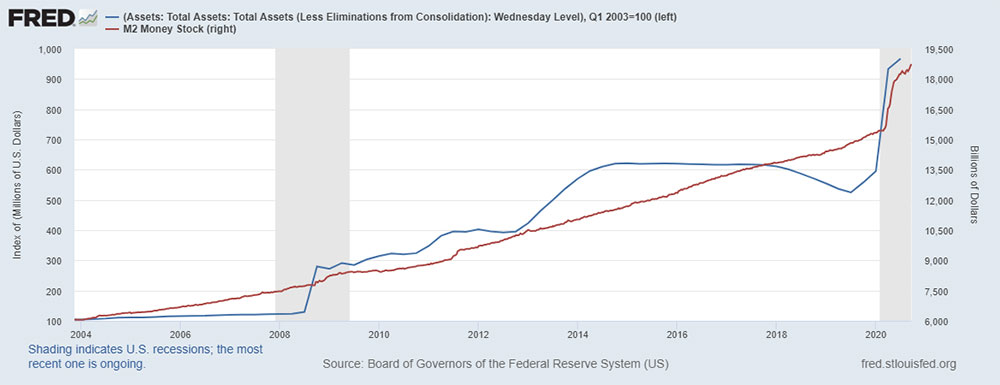

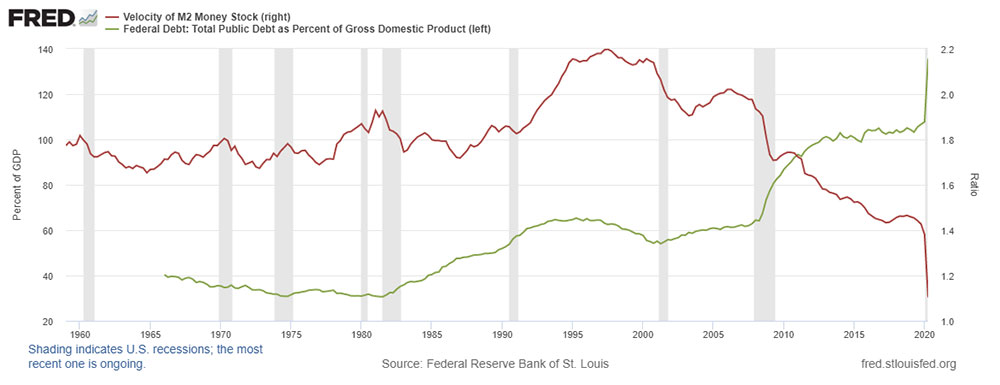

As shown in Figures 1, 2 & 3, the money supply (M2) has indeed increased, but the velocity of money has noticeably decreased and left its decades-long range downwards shortly after the start of QE in 2011. Furthermore, comparing the velocity of money with the ratio of total debt to Gross Domestic Product shows that when debt accounts for approximately 2/3 or more of the Gross Domestic Product, the velocity of money weakens. With the virus from China, it has almost come to a complete halt.

In short, it can be said that as a global economy, we seem to be deeper in the mire than before. The credit situation dominates events, and although central banks are doing everything in their power, the weak demand side for loans and investments appears to be a significant part of the problem. Growth stimuli are required.

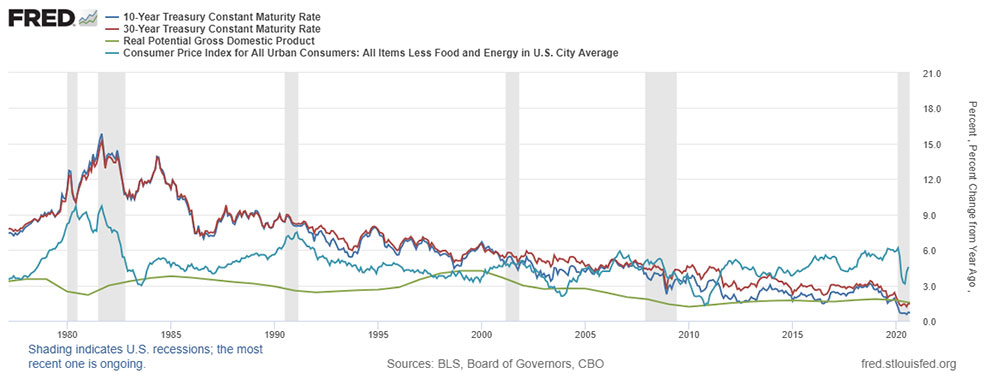

Central banks are helping as much as possible, but whether they can timely withdraw the provided money should the economy gain momentum is an open question. The virus has disrupted or dislocated supply chains, which in turn can upend prices. What tends to look like overcapacity on the supply side and has a deflationary effect has also driven up costs. After years of disinflation and deflationary tendencies, markets are tentatively suspecting the first signs of inflation.