The Navigator provides insight into stock market events with an outlook.

January 9, 2022

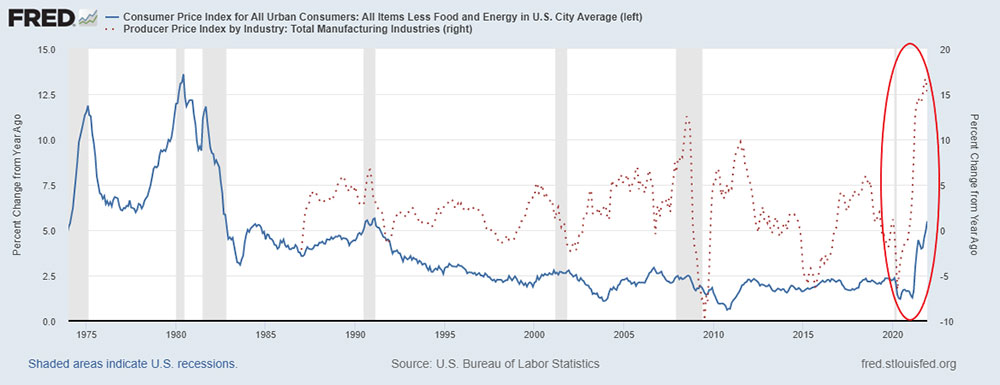

“D-Time.” Towards the end of the year, an outlook is presented in which inflation occupies a prominent position. Politicians worldwide have noticeably more to say than before the pandemic: Lockdowns and quarantine regulations lead to a shortage of supply, and at the same time, social programs and stimulus programs do not reduce the money supply accordingly, but even expand it. In addition, there are measures regarding climate change, which make energy more expensive and further contribute to inflation. The central banks are under pressure to act and are talking about countermeasures. This would withdraw capital from the stock markets, and nervousness is spreading accordingly. We are in a time of decision – are we moving towards administered markets or are we finding our way back to a free market economy?

Market review

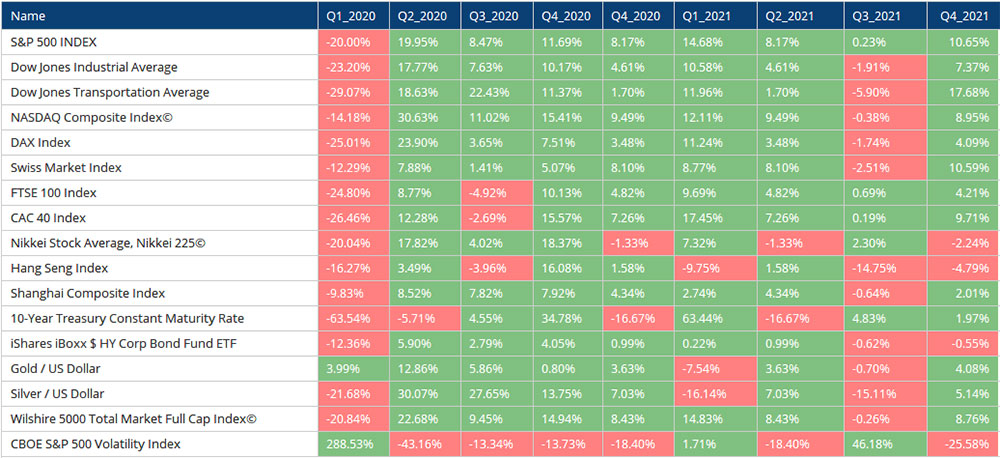

On balance, the markets were able to leave a friendly impression in the fourth quarter. In the meantime, this looked different: In November, sentiment fluctuated and investors were risk-averse. Since then, the markets have been moving sideways, with a partial breakout to the upside towards the end of the year. The more defensive stocks were able to gain some ground against the cyclical stocks – in some cases also against the growth stocks, although there was a strong recovery here towards the end of the year, primarily in the US tech stocks. The Asian markets were under somewhat more pressure and some even closed slightly in the red. Analogous to the tense situation in November, volatility broke out to record highs, as we last saw in March 2020, but then fell back to more cautious levels of below 20 by the end of the year (measured by the US S&P500 Index).

After the stock markets tended to leave the second quarter rather at the upper end of the range, the third quarter was left tending to be at the lower end of the range.

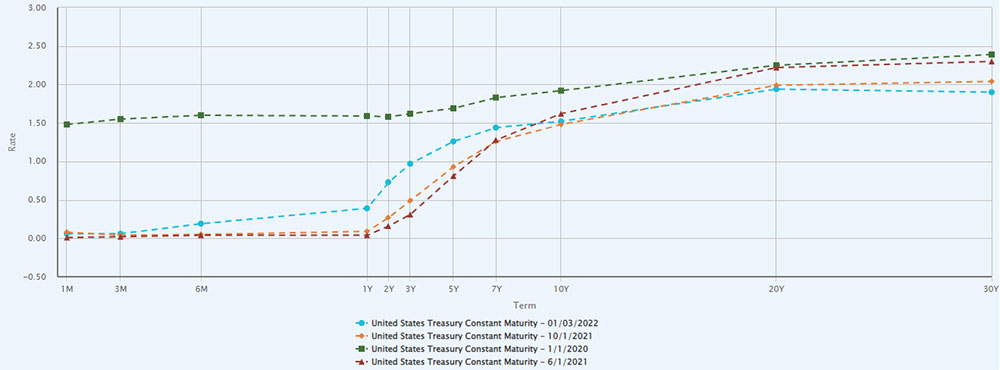

With regard to interest rates and capital markets, a slight increase can be seen in short-term and, even more so, in medium-term interest rates. However, the 10-year yield remains almost unchanged, and has even fallen somewhat compared to a year ago. The steepness of the curve is also somewhat flatter than it was a year ago.

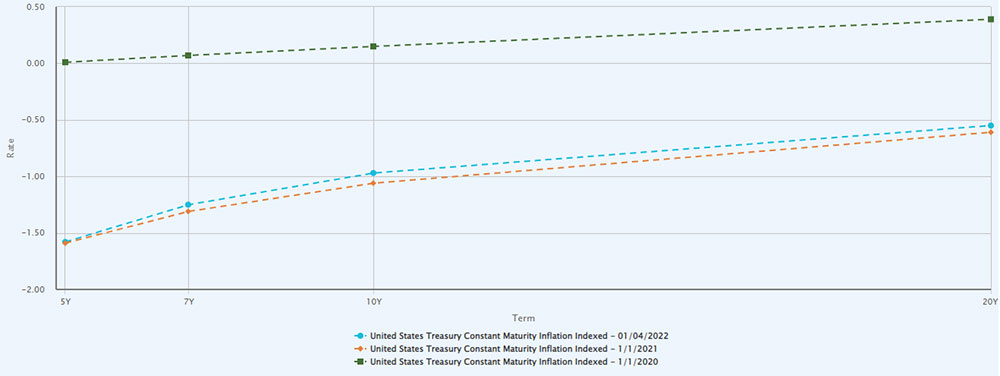

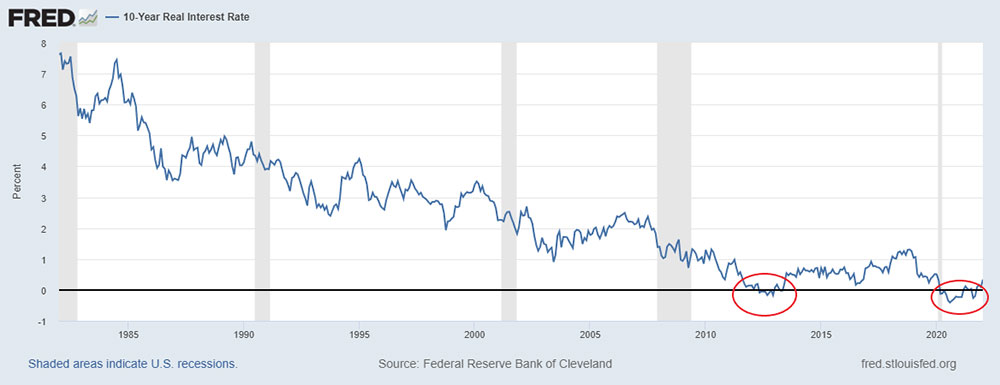

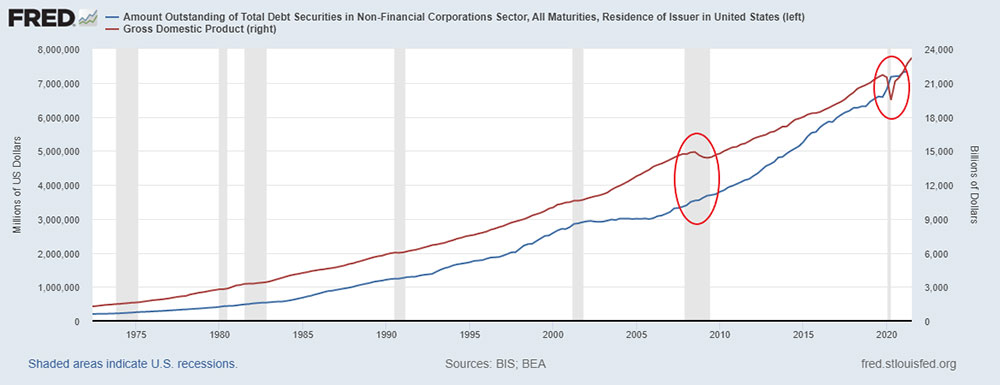

In general, it can be said that, contrary to general perception, the capital markets do not see sustainable inflation. Inflation-adjusted yields show only a minimal increase compared to a year ago, but a noticeably lower yield compared to two years ago.

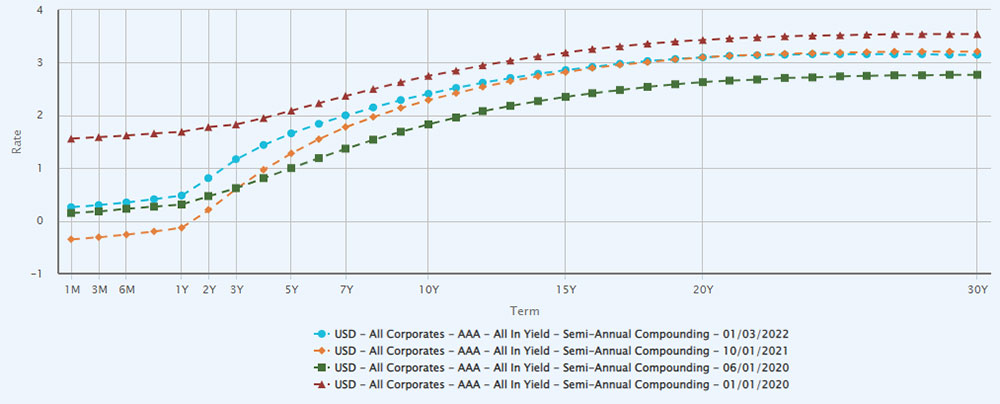

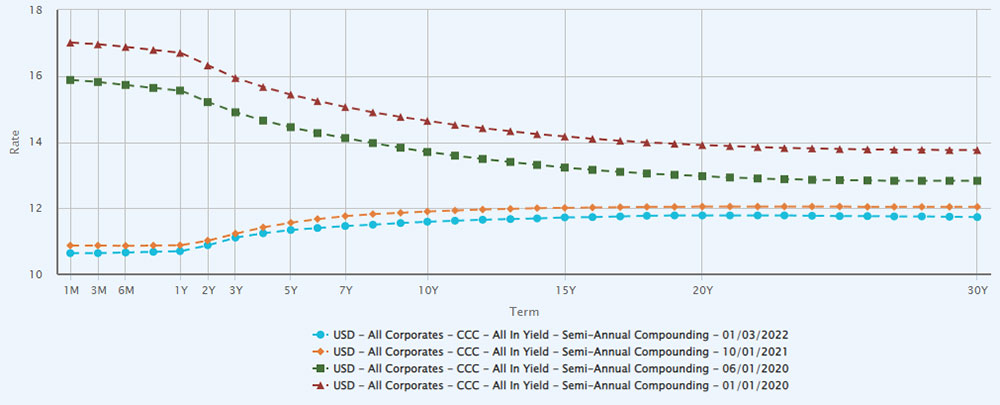

A certain relaxation can be seen in corporate bonds, where the yields for poorer debtors have fallen slightly. Compared to the time before the pandemic, the curve is also no longer inverted for this sector and, in general, has tended to become steeper for the last quarter of 2021.

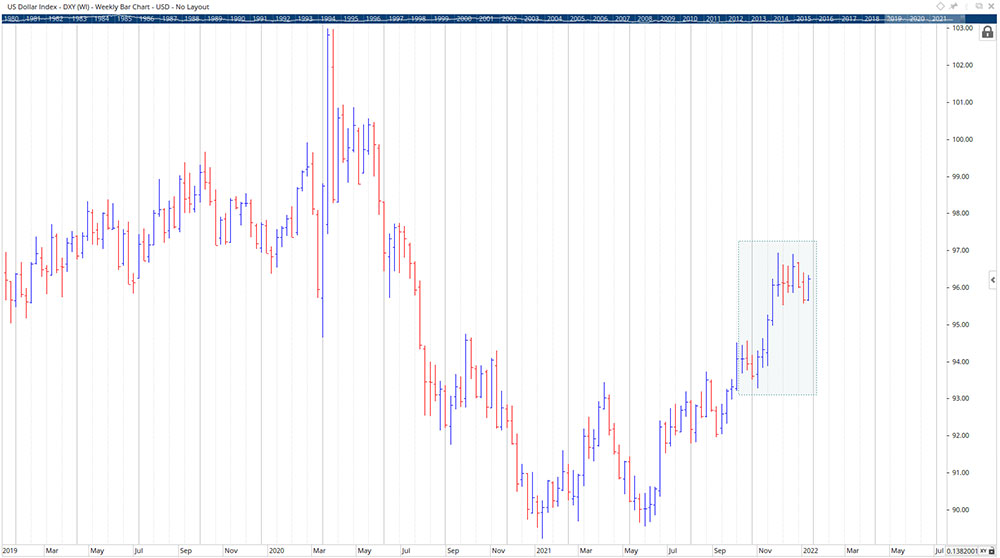

The US dollar was able to break away from its lows and has managed a breakout to the upside in the index (the index consists of over half of the exchange rate against the euro, which showed weakness).

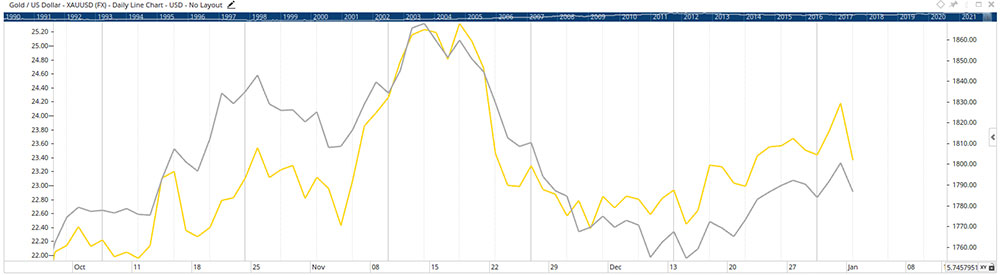

Gold has demanded a lot of nerves from investors, as there was once again an attempted breakout to the upside. It remained an attempt for the time being, as did silver, which shows great potential for catching up with gold in the longer term.

In focus

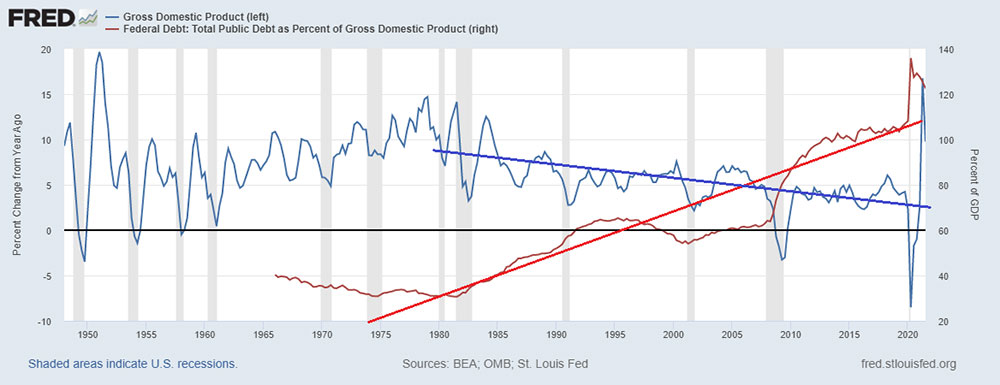

The years of decision – and it seems as if we are in the middle of them. As already mentioned several times in these lines, we are registering mounting mountains of debt with a simultaneously decreasing growth rate. This trend has existed since the beginning of the 1980s.

The low interest rates of these days are probably not only due to the policies of the central banks, but also to the trend towards lower growth rates (where demographic development is also likely to be a significant factor). The central banks are fulfilling their mandate and combating the associated pressure on prices, disinflation, although the central banks hardly have the instruments to do so effectively. As a result, we see the balance sheets of the various central banks expanding and, as a result, an inflation of assets: The money does not find its way into the producing economy, but into the financial industry (stocks, bonds, cryptocurrencies and NFTs, but also into art or real estate financed by mortgages). The thesis here is that with increasing debt and low interest rates, commercial banks are increasingly only willing to grant loans to solvent debtors. The margin for defaults is thin.

With the pandemic, the lockdowns and other measures such as quarantines, economic output has been curtailed. However, the same politicians, with less production, have tried to compensate for losses in income as much as possible and to pay out money with the help of stimulus packages.

The decision of these years will be whether we see a debt cut or – more likely – a slow “growing out” of the situation. The latter would require negative real interest rates. Should inflation prove to be persistent, the central banks will come under increasing pressure and will have to raise interest rates (price stability as a mandate) and thus choke off the economy. This is all the more true as rising interest rates also put pressure on the stock markets: The financial markets play a not insignificant role for growth in the consumption-driven, rich industrialized nations.

Outlook

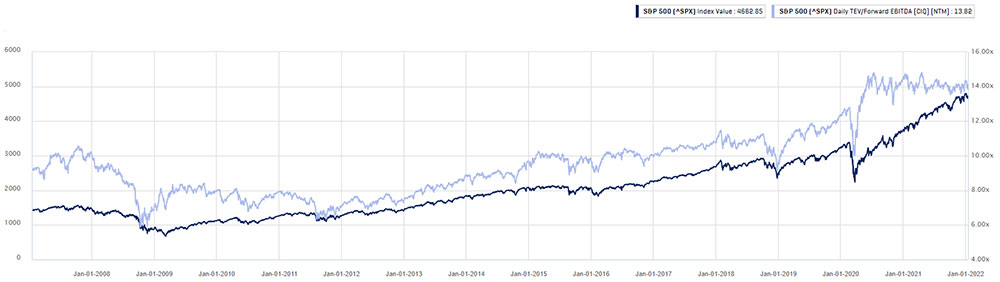

The stock markets are known to anticipate current events. 2022 could therefore be the year of decision on the stock markets. If we are near the end of the dead end, consisting of high debt, low interest rates and rising inflation, the measures taken by the central banks will put pressure on valuations. The stock market corrects. However, if inflation flattens out again, we should see more of what already exists: The low real interest rates support the stock markets and, if anything, valuations will continue to rise.

The past decade has brought such an increase in valuation. The pandemic was a turning point, where the economy collapsed excessively and debt increased again. The issue of refinancing remains and hangs like a sword of Damocles over the valuations (debt-financed assets).

For investors, the choice is likely to be limited for the time being: interest rates will be low even after the forecast interest rate hike and the money will flow into risky assets. In the event of a threatened price correction, investments with the most solid earnings potential are still recommended.

“It is better to be approximately right than precisely wrong.” Warren Buffett

EDURAN AG

Thomas Dubach