The Navigator provides insight into stock market events with an outlook.

April 6, 2021

“A Second Crutch”. The markets continue their upward trend, in contrast to the economy, which remains battered. Capacities are still idle, and the labor market is struggling. The new US administration has ambitious plans and is supporting the economy with an unprecedented investment program. Alongside loose monetary policy, this serves as a second crutch for the struggling real economy.

Market review

The first quarter was still dominated by the virus. Many started the new year with the hope that the vaccination campaign would soon pave the way back to the “old” normal. With the emergence of new mutations, such as the variant from Brazil, and delays in vaccinations, hope diminished somewhat. Cumbersome Europe failed to secure enough vaccines in time and lags behind the Anglo-Saxon countries. While the Trump administration or Prime Minister Johnson were previously labeled as chaotic or COVID-ignorant last year, Europeans today are still in lockdown and cannot go to a sports stadium or have a beer in a pub.

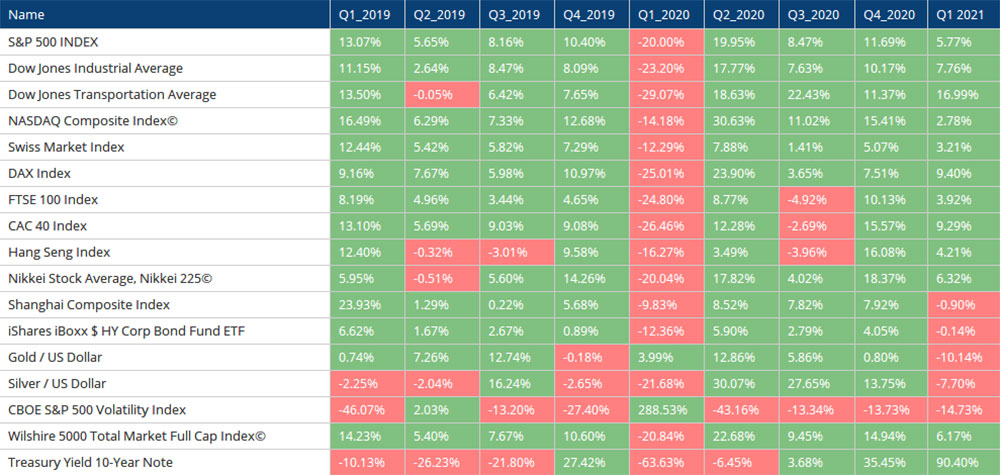

Stock markets traded in a relatively broad sideways movement for the first part of the quarter, only to regain upward momentum towards the end. While sentiment at the beginning of the quarter was rather cautious – many had hedged their positions – it was likely, among other things, the announcements by the US government of immense economic support packages that ultimately reawakened the markets. We are now in a situation where, in addition to the central banks’ low-interest rate policy, governments are channeling additional amounts of money into the markets (and now also into the real economy).

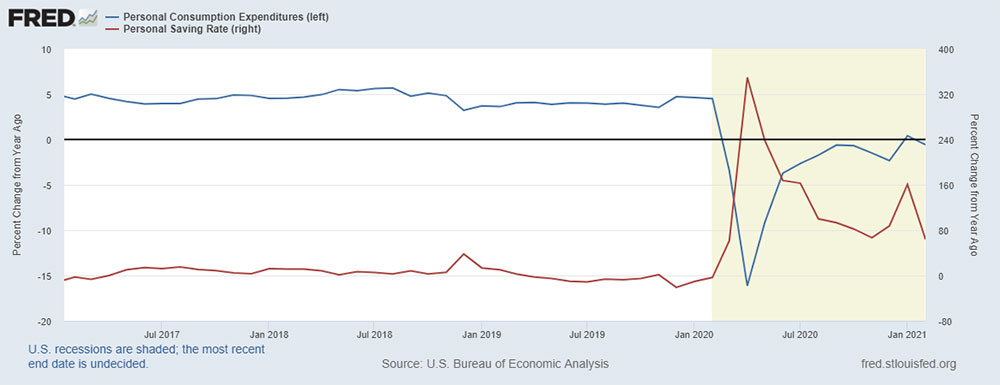

On the interest rate front, investments came under pressure; that is, yields rose and are approaching pre-COVID crisis levels again. However, the yield curve has steepened, representing a new dynamic. The immense deficits and pent-up consumption, or rather the money saved during the lockdown, demanded an extra premium for longer-term investments due to the risk of price increases (anticipation of inflation). While ‘inflation fears’ might be an overstatement, the topic of an inflationary surge has certainly arrived. On the other hand, national bank purchases already account for a significant portion of bond demand – the market is thus relatively dried up, and with the existing demand (also due to regulations or simply investment guidelines), there is continued downward pressure on yields.

Gold continued its consolidation, which had already begun in the last quarter of 2020. Commodities, however, traded higher, which is likely attributable to the discussion about a potential rise in inflation. The US dollar weakened significantly against the JPY and CNY, which, in conjunction with rising US interest rates, again raises questions about the state of the economy. While under President Trump, US dollars were increasingly used “at home” – a pull back home that, for example, made life difficult for foreign dollar debtors – it is still unclear whether under President Biden, the demand for capital for investments will occur to the same extent in the USA. Finally, cryptocurrencies have also made headlines, especially Bitcoin. A relatively light asset class with a promising starting position (BTC is currently limited to 21 million units as agreed) meets cheap money coupled with a certain carelessness: excessive demand drives prices up. There is no immediate return. For us, BTC is an opportunity to diversify, within a manageable scope, and also an indicator of the overall market’s condition. Other coins, including “decentralized finance,” or DeFi for short, which has been making headlines since mid-2020, are also part of this.

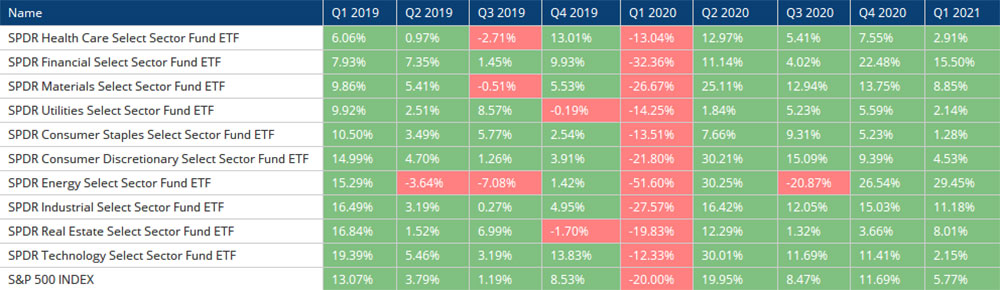

Among the sectors, the energy sector once again came out on top, as in the last quarter. Financials also continued their rise from the previous quarter and likely benefited further from the steepening yield curve. Overall, all sectors concluded the quarter with higher valuations.

With the grand-scale rescue operations by central banks and governments, the markets are, in a sense, moving forward on two crutches. Criticism of such rescue operations is diminishing. While not necessarily today, the danger of a certain hubris is building up.

Today's Focus

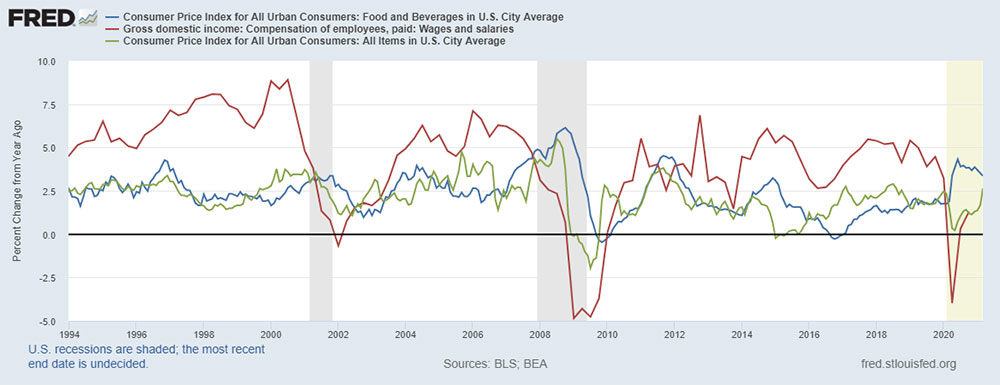

The question currently facing many market participants is whether inflation is back. After years of deflationary tendencies, there are indications that a turning point is at hand. We believe that the deflationary forces that have shaped events over the past roughly thirty years are still at play. For example, globalization, which is being revived under President Biden and exerts downward pressure on wage growth in the Western world. Furthermore, demographic trends and the move towards automation (technology) are likely to continue to contribute. Added to this are the immediate circumstances of the COVID situation, where value chains and supply chains have been interrupted or disrupted, and productivity has also suffered. Should we soon return to the (new) normal, this return is likely to help restore supply chains, keep prices in check, and an increase in productivity could maintain some pressure on wages (at least foreseeably). On the other hand, with government support funds, a lot of new money is flowing directly into the real economy. This is a significant development that did not occur to the same extent with central bank money previously. With central bank reserves alone, no citizen can directly buy anything – as described earlier in these lines; however, through transmission mechanisms, money does circulate to some extent (people feel richer when stocks or real estate rise and are more inclined to treat themselves, etc.). And if a country starts down this path in politics (especially the USA), it could become difficult to deviate from it. A trend towards higher prices and higher interest rates is a real possibility – inflation could emerge, at least in the short term. In the medium to long term, growth is likely to suffer due to high debt, which in turn could cause downward pressure on price development. History teaches us: high debt relative to gross national product, such as in the 1920s or after the 2008/09 financial crisis, was followed by a deflationary or disinflationary period.

Central banks have signaled their intention to keep key interest rates low for the foreseeable future. Even an overshoot of the inflation target (2%) would not yet trigger intervention – because a sustainably higher inflation, moving away from the zero threshold, is desired. The new definition is as follows: Inflation should average around the target, allowing for measurements above 2% to be tolerated (see a message from the Bank of England below – the ECB and the US Fed share this view).

The question now arises as to how central banks measure inflation. It has been indicated on several occasions that, for example, energy costs or food are considered transitory. This means central banks can overlook them. There are indications that wage growth is the decisive factor. After all, the US Federal Reserve has a mandate not only for price stability but also for achieving full employment. In summary, the understanding seems to be that inflation should sustainably detach from current low levels, and this will only be convincing when wages also rise.

Since inflation is also (and some believe, primarily) a psychological phenomenon, it will be all the more difficult to discern or foresee the turning point. Nevertheless, a certain reallocation of investments may make sense, as various cycles point to a shift in the market regime (even if the right timing is hard to hit).

Market Technicals

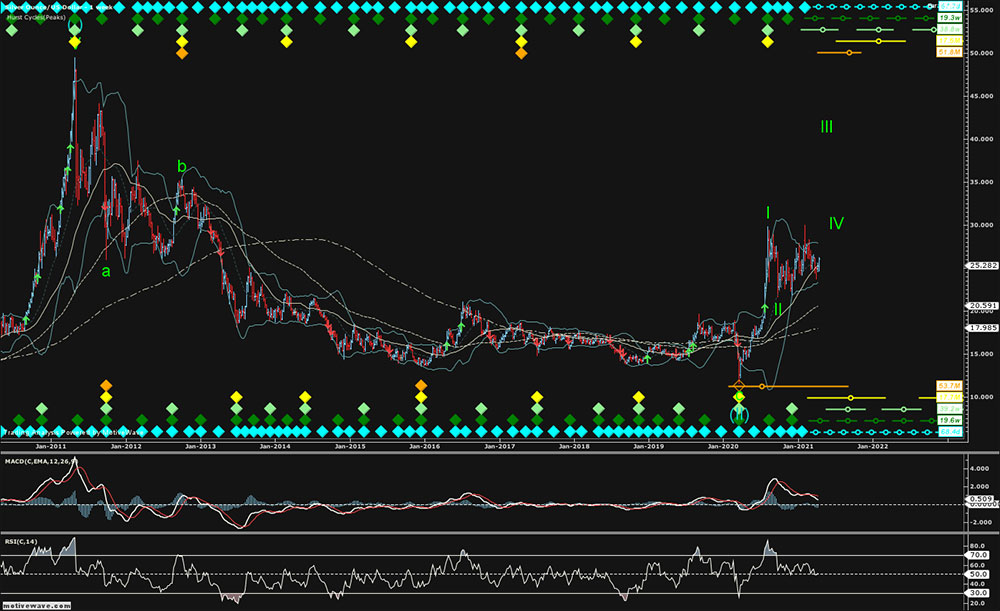

The German stock index DAX shows an upward breakout in the weekly chart, although it is already in a slightly overbought area.

The development of interest rates is likely to be decisive until the end of the year.

Attached is a chart illustrating the yield of the 10-year US Treasury bond compared to the gold price in USD (inverse). It will be interesting to see whether interest rates continue to rise or if they revert to the old trend.

The US dollar is, in a sense, facing a similar question: whether its long-term downtrend will continue or if we have seen a reversal (also in the index against trade-weighted currencies). Since the 2008/09 financial crisis, the US dollar has broken free from its immediate downtrend and is now at the upper end of the overarching trend.

The development of the gold price indicates a probable continuation of consolidation, even if a short-term upward counter-movement should not be surprising. Silver, however, we believe, could still gain ground.

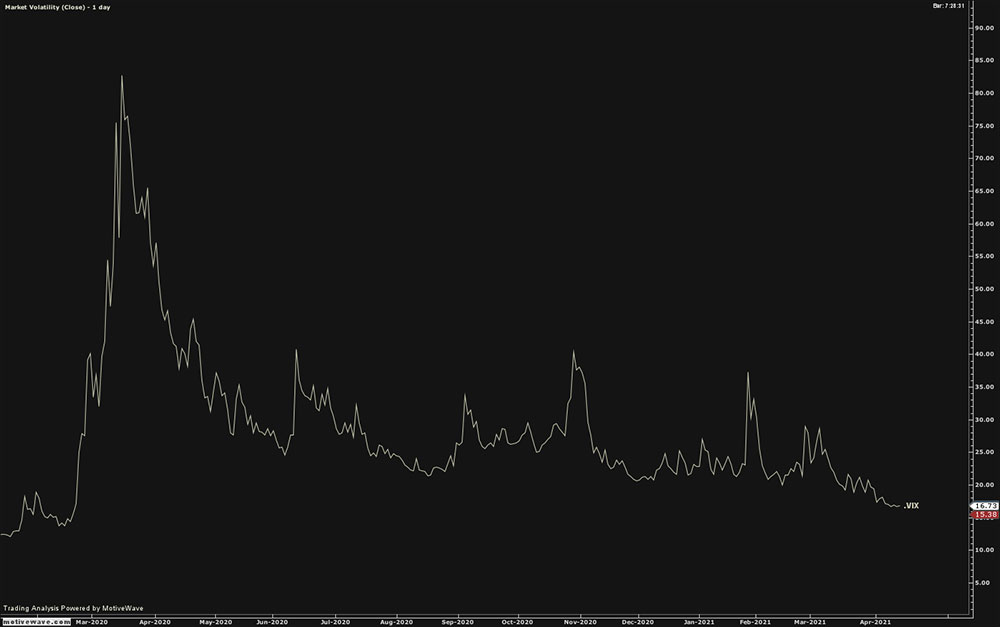

The volatility index has now returned to low levels, consistent with market sentiment, although further downside potential is possible here, should a certain nonchalance dominate again thanks to the incredible money supply.

Outlook

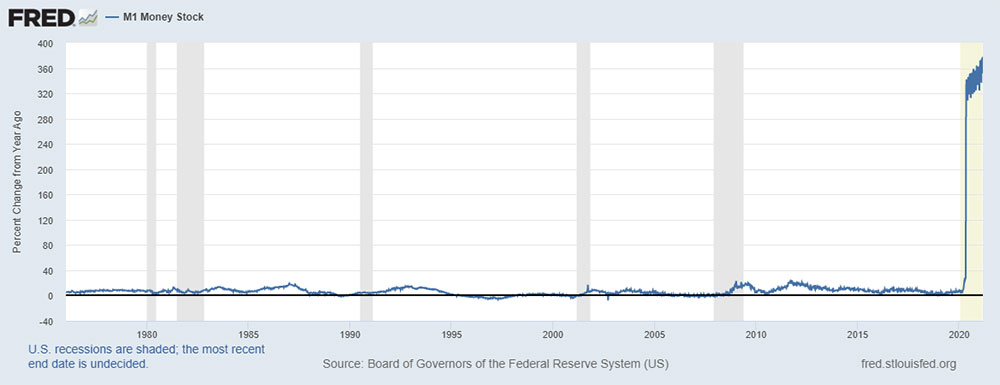

The upcoming quarter promises an environment that could hardly be better – at least for the markets and in the short term. It is obvious that in the long term, this equation does not add up. It’s not as if humanity hasn’t thought of solving problems by printing money before. The markets are flooded with money. The M1 money supply (central bank money) has increased by well over 300% within a year.

Interest rates are still low (enough), governments are providing support wherever they can, the vaccination campaign is gaining momentum, and the population is weary of COVID, which increases pressure to ease lockdowns even with non-low case numbers. However, it is doubtful whether the economy will return to the old normal and thus whether growth will resume. At least, it is difficult to see the middle class gaining better prospects in the foreseeable future. The fact that governments continue to spend money at all costs alone will not be enough. On the contrary. Interest rates would continue to rise if deficits are too high and confidence wanes (though not necessarily for government bonds and reduced for other bonds if central banks support the markets). With rising interest rates, volatility would return. Stock markets can withstand a certain degree – historically, inflation of around 2% is even almost optimal, but if inflation continues to rise, stocks usually suffer as well. This does not necessarily have to happen in the upcoming quarter. The markets can continue for a good stretch as before. With two crutches – one from the central bank and now support via fiscal policy – progress is made, albeit less dynamically.

Portfolios should take into account a potentially more fragile world. In addition to a certain degree of diversification, there are now investments that promise a trend reversal and offer favorable entry opportunities. It will be interesting to see how gold prices and commodities behave. Both could gain ground or at least act as value preservers in a scenario of increasing inflation. In equities, it is expected that more defensive stocks will continue their catch-up with growth stocks. This comes after the former had been in a correction since around 2018, which is likely to have ended last summer. Should nominal interest rates continue to rise, it is almost a given that real interest rates are likely to remain negative. Between 1945 and 1951, the USA also saw a policy of a controlled yield curve, where the central bank bought 10-year government bonds to keep the yield at 2.1%. The economy grew faster than the yield (of debt), and national debt reduced over the years from 110% to about a quarter of its initial value. Savings accounts and bond portfolios were the losers. Real assets with income potential – if acquired at a good price – were the better choice, as they are today. How strong inflation will be this time, whether it will only be a temporary phenomenon, and whether deflationary forces will soon regain the upper hand, should become apparent soon.

“Inflation is taxation without legislation.” Milton Friedman

EDURAN AG

Thomas Dubach