The Navigator provides insight into stock market events with an outlook.

January 10, 2024

«Bear Hunt». The markets did not really get going and the Hamas attack on Israel brought the slump. With a view to potentially higher oil prices, inflation then fell further. Worse was avoided, so that the markets were able to recover significantly towards the end of the year due to the cautious positioning in combination with potentially lower interest rates.

Market review

The markets were able to make up for some ground in this fourth quarter. Thanks to an outlook that does not promise any further increase in inflation and thus a possible end to the rise in interest rates. Above all, markets in the euro area were able to make up ground in percentage terms, after they were oversold not only due to price losses but also due to currency factors – investors increasingly bought the oversold German market, Europe in a broader sense.

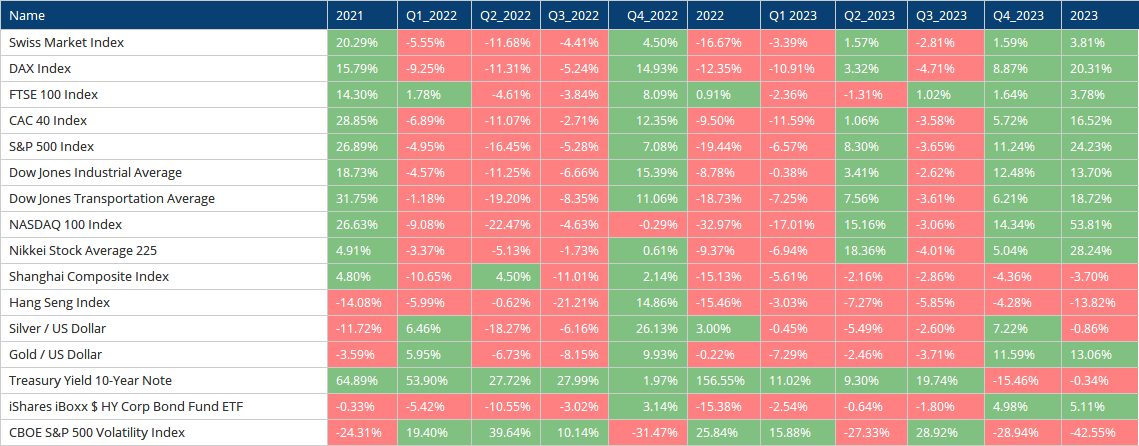

Overview of selected indices

Gold and other precious metals also gained and came close to previous highs. A breakout upwards clears the way to new all-time highs. In terms of currencies, there was a countermovement against the strengthened US dollar, which brought the EUR back above parity, and in the case of the yen, similar to the stock market rally, an equally strong countermovement set in towards the end of the year (USDJPY).

The energy sector continued its consolidation, but closed the second half of the year slightly in positive territory. However, it was replaced by the recovering financial market and the technology sector in the lead. Consumer Staples and Utilities went negative out of the second half of the year, despite the strong fourth quarter. The mixed situation with a still strong consumer and labor market (at least according to statistics), falling inflation figures and massive interest rate hikes, especially at the short end, shows first tendencies, but not yet a clear picture. However, the recession expected at the beginning of the year seems to be off the table.

Overview sectors

Overview of sectors (SPDR)

In focus

The expected recession did not materialize, at least in the first half of the year. The labor market is holding up surprisingly well, even if cracks are visible upon closer inspection. However, consumers still seem to be able to draw on Covid funds, the stimulus is still working. The economy sees itself forced to accept higher tariffs, approaches to a dynamic towards the employee market. This is mainly because it seems difficult to get people back to work. However, this circumstance will probably weaken when the massive programs of the governments have trickled through the system. The attack by Hamas on Israel brought a turning point, at least geopolitically. After a brief twitch, the markets adhered to the motto that political stock markets have short legs. But here, too, much remains vague and the situation remains uncertain, where further misfortune can shock the markets at any moment. Seen above all this, the money seems to continue to find its way into risky investments. At least into the selected large-capitalized names. The market breadth has decreased again and the indices form negative divergences here and there. The flip side offers attractive investments, namely where the large hoses of passive investments do not find their way. But also in blue chips, such as Roche, the last two years have corrected and offer a dividend yield of almost 4% with a valuation of >10x the operating profit. Also technically, some titles in the midcap range are in the starting blocks. The prospects are difficult to manifest, which probably tempts investors to invest in the upward-trending growth stocks. However, these are expensive and, according to Adam Riese, will reduce the premium again one day – and not all will be able to meet the forecasts. The focus for us is the intermediate stage, away from the low interest rates, towards either higher rates in the medium term or then into a recession. The debt situation of the nations has deteriorated continuously, the political landscape has become more fragile. Investments with a low risk premium shine, in our eyes, and the current situation offers opportunities to expand the portfolio accordingly.

Outlook

With the easing inflation, the market is discounting interest rate cuts. After the central banks have rapidly raised interest rates, the first signs of braking are appearing. Even if still subtle, the wording indicates a soon turnaround in interest rate policy. To be kept in mind are the labor market as well as – self-evidently – the inflation figures. Here, the augurs probably divide into two camps: The central bank at the forefront sees the possibility of being able to control the economy including inflation by means of adjusting screws. The other half, so to speak, sees inflation primarily as a psychological phenomenon, where one reacts rather than acts, and the former usually too late. Nevertheless, deflationary or dis-inflationary pressure seems to be present. In the western industrialized nations, demographics play a role (post-war generation is retiring), with the higher interest rates it is becoming increasingly difficult to refinance the immense debts. China has just experienced a shock in the real estate market and is currently struggling more with deflation than with inflation. The political situation also brings with it the circumstance that raw materials are likely to become more expensive. Western Europe has many people, but few raw materials – Russia has few people and many raw materials. With the BRICS states, a new economic community is forming and it will be more difficult for the West of the industrialized states to get access to cheap raw materials. This in turn represents the countermovement and drives prices upwards. For capital, a balanced portfolio offers the safest home in an increasingly uncertain world. The stock market bear continues to roam through the forests, one was close on his heels, but he could not yet be killed.

“Cheap money leads to malinvestments.” Tom Borg

EDURAN AG

Thomas Dubach