The Navigator provides insight into stock market events with an outlook.

January 03, 2023

“Recession”. The markets are anticipating a possible interest rate turnaround. After a market correction, a turnaround occurred after the first third of the fourth quarter and a strong price rally began. Although much is amiss with the after-effects of the Covid crisis, where supply chains are being redefined, and the conflict in Ukraine, where the BRIC states are distancing themselves from the USA, the markets seem to be pleased for the time being that inflation is weakening somewhat. However, the aforementioned harbors additional potential for inflation. There is also the threat of an economic slowdown if less money is available for consumption.

Market review

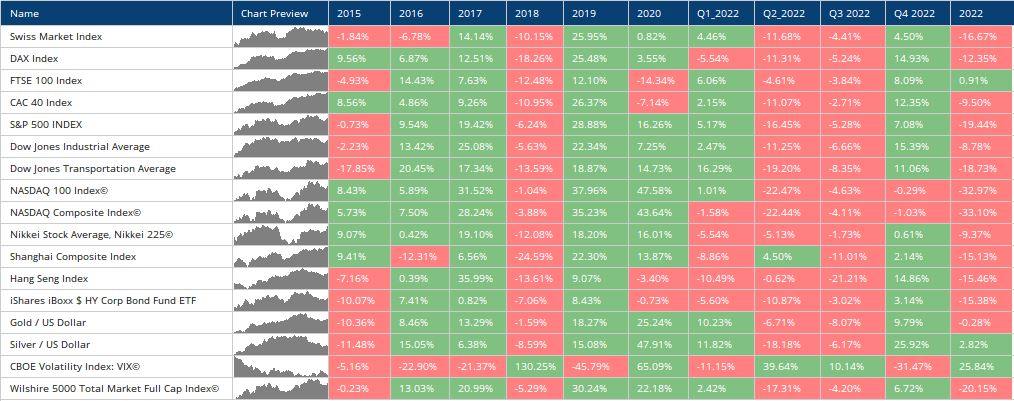

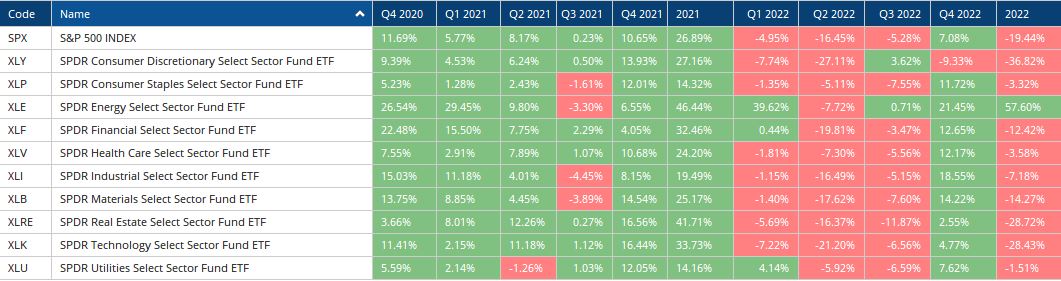

The markets were able to make up for some ground in this fourth quarter. Thanks to an outlook that does not promise a further increase in inflation and thus predicts a possible end to the rise in interest rates. Markets in the euro area in particular were able to make up for some ground after being oversold due to both price losses and currency factors.

Gold and other precious metals also gained and came close to previous highs. In terms of currencies, there was a countermovement against the strengthened US dollar, which brought the EUR back above parity and, in the case of the yen, brought the strong decline that had been going on for several months to a halt for the time being with a no less dynamic countermovement.

In terms of sectors, it was once again the energy sector that was able to gain the most. In the technology sector, confidence returned, with titles that have undergone a noticeable correction over the last >12 months and recently made headlines with cost adjustments.

In focus

Where the outlook still looked bleak in the summer until the beginning of this fourth quarter, the turnaround came with the inflation figures in October. An oversold market turned positive. Inflation remains the focus of the debate: The central banks are relentless in the fight against inflation, but the market seems to believe that the words do not necessarily have to be followed by deeds, especially if the economy falls into a slump due to the drastic rise in interest rates. It seems plausible that the inflation figures will come down from their highs. The supply chains are reorganizing, and supply bottlenecks are dwindling. But much is becoming more expensive because it is no longer just the price that matters, but also security. The conflict in Ukraine adds another uncertainty, namely how lasting the divide between East and West, or between the USA and its closest allies versus the BRICS states, will be. Are we heading towards a divided, new world order or will everything return to normal? In our opinion, the market seems somewhat nonchalant here, underestimating the risks of a recession or other crisis.

There are already indications in this quarter that not everything is as good behind the headlines as it seems. For example, the US labor market, where unemployment figures are back at low levels as they were before the Covid crisis, which in turn was the lowest since the early 1970s. It turns out that a worker with three jobs, because one alone pays too little, also contributes to this positive statistic. Or that when employer costs rise, it does not necessarily – or demonstrably – mean that the employee has more money in his pocket. Also, participation in the labor market is still significantly below the level before the Covid crisis and again massively below the level before the financial crisis of 2008/09. The ice we are walking on has not gotten thicker.

The US housing market is also tending towards weakness with declining house sales/transactions, which contributes a significant part to economic output.

Outlook

The recovery is likely to take some time, as inflation figures could continue to fall somewhat after the initial surge. The crucial question could be whether the inflation was just a flash in the pan or whether it will remain with us in some form. While the distortions due to the lockdowns initially provided a good reason for the rising prices, politicians intervened, distributed checks, supported left and right, and most recently wage negotiations also made headlines, e.g. the federal civil servants in Bern with over 2% more wages for the new year 2023.

The opinions of the soothsayers are widely scattered and more or less dominant depending on the market situation. One variant would be stagflation, with interest rates slightly below inflation, perhaps similar to what was seen after the Second World War. Because the mountains of debt are high, the states cannot afford high interest rates and with such a constellation, the ability to act can be regained. The savers pay for it. Seen in this way, the stock markets would be in good shape again in the medium term, as values can be maintained – accepting a valuation expansion (one will have to pay more for a future unit of earnings). But until then it can remain volatile, we rely on stocks and in this spectrum heavily on the most solid titles possible with cash flow as well as a promising business model.

“Where strength does not suffice, deception must be employed.” Pietro Metastasio

EDURAN AG

Thomas Dubach