The Navigator provides insight into stock market events with an outlook.

“Time to pause.” The economy continues to recover as lockdowns are lifted in many places. Supply chains on the supply side can hardly keep up with demand, which is strong due to pent-up savings capital combined with a backlog of consumption. As a result, prices are rising. The stock markets still seem carefree. However, we are likely approaching the window where inflation or a relapse into deflationary tendencies will dominate events in the markets. The showdown is underway: For the quarter, the markets developed sideways with a slight tendency to strength.

Market review

The markets confirmed the upward trend of the first quarter and have – once again – anticipated economic development. According to the soothsayers, the economy should continue to stabilize and – also trusting in the success of the vaccination – return to normality. However, this normality will look like in detail.

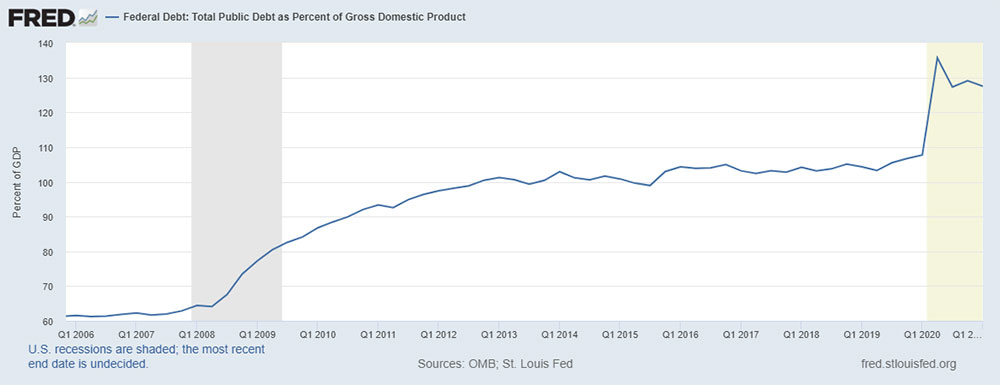

The lockdowns ordered by the governments with the associated burdens continued to contribute to the growing debt amount: Measured as a percentage of gross national product, the debt burden of the still largest economy in the world, the USA, has noticeably exceeded the 100% mark and, at over 130%, has set a new noteworthy mark far above the 106% mark after the Second World War.

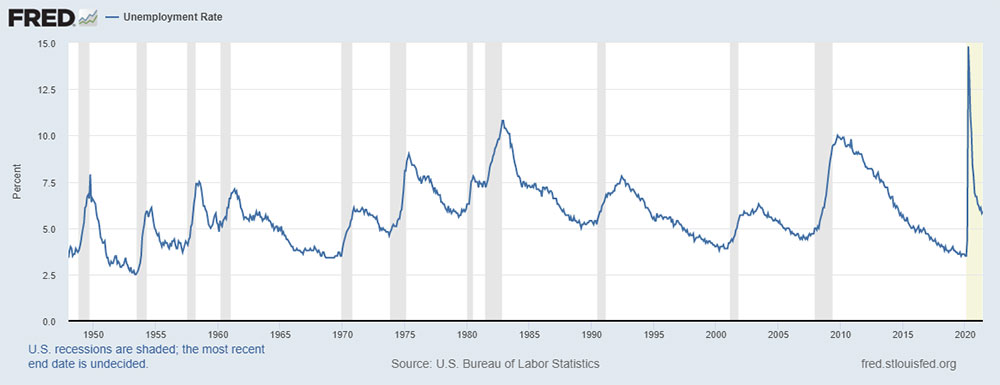

With the reopening of the economy, unemployment figures have also fallen rapidly. At the current pace, unemployment figures could return to the level before the declared pandemic as early as the end of 2022. This would be a recovery that is taking place approximately five times faster than during the financial crisis.

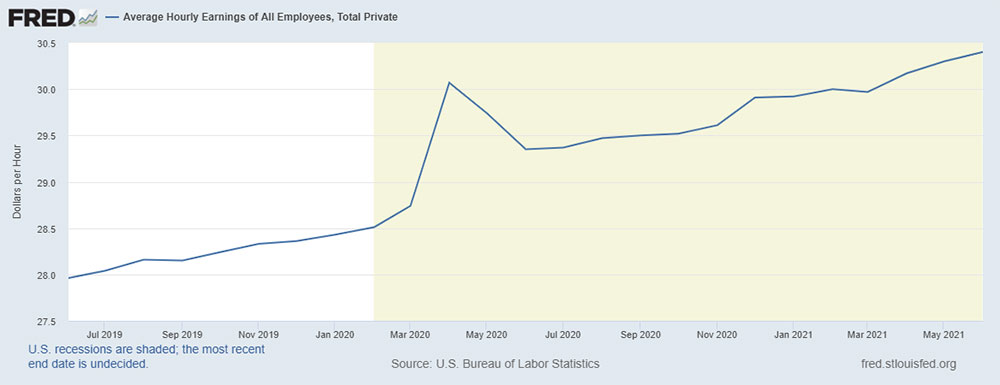

Wages have also risen simultaneously in the labor market. Criticism is being voiced that, due to the relatively generous government support funds, companies have to pay higher wages so that people return to the labor market.

With the magnificently designed rescue operation by central banks and governments, the markets are, in a sense, on two crutches. Criticism of such rescue operations is becoming less and less. Even if not necessarily today, the danger of a certain hubris is piling up.

Stock markets

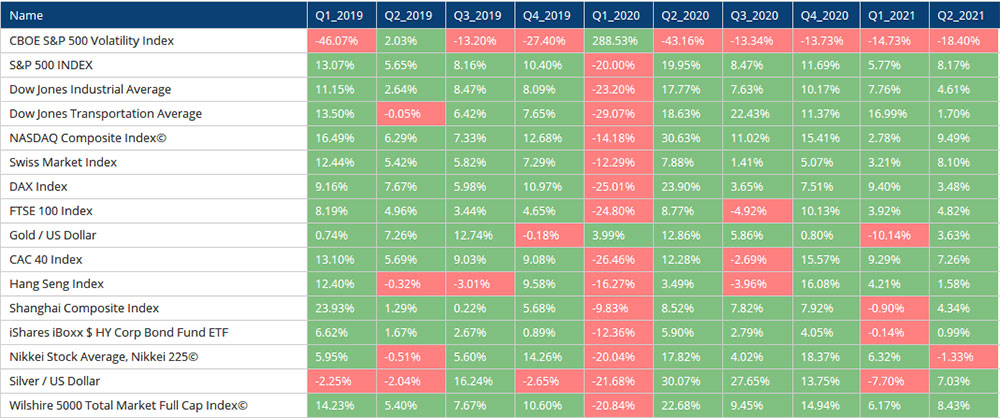

In terms of sectors, energy stocks were able to increase noticeably, but there were sectors that benefited even more: the real estate sector swung upwards most strongly, followed by technology stocks. At the lower end of the spectrum is the utilities industry, followed by consumer goods stocks/staple foods, which are likely still suffering from reduced capacity utilization.

Today in focus

Around 75 years ago, there was a turnaround in interest rates. Measured by the longer-term US government bonds, interest rates bottomed out in the spring of 1946 at just over 2%. Over the next 10 years, the interest rate level of these bonds rose to just over 3%. It was the beginning of the famous bond bear market, which lasted from 1946 to 1981. A beginning without much fanfare, but with emphasis.

These days, interest rates are again increasingly in the spotlight. In simple terms, one can identify two (opposite) interpretations of the current events: Inflation is setting in or disinflation is returning (or even worse: deflation is setting in).

According to official statements by the central banks, the current development is a so-called transitory inflation. Prices are rising because i) a lot of money has been saved during the lockdown period and the pent-up consumption is now being made up for, and because ii) capacities have been reduced by the lockdowns and are now lacking on the supply side. After a brief increase, the inflation development should level off again and rise slightly, according to the central banks’ plan. The inflationists see it somewhat differently: the increased prices will remain, which in turn calls for higher wages. An upward spiral is set in motion. The deflationists agree with the central banks that the increase in inflation is only of a temporary nature, but thereafter the deflationary forces of recent years will continue to prevail (demographics, technology, debt pressure on economic vitality).

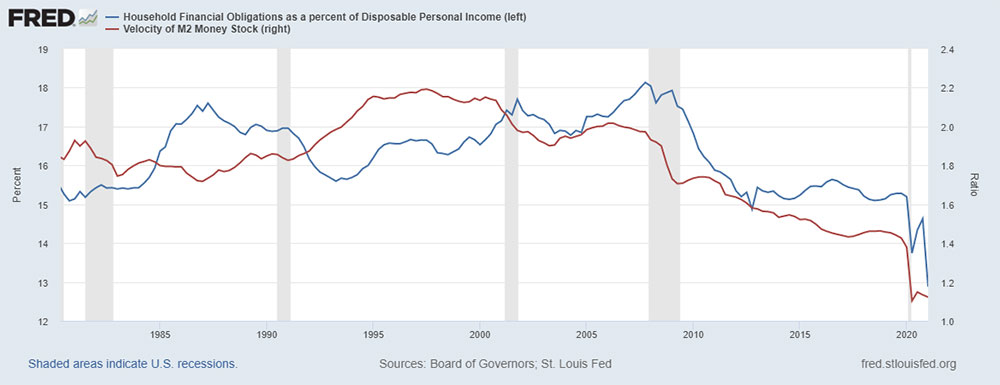

From the monetary side, there is much talk in the market of money printing and, consequently, of rising inflation. The central banks lowered interest rates in response to the events of the financial crisis of 08/09 and then, at the end of 2011, began to buy up more bonds on the market. As a result, the balance sheets of the central banks have been massively increased. However, the money with which the bonds were bought has not come directly into circulation, but is recorded as a credit of the commercial banks in the balance sheet of the central bank. Low interest rates should encourage private individuals to take out loans. This gets the economy going. Low interest rates, however, also show that lending is faltering: Interest rates are lowered so that loans are taken out again. Milton Friedman pointed this out in his work. If interest rates are too low, the banks increasingly only lend to solvent clients, as there are hardly any reserves or margins for defaults. We may have reached this point with the Covid shock – lending has decreased according to the published statistics. The money that commercial banks have as reserves with the central banks remains trapped in the banking system and does not find its way into the economy. Thus, there is tendentially too little or simply less money in the economy; in addition, existing loans will one day be repaid, including interest. The thesis can be put forward that with faltering lending, the amount of money in circulation shrinks and assets would have to correct downwards. As a consequence, deflationary pressure arises.

The figure shows, for example, the relationship between the indebtedness of private households and the velocity of money (money supply M2: cash circulation and book money sight deposits).

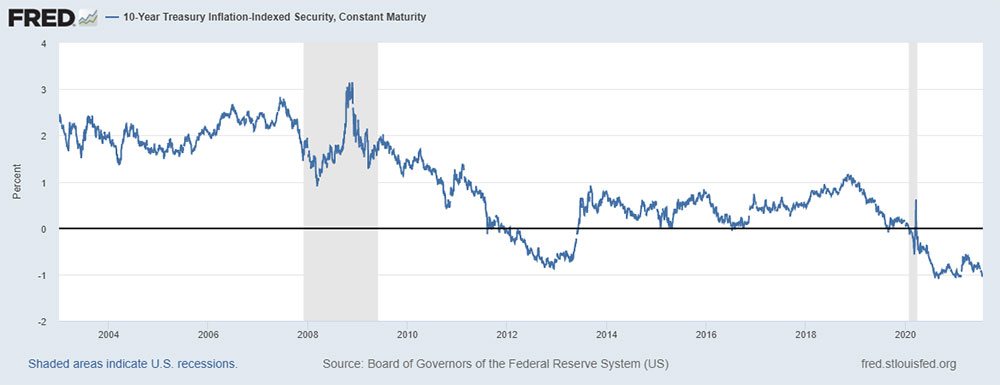

The yield on the 10-year US Treasury has initially fallen somewhat again after a striking increase was recorded in the first quarter. Do the markets share the view of the central banks, namely that inflation is only of a temporary nature, and/or that the bonds are simply increasing in value because the banks cannot lend the money and therefore invest it in fixed-income securities?

The inflation-adjusted government bonds show no major tendencies towards rising inflation. On the contrary: If one compares the current situation with the crisis in 08/09, similarities can be observed. After an initial surge in yield, it was again lower towards the end of the quarter.

The yield curve has become a little steeper over the quarter. However, it has recently flattened somewhat after the Federal Reserve meeting (the short rates could be raised somewhat earlier than thought, according to speculation).

In Europe, on the other hand, yields have risen somewhat, as with the German Bund, where the yield (10 years) has risen from -0.29% to -0.20%. In Italy, yields have risen from 0.67% to 0.82% and in France from 0% to 0.13%. The industry is recovering, and the euro could not break out upwards (next attempt to weaken against the US dollar?). In the United Kingdom, the yield fell from 0.85% to 0.72%.

Outlook

The Biden administration has big plans and is planning additional spending in the order of USD 6-8 trillion (up to slightly above). This makes up about 1/3 of the estimated annual economic output of the USA. US citizens receive USD 1400 via the «American Rescue Plan» in addition to the already paid out USD 600 and the USD 1,200 sent by the then Trump administration. The «Build Back Better Plan» also consists of the «American Jobs Plan» and the «American Families Plan». One notes: The state is firmly taking the reins.

Also elsewhere, in other nations, politics has taken measures and set up programs to help private individuals and companies. Legitimate, because politics with the lockdowns has caused the damage. But: What has once been installed by politics often remains longer than thought. Dependencies arise with the consequence that the state could gain influence over the private sector. Soon, regulations imposed by politics are likely to follow. The economy will be less free. The needy will be those who can (or must) pay the bill to the state and are not very mobile: the middle class and the trade. The Trump administration was on the way, true to the mantra «Make America Great Again», to bring capital and jobs back to the USA – at the expense of the winners of globalization over the last 20-30 years such as China or other global as well as regional (Mexico) workshops. The Biden administration seems to want to work less emphatically in this direction and thus a part of the value creation will take place outside the USA. Without additional (sensibly paid) jobs and thus income, the political situation is likely to remain tense, in the USA, but also in Europe.

Basically, it seems to be assumed in the market that what has taken place in the markets in the last ten years or so will continue. Central banks – and newly since Covid also the governments – are always trying to cushion distortions. Interest rates remain low, capital is driven into risky assets. However, as explained in the section on interest rates, the lower the interest rates, the more lending falters (banks become more selective in lending due to the lower margin). This could have fatal consequences, because the deflationary forces would gain momentum and assets, including stocks, would have to lose value as a consequence. It is therefore important to keep a close eye on this development, to invest in quality and to diversify where possible (which can be a challenge, as much depends on interest rates).

“There ain’t no such thing as a free lunch.” Robert A. Heinlein, „The Moon Is a Harsh Mistress“, 1966

EDURAN AG

Thomas Dubach