The Navigator provides insight into stock market events with an outlook.

July 7, 2024

“Focus on Interest Rates”. Inflation is weakening as expected. The additional COVID fiscal stimulus, driven by free-spending consumers, caused an inflationary surge, following supply shortages due to lockdowns. As expected, this effect dissipated over time. Nevertheless, inflation remains a topic. Combined with uncertainties surrounding the upcoming US elections and the ongoing conflicts in Ukraine and Israel/Middle East, the second half of the year presents a mixed outlook. A sideways movement is likely, where growth stocks and value stocks could move in opposite directions.

Market review

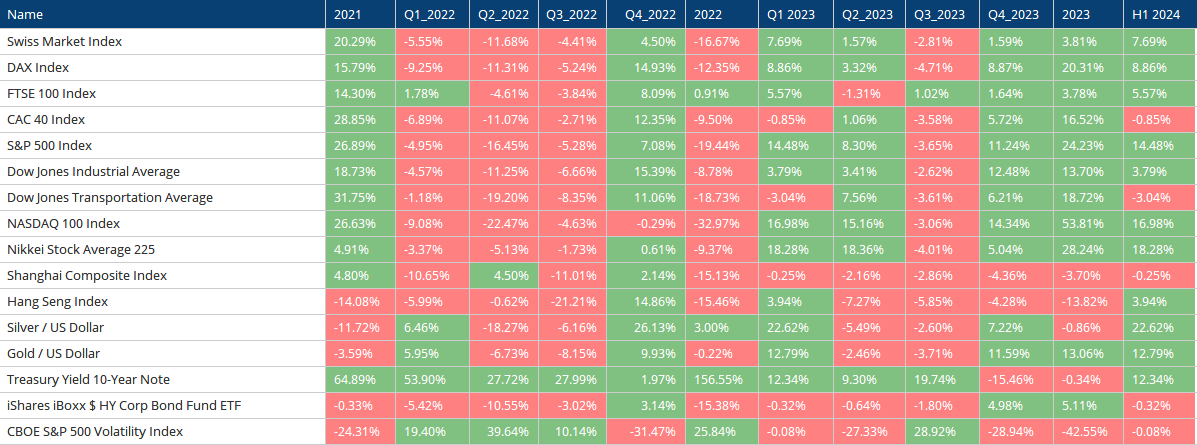

The first half of the year started with euphoria, as markets bet on declining inflation and thus a series of interest rate cuts. However, according to official readings (statistics), the economy in the leading US market appeared to be performing better than expected, which prompted central bank(s) to take no action for the time being. The markets believe that a delay is not a cancellation.

Overview of Selected Indices

Source: Optuma

Furthermore, technology stocks gave the markets an additional boost. AI made the chip manufacturer a market darling. While in 2023 it was the Magnificent Seven that lifted the markets, in 2024, a single stock is enough. Nvidia’s market capitalization reached over 3 billion USD in early June 2024, surpassing the gross domestic product of some European countries, including France and Italy.

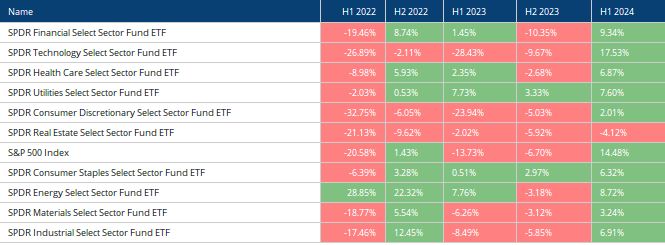

Selected Sectors in Comparison / Source: Optuma

Furthermore, gold advanced to new record highs. The important mark of around $2,050 was broken in the first quarter. The progress of the BRICS nations, where important states like China and Russia have been buying gold for a long time, along with the spiraling debts in the West, is driving demand.

In focus

Outlook

With declining inflation, the market discounts interest rate cuts. After central banks rapidly hiked interest rates, the first signs of braking are appearing. Even if still subtle, the rhetoric indicates an imminent shift in monetary policy. The labor market, as well as – self-evidently – inflation figures, need to be monitored. Here, the pundits are likely divided into two camps: The central bank, for one, sees the possibility of controlling the economy, including inflation, through adjustments. The other half, so to speak, primarily views inflation as a psychological phenomenon, where one tends to react rather than act, and the former is usually too late. Nevertheless, deflationary or disinflationary pressure seems to be present. In Western industrialized nations, demographics play a role (the post-war generation is retiring), and with higher interest rates, it is becoming increasingly difficult to refinance the immense debts. China has just experienced a shock in the real estate market and is currently struggling more with deflation than with inflation. The political situation also implies that raw materials are likely to become more expensive. Western Europe has many people but few raw materials – Russia has few people and many raw materials. A new economic community is forming with the BRICS nations, and it will be more difficult for the industrialized Western states to access cheap raw materials. This, in turn, represents the counter-movement and drives prices up. For capital, a balanced portfolio offers the safest home in an increasingly uncertain world. The market bear continues to stalk through the woods; it was closely pursued, but has not yet been brought down.

“It is in the nature of capitalism that outbreaks of madness occur periodically.” John Kenneth Galbraith

EDURAN AG

Thomas Dubach